Today’s Product Manager 2014

The environment that product managers work in today is both unsettled and unpredictable. That theme reverberates throughout our 6th annual Product Manager Survey as our respondents express a little more concern about how their brands stack up and what the future could hold for their current company. For example, respondents rated several of their brand’s individual attributes less favorably compared to previous years. Respondents also expressed a growing concern over managed care, market access, payer influence and the reimbursement environment.

It is clear the effects of the ACA and the shift to an outcomes-based healthcare system are forcing marketers to rethink their approach. No longer is a superior clinical profile enough. Now, product managers must demonstrate a value proposition that shows how their brand can save money, decrease hospital time, reduce the amount of additional procedures or medications, etc. All of the players involved in the healthcare system are still trying to determine what is the best approach to improve patient outcomes—which is the ultimate goal—and product managers are working to figure out what they need to do to show their brands are capable of doing just that.

But product managers are also working in an industry that is wheeling and dealing like crazy with new mergers and acquisitions seemingly announced daily. And respondents believe that these deals will have a greater influence on the industry than the past few years. Of all the factors we ask respondents to rate based on their impact on the industry the past year as well as next year, none rose more than “Mergers.” In fact, respondents expect it to have an even higher impact next year then it did in 2010 when the industry was dealing with the fallout of huge mergers like Pfizer and Wyeth. It can be unsettling to work in an environment when you know your company could be sold at any time, but that is exactly what today’s product manager is faced with.

As always, we are incredibly grateful to everyone who took time out of their hectic schedules to complete our online survey, which was conducted over a six week period between May and June 2014 by Litchfield Research. We received responses from more than 220 people from all over the pharma and medical device industries (see the tab below for a full list of respondents’ companies). And based on their responses we were able to put together this comprehensive examination of today’s product manager.

Industry Breakdown

While most of the respondents to our survey hail from pharma (68%), we still captured insights from a full spectrum of product managers in the life sciences including biotech (16%), medical device (11%) as well as a few individuals from diagnostics, dermo-cosmetics, OTCs and, of course, those who work with both drugs and devices. And just like last year, the plurality of our respondents work for one of the 10 largest companies in their sector (Figure 1). Going a bit further, more than half (57%) work for a top 20 company while 14% are somewhere below that but still in the top 50. And, as usual, about 30% of respondents work at a boutique-sized company.

Brand Experience

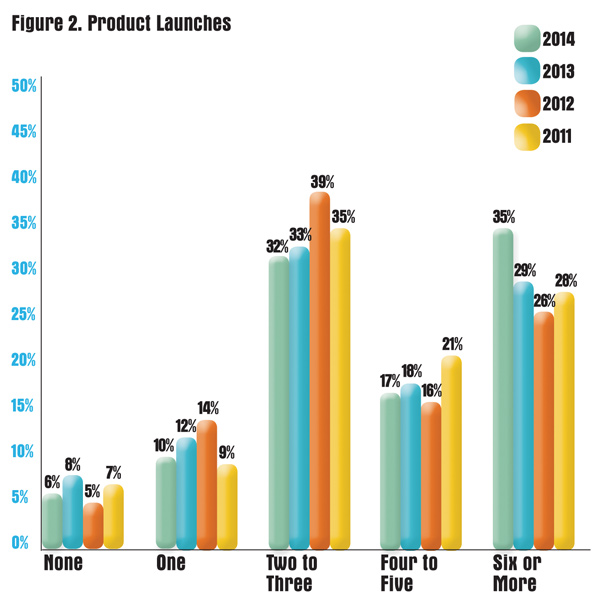

This year’s average respondent may have a few more gray hairs than in previous years—they have spent about three more years in the industry (18 years compared to 15 in both 2013 and 2012). However, they have handled about the same amount of brands in their careers (14 versus 13). And yet, another sign that this year’s crop may contain a few more veterans is the fact that 35% have worked on six or more product launches in their career—a new high for our survey (Figure 2). Furthermore, this six-percentage point increase was achieved through only slight decreases in all of the other product launch ranges we asked about, so the mean number of brands worked on also reached a new high—3.8.

Not only are these respondents more experienced within the industry as a whole, they also appear to be company stalwarts. The average years spent with their current employer increased from 7.3 to 7.8 with small increases in those who have been with their current company for 11 to 15 years (19% vs. 16%) and more than 16 years (11% vs. 10%). Their companies also trust them with more money—15% are given sign off power of up to $501,000 for individual initiatives. Only 7% were allotted that amount of trust last year.

Salary

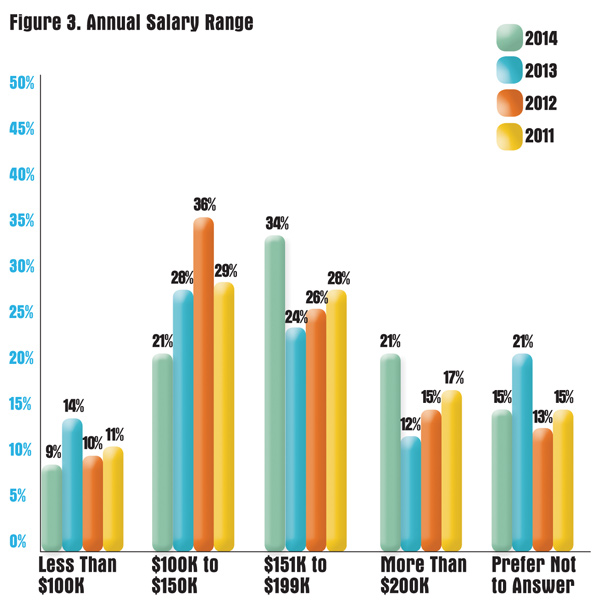

With greater experience comes a higher salary. The fact that our respondents have been in the industry a little longer has paid off as reported salaries are up (Figure 3). We had big gains in those making between $151,000 and $199,000 (a 10% increase) and those making more than $200,000 (up 9%). This is also the first time since 2010 that we have seen gains in those two salary ranges and both represent new highs in the five-year history of the survey. That also means that the average salary of respondents has reached a new height: $155,000—up from $108,200 the previous year. Reading that should put a smile on anyone’s face who works in this industry.

Satisfaction

Apparently more money is not enough to improve job satisfaction (Figure 4). Not only are respondents equally as satisfied with their salary as last year, but satisfaction levels are practically the same across the board. We asked respondents to rate their satisfaction levels on a scale of 7 (very satisfied) to 1 (unsatisfied). As always, relationships with their bosses ranked very highly (62% rated it as a 6 or 7 in 2014 vs. 64% last year), and just over half (53% vs. 54%) are pleased with their current position overall. Respondents also didn’t hesitate to pay tribute to their brand teams (50% give theirs a high rating—up 3% from last year).

At the other end of the spectrum, respondents were least satisfied with their resources (budget, sales support, etc.) as 25% rated it as a 3 or lower (the same as last year). However, 2013’s respondents were most frustrated with their company’s regulatory environment as 29% give it a poor rating. This year, only 21% wanted to pull their hair out at the thought of the process, so there was at least improvement in one area of respondents’ jobs.

Resources

Last year’s group of product managers turned to digital resources for the info they need to manager their careers, but this year’s respondents went in the other direction. We asked them to rate their career information sources on a scale of 7 (extremely important) to 1 (unimportant), and print industry magazines emerged as their go-to resource with 37% rating it as a 6 or 7. Social media took last year’s top spot, but it dropped by 10% this year. Similarly, mobile apps (26% last year vs. 17% this year), blogs (22% vs. 15%), online magazines (20% vs. 16%) and eNewsletters (36% vs. 32%) all took hits. This is a little surprising considering the growth of digital channels and the shift in how most people consume their news, but it may be a reflection of the more “experienced” respondents we seemed to have received this year. Perhaps, this old guard is still reliant or more comfortable with traditional media, or respondents were just not pleased with the quality of info they found in digital channels last year and decided to switch back.

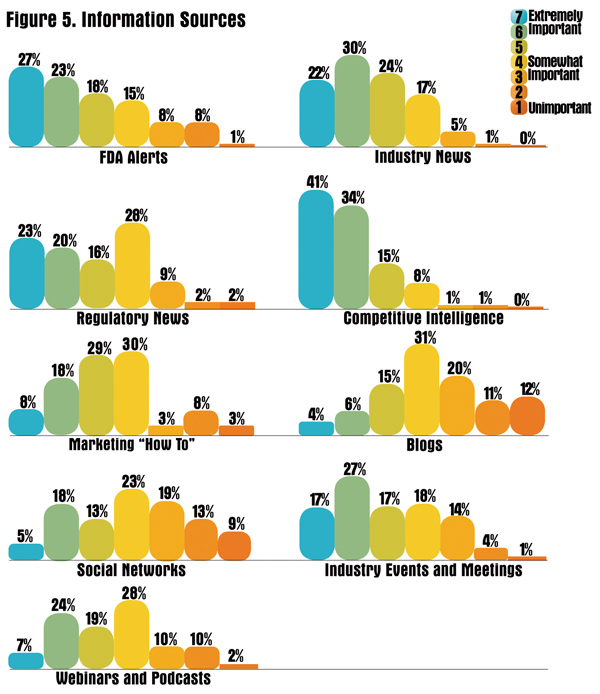

Marketers were also asked to rate the info they rely on to manage their brands on that same 7-to-1 scale (Figure 5). Competitive intelligence once again came out ahead with 75% giving it high marks (compared to 79% last year). Industry news remained in the second spot, but FDA alerts overcame regulatory news for the third most important resource to a product manager’s heart. Once again, social networks and blogs were considered to be the least important resources, which is once again a tad surprising. Just as we keep hearing about people who are turning to smartphones and tablets for their news, we are also treated to stories about more marketers using social media listening to monitor the perception of their brands online. However, that does not appear to be the case among this group of respondents.

Successes

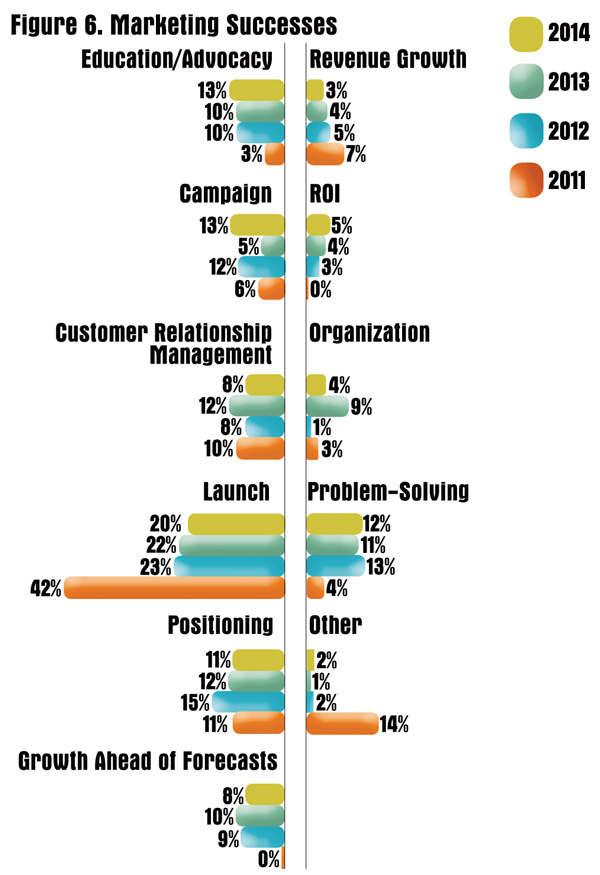

It is always fun to look back and reflect on your greatest marketing achievement (even if you just want to put a smile on your face at a time when you are struggling). And this year, the plurality of respondents, once again, chose to look favorably on a successful product launch—after all what could be more satisfying for a marketer than getting a brand started off on the right foot (Figure 6). Still, respondents’ answers varied quite a bit as only 20% named that as their top achievement. Crafting a particularly successful campaign also ranked highly this year (especially compared to last year when only 5% of people named it). In fact, it was co-runner up along with educating patients, which also saw a small gain in responses over last year (13% vs. 10%). And considering how every company likes to preach patient centricity these days it should come as a shock to no one that more marketers were pleased with their advocacy efforts.

Problem-solving (cleverly navigating a difficult regulatory, resource or other constraint) and repositioning or re-launching a product to improve performance were also among the top success stories that respondents like to brag about. Meanwhile, providing better organization by setting up internal programs/systems/people dropped to the bottom three of responses after seeing a large increase in responses last year. Our respondents also named things like “building lifecycle management strategies,” “influencing clinical practice guidelines” and “mentorship and career growth for my teams” as their fondest achievements.

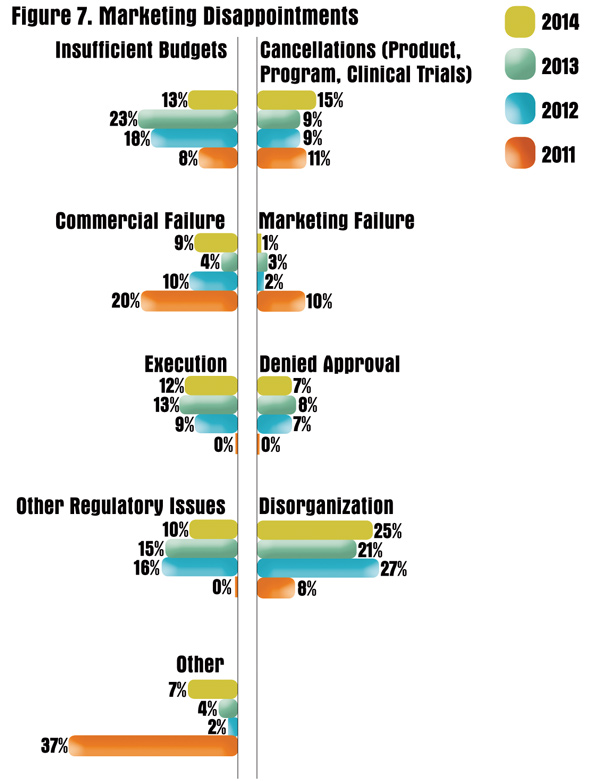

Disappointments

It can be just as productive, though not always as pleasant, to reflect back on your greatest failure and recall the lessons learned from that disappointment. This year, one-fourth of respondents were most disappointed by a lack of organization or the internal miscommunication, red tape, delays, reversals, etc. that can destroy viable market opportunities (Figure 7). Meanwhile, 15% of respondents had to deal with flat out cancellations of their product or program—up from 9% last year. In other words, the plurality of respondents were disappointed by their ability (or inability) to get a project off the ground. On a positive note, two perennial sources of disappointments: Insufficient budgets (down 10%) and regulatory issues such as delays and requests for more data (down 5%) were not considered as much of a cause for failure this year.

On a less positive note, the amount of respondents who had to suffer through a product or program that was introduced but failed because of poor positioning or competition increased by 5%. Other respondents named things like an “inability to instill cross brand customer experience as a valuable activity,” “managed care coverage,” “manufacturing challenges,” “not launching a product because of pricing concerns in another country” and “poor team dynamics” as the greatest cause of their current ulcers.

Influences

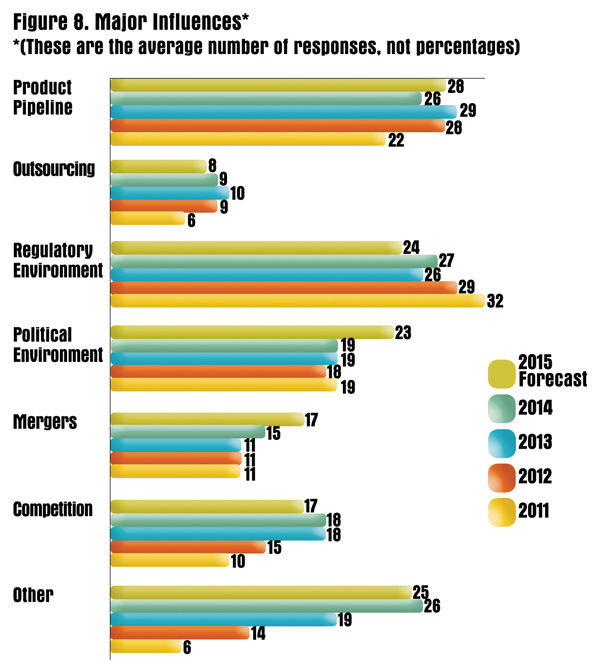

The pharma industry has been making deals left and right lately. Not only are U.S.-based companies looking to merge with an overseas company to take advantage of a friendlier tax structure (such as AbbVie’s acquisition of Shire) but companies are also trading assets (such as GlaxoSmithKline swapping their cancer drugs for Novartis’ vaccines business). While mergers are nothing new in pharma, our respondents are starting to feel the repercussions like never before. Every year, we ask respondents to rate the factors that will have the most impact on the industry (Figure 8). And every year since 2011, “Mergers” has been rated as an 11. We also ask respondents to forecast the factors that will have the greatest impact the following year, and our 2013 respondents predicted that mergers would have a similar impact in 2014 by rating it as a 10. Well, they were wrong.

Of all the factors we ask about, the impact from mergers increased the most over last year as it was bumped up to a 15. And our respondents expect there to be even more dealing in 2015 as they are rating it as a 17 for the coming the year. That would be the highest impact for mergers since 2010 when it was rated as 16. And of course, that was after a crazy 2009 when we saw Pfizer take over Wyeth, Merck & Co. acquire Schering-Plough, and Roche take control of Genentech. Pfizer has already tried to make a similar earthshaking move this year with its failed attempt to acquire AstraZeneca. Also, as stated above, AbbVie is set to acquire Shire while earlier this year Actavis acquired Forest Laboratories. Still, we have yet to see a deal of the same magnitude as those 2009 deals, but you never know what could happen when you wake up tomorrow. And it is certainly on the mind of our respondents as they go to sleep each night.

Besides mergers, 2014 played out similarly to 2013. Concerns over product pipelines dissipated a bit, dropping from 29 to 26, and the regulatory environment retook its place as the industry’s top influencer; however, its rating was virtually the same as the previous year (27 vs. 26). Meanwhile, several respondents named managed care, market access, payer influence and the reimbursement environment as major influencers this year. In fact, many respondents named those same factors as major influencers to look out for next year. It is clear everyone is still adjusting to the effects of the ACA and the shift to an outcomes-based system in which it is more important than ever to provide a value proposition for your brand that demonstrates how it benefits all of the stakeholders involved (patients, payers and providers). And with the midterm elections set for later this year, our respondents also foresee a larger impact from the political environment next year.

Lifecycle

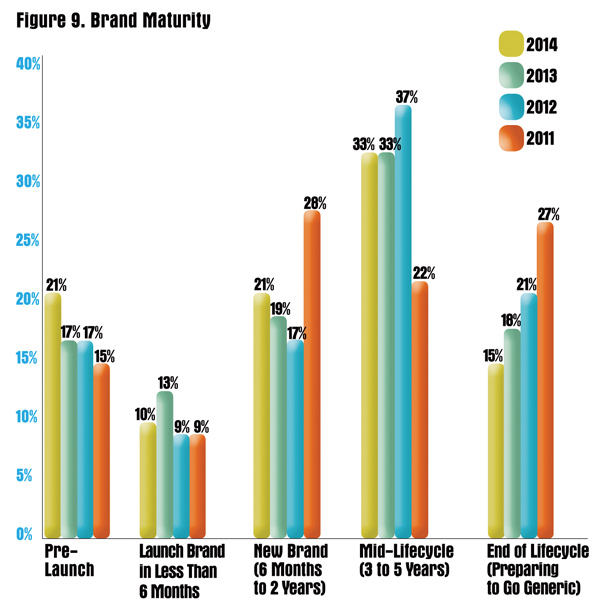

For the first time since 2011, more respondents are working with brands that are still in the early stages of their lifecycle rather than nearing the end of it (Figure 9). Albeit, there is a very small margin between the two as 52% are somewhere between pre-launch and two years while 48% are somewhere between three years and patent expiration, but I am sure if you ask anyone in this industry they would take that as a positive. Considering one respondent even named “overly conservative R&D for the past 10 years” as the biggest influence on the industry as an answer to our previous question, it is nice to see there are some new drugs on the horizon. On a less positive note, the market share of our respondents’ brands did take a small hit. Only 13% of respondents reported a decrease in market share in 2013; this year that number inches up to 16%.

Attributes

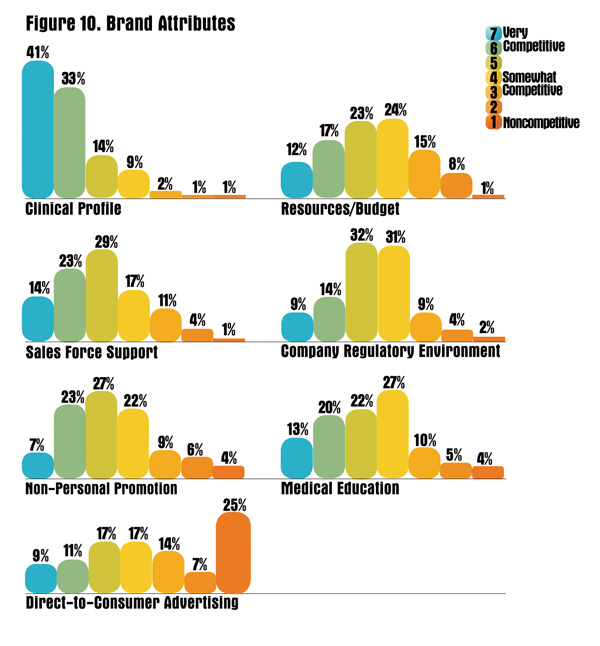

Despite the decrease in market share, on average respondents are only facing 4.3 direct competitors to their brands (which is down from 6.4 last year but on par with the amount reported in 2011). Furthermore, the decrease in direct competitors has not made marketers any more confident about how their brand stacks up. In fact, only 60% feel good about their brand’s chances against its fiercest competitor—down from 66% last year.

Respondents also have lost a little faith in their brand’s individual attributes (Figure 10). We asked respondents to rate various attributes of their brand on a scale from 7 (very competitive) to 1 (not competitive at all) and, as always, a brand’s clinical profile remains its strongest attribute. In fact, 74% rated it as a 6 or 7 compared to just 68% last year. However, all of the other attributes either took a hit in confidence levels or drew even. After rising last year, both sales force support (a drop of 5% in ratings of 6 or 7) and company regulatory environment (a 4% drop) are viewed as less competitive compared to last year. A brand’s direct-to-consumer efforts and non-personal promotion were also perceived as weaker as both received 5% more ratings of a 3 or lower. Meanwhile, both resources/budget and medical education are on par with 2013’s levels.

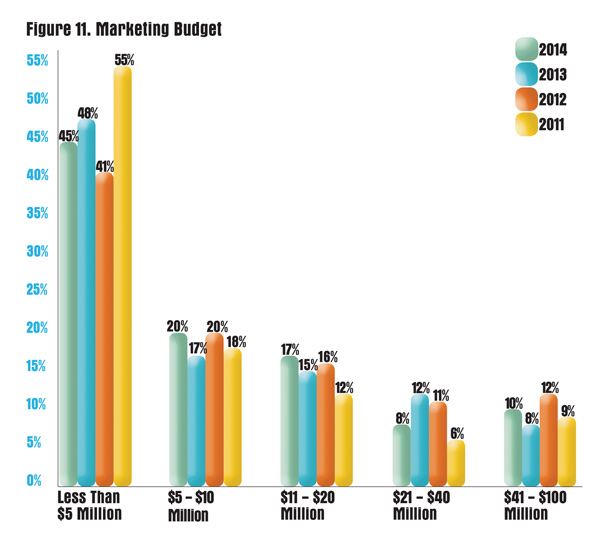

Budget Allocation

Marketing budgets have remained fairly stagnant compared to last year (Figure 11). In fact, the average budget of $14.7 million is up just a tick from last year’s $14.03, but still down from 2012’s nearly $17 million. And yet despite the relatively unchanged budgets only 48% feel that they are given enough money to remain competitive—a 7% drop from last year.

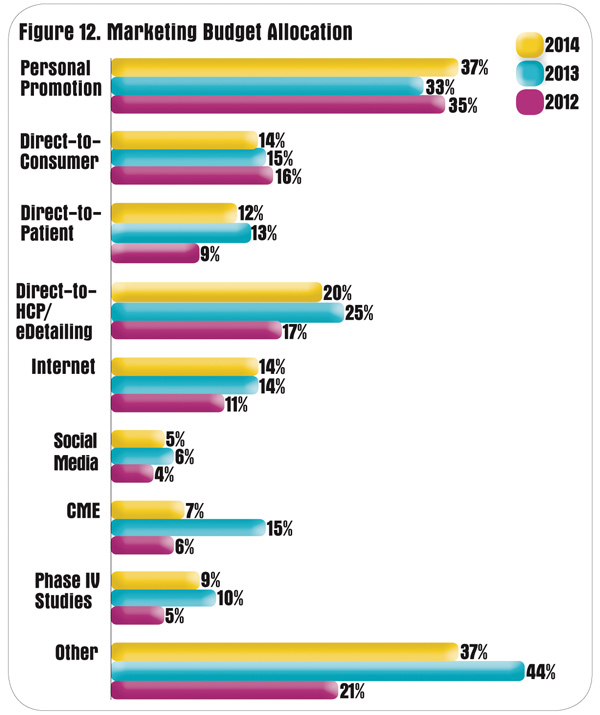

There has also been little change in how marketers are allocating their budgets, save for two decreases worth pointing out (Figure 12). CME spending dropped 8% to just above the level it was at in 2012. The Accreditation Council for Continuing Medical Education (ACCME) recently released a study of its own that showed while commercial support for ACCME-accredited providers decreased for the fifth straight year, it only dropped by 2% between 2013 and 2012—an improvement on the 10% drop between 2012 and 2011. One of the reasons for the relatively small drop last year could be because CME spending was actually made exempt from Sunshine Act reporting. Our 2013 respondents may have been responding to this exemption when they decided to increase their spend in CME, but it wouldn’t explain the drop off this year. However, the Centers for Medicare and Medicaid Services (CMS) is now proposing to eliminate that exemption, so it will be interesting to see how CME spending is affected next year if the proposal passes.

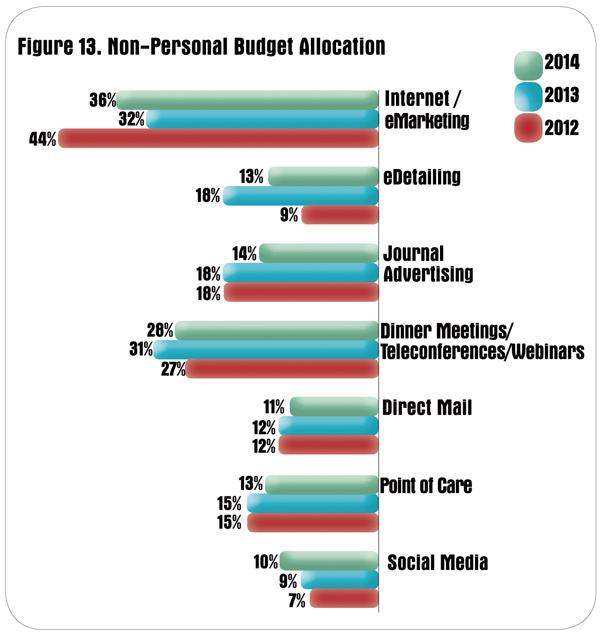

The other notable drop was a 5% decrease in direct-to-HCP/eDetailing, which has gone up the past few years as marketers try to find alternate ways to reach “no-see” physicians. eDetailing also dropped 5% when looking solely at non-personal promotion spending (Figure 13).

In fact, every NPP category dropped at least a little except for Internet/eMarketing, which rose by 4%. Perhaps, marketers are just turning to different digital channels to reach HCPs.

Budget Changes

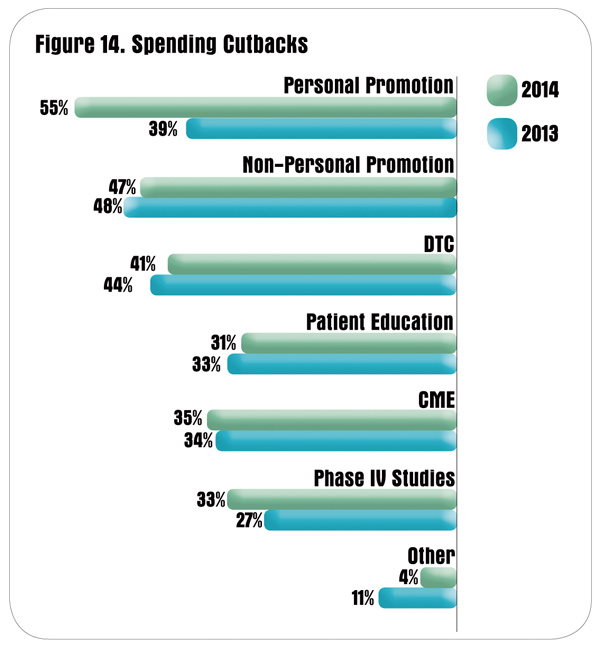

For the second year in a row, slightly fewer respondents have had their budgets slashed: Over the last three years the number has dropped from 42% to 40% to 36%. It may not be a significant margin, but it is certainly better than a trend in the opposite direction. And the plurality of respondents actually experienced a little give and take as they saw their budgets both increase and decrease over the last year. Fortunately for those on just the take side of that equation—the rate of the cuts hasn’t changed since last year’s 20%. What has changed is where marketers are deciding to implement those cuts (Figure 14).

Of our respondents who had their budgets cut, over half decided to take something away from personal promotion. That is a big change from last year when only 39% made cuts to that area. Of course, personal promotion always seemed like it would be a popular place to cut considering how much we hear about the increasing difficulty of reaching doctors as well as the never-ending reduction of sales forces across the industry. But this is the first time the survey has actually matched that perception. Both non-personal promotion and DTC remained the other most likely fatalities, while respondents were also a little more willing to take away money from Phase IV studies and slightly less likely to reduce patient education.

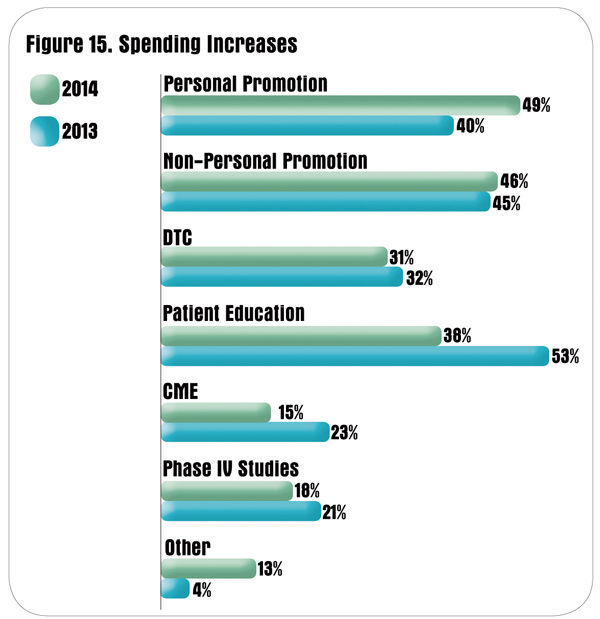

Practically the same number of respondents was lucky enough to receive a budget hike as last year (29% in 2014 vs. 28% in 2013), but the rate of that increase changed dramatically. The average bump in 2012 was 26%, in 2013 it was 30%, this year it was 46%. And the recipient of most of that extra cash just so happens to be personal promotion (Figure 15). So if product managers have the cash, then they are looking to give their sales forces all of the advantages that they possibly can. They are also willing to play both sides of the coin as a hefty portion of their windfalls is going to non-personal promotion. The biggest difference over last year is in the decrease of extra funds going to patient education, so perhaps this year’s crop of respondents is a tad less patient centric (despite the increase in those bragging about their advocacy efforts). Or they are just trying to revitalize their approach to physicians at a time when so many are struggling to reach them. Other respondents said that they are using their increased budget to improve areas such as KOL development, market research and disease education.

Sales Force and Sampling

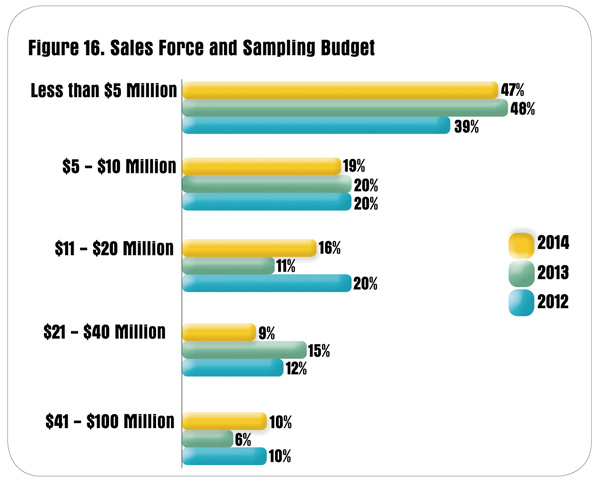

All of that extra cash going to personal promotion means that sales force and sampling budgets are actually up over last year (Figure 16). In fact, the average budget is nearly $2 million higher as it increased from $13.1 million last year to $14.9 million this year. That includes a 4% increase in those with a top tier budget in the $41 to $100 million range. Despite the increase in overall budgets, more respondents actually reported having their sales force and sampling budgets cut this year compared to 2013 (62% vs. 59%). The decrease of those budgets was also higher as this year’s respondents saw an average cut of 18% compared to 16% in 2013. However, those with an increased budget also got a larger hike—it increased from 17% to 21%.

Last year when budgets were lower and fewer respondents actually had to deal with a reduced budget, more than half (54%) of respondents reported that their sales force increased. The same cannot be said this year, despite the rise in budgets. Instead just over half of respondents (51%) had to reduce their sales forces with an average cut of 16% (which is lower than last year’s 19%). Meanwhile, the average rate of increase for the 49% with a larger sales force was 17% (compared to 18% in 2013).

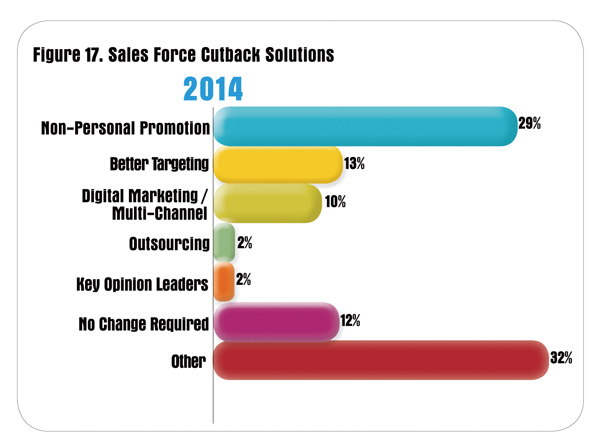

As we have seen for the past couple of years, when sales forces are cut most respondents turn to non-personal promotion (Figure 17). In fact, the key for most respondents is to simply find an alternate approach to reach HCPs, including such NPP tactics as digital, social, multi-channel marketing, eBlasts, webinars and more. Others choose to focus on better segmenting, with one respondent saying that the access to more data has led to the ability to improve targeting techniques. Additionally, that same respondent says that his company also provides incentives to better performers, which creates a smaller but more effective effort. Another respondent reports that his company has been able to deal with reductions just fine as his company is refocusing on specialty HCPs.

A small minority is having success by beefing up relationships with key opinion leaders. While another small group just decided to outsource the role to another organization. Some of the other more interesting responses include “marketing” more, focusing on payers, more focused account management and simply trying to make the most of what they are given and using past successes as examples to their customers. Unfortunately, not everyone is finding a way to cope as one respondent is finding it very challenging to overcome sales force reduction as other resources have been cut as well.

What’s On the Horizon

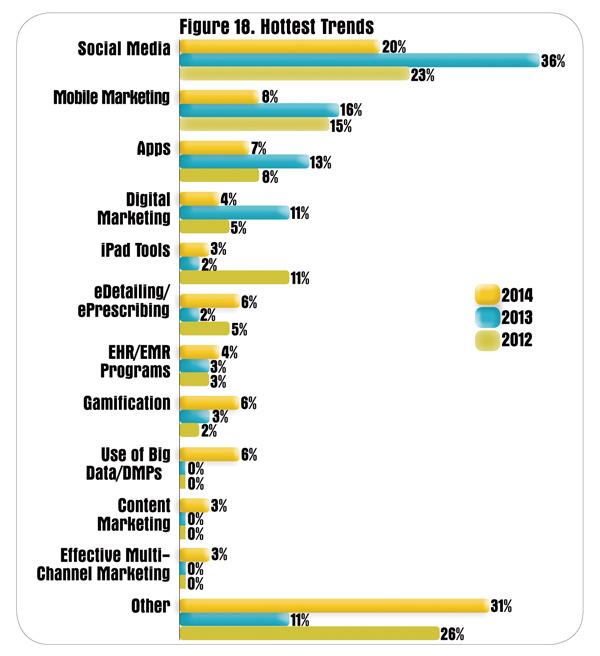

Social media has been a popular answer to this question since we started asking marketers to name the “hottest new marketing trend” in 2010, but it appears they are finally tiring of saying the same thing year in and year out (Figure 18). Or, four years is just too long to continue to consider something “new.” Still, 20% did name social media as their top choice—which bests every category except for the mostly one-off responses grouped together in “Other”—so some marketers are still anxiously waiting for the day when either they feel safe to jump into social media or they see it has finally delivered on its initial promise. However, 20% is also the lowest of the number of responses for social media in the history of the survey. And as one respondent so elegantly put it, “There is nothing trendy recently. Social media? Yawn.” While many share his opinion on social media, a few do believe there are exciting new things on the horizon.

The biggest trend to emerge out of this year’s survey has been “Big Data,” which obviously isn’t new if you have been paying attention for the past year, but finding a way to use this data has become a point of focus for some of our respondents. Specifically, one respondent mentioned using content management system (CMS) platforms, data management platforms (DMPs) and analytics integration to optimize consumer/patient experience and increase acquisition/retention. Another wants to work to improve DMP targeting for mobile and tablets where it is not as well developed as desktops.

Meanwhile, mobile, apps and digital marketing (the second, third and fourth most popular responses in 2013, respectively) were all mentioned far less this year. Maybe the simple fact that marketers feel a little safer working in those areas than in social media makes it easier for them to stop considering those channels as new, but there were a couple of interesting responses for these areas. Several respondents mentioned developing apps or other technologies that can help with the self-management of conditions and allow patients to take control of their health. Others like the idea of starting to take advantage of the GPS in people’s smartphones. One person mentioned doing digital advertising on smartphones that link behavioral dynamics to geo-targeted locations. For example a notice that, “Your favorite brand of soda is on sale at 7-Eleven at the next intersection.”

Some of the other interesting trends brought up include using eDetailing to target physician support staff, programmatic buying, offering a real value proposition to customers (from their point of view—not just the manufacturer’s point of view), partnering with payers, and market access strategies that include integrated delivery networks and Medicare administrative contractors. One more thing to keep an eye on: Mergers and acquisitions among wholesalers/specialty distributors, pharmacy benefit managers, etc.

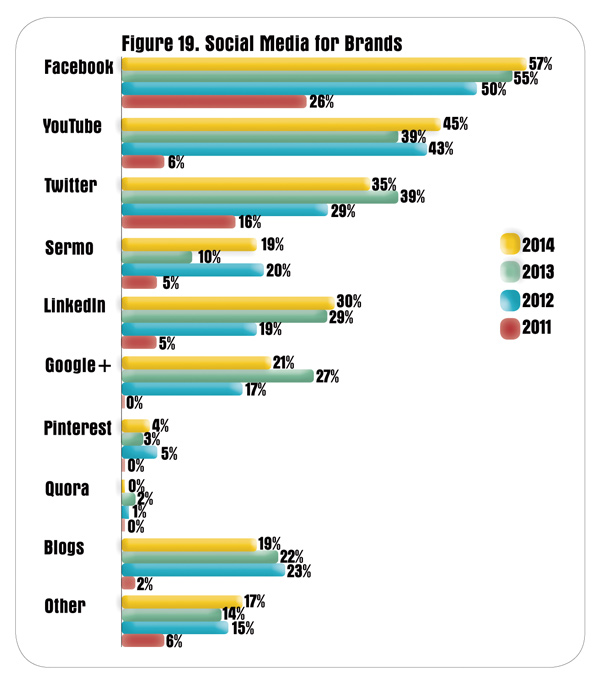

Social Media Use

The much-anticipated FDA guidance on social media finally showed up on marketers’ doorsteps this year and yet it doesn’t appear that much has changed in the use of social media for brands (Figure 19). To be fair, the guidelines so far have come in the form of three draft guidances that only cover a portion of what marketers may do on social media, including postmarketing submissions of interactive promotional media, Internet/social media platforms with character space limitations, and correcting independent third-party misinformation online. To be even fairer, two of those guidances arrived in June, when the survey was being conducted, so they wouldn’t have any effect on the actual use of social media. But you would imagine that they might affect our respondents’ perceived use of social media for next year. However, that does not appear to be the case either.

Only 67% believe that social media use by pharma and medical device marketers will increase next year—that is the lowest total ever. In fact, only once before has that figure ever dipped below 80% (when it was slightly below that at 76% in 2012). Meanwhile, 7% think it will decrease (which is also a new high) and 26% simply expect it to remain the same. For the most part, nothing in the three guidances really threw marketers for a loop. In fact, the guidelines mostly aligned with what marketers figured the FDA would come up with—they just confirmed that was the case. It is hard to say whether the guidelines had any effect on our respondents’ lack of expectation for more social media growth. Maybe some were discouraged by them or the fact there hasn’t been something a little more comprehensive to this point. Or maybe there are just simply fewer places where social media can grow.

As we saw last year, people grew tired of waiting for the FDA and marketers just decided to jump in. Between 2012 and 2013 there were large increases in the use of Twitter, Google+ and LinkedIn. At this point, maybe the only people left on the sidelines are those who waited for the FDA to tell them exactly what they expect from marketers. Also, it is important to note that even those who do use social media have struggled to demonstrate the all-important ROI, which can make it difficult for the higher-ups to approve new social media initiatives. So there is less incentive for even the veterans in this space to ramp up their presence. All in all, we may just see small increases in social media use next year, similar to this year’s results with Facebook (up 2%), YouTube (up 6%) and Sermo (up 9%).

Thanks To Our Respondents From These Companies:

Abbott Laboratories

Abbott Vascular Devices

AbbVie

Acorda Therapeutics

Aesculap, Inc.

Agfa HealthCare

Alcon Laboratories, Inc.

Alexion Pharmaceuticals, Inc.

Allergan, Inc.

Amgen, Inc.

Antares Pharma, Inc.

Apotex Corp.

Astellas Pharma

AstraZeneca

Bayer HealthCare

Biogen Idec

Biomedical Systems

Boehringer Ingelheim

Breckenridge Pharmaceutical, Inc.

Bristol-Myers Squibb

Cadence Pharmaceuticals

Celgene

Cornerstone Therapeutics Inc.

CryoLife

CSL Behring

Cubist Pharmaceuticals, Inc.

Daiichi Sankyo

Dentsply Professional

DUSA Pharmaceuticals

Edwards Lifesciences

Eli Lilly and Company

EMD Serono

FemmePharma Global Healthcare

Ferndale Healthcare

Ferring Pharmaceuticals

Forest Laboratories, Inc.

Galderma Laboratories, L.P.

Genentech

Genzyme

George King Bio-Medical, Inc.

GlaxoSmithKline

Global Pharmaceuticals

Grifols, Inc.

Henry Schein, Inc.

Impax Laboratories

Ipsen

Janssen Pharmaceuticals, Inc.

Johnson & Johnson

MAQUET Cardiovascular

McNeil Consumer

Medimmune, Inc.

MEDIpoint, Inc.

Medtronic Neurological

Merck

Momenta Pharmaceuticals

Nicox

Novartis

Novo Nordisk

Nutricia

Onyx Pharmaceuticals

Otsuka

Pack Pharma

Palatin Technologies

Pfizer

Pierre Fabre Laboratories

Purdue Pharma

Ranbaxy

Regeneron

Salix

Sandoz, Inc.

Sanofi

Sanofi Pasteur

Santarus, Inc.

Shionogi

Shire Pharmaceuticals

Sunovion

Takeda Pharmaceuticals, Inc.

Talecris Biotherapeutics

Teva

UCB

Valeritas

Watson Pharmaceuticals