Product managers, as their name suggests, have always been focused on marketing their products. But in 2013 we have seen that focus move away from product-centric marketers and toward patient-centric marketers. The results of our 5th annual Product Manager Survey display that trend in full force. Marketers are devoting more of their budgets and time toward Direct-to-Patient initiatives, patient education and partnering with patient advocacy groups. Today’s product manager has truly put the patient at the forefront.

For years, pharma has been reluctant to engage with social media due to the lack of guidelines from the FDA—which still haven’t arrived—but this year our respondents reported an increase of social media use for their brands across the board. The use of Facebook, Twitter, LinkedIn and Google+ all rose from 2012 (a year in which social media use saw a pretty sizeable jump as well). But the waiting finally seems to be over. Perhaps, this has a little something to do with the new product manager—the patient-centric product manager. After all, millions of patients are looking up info or discussing their diseases and treatment options online, so how can pharma afford not to find a way to be a part of these discussions?

Those aren’t the only challenges that today’s product manager has faced and found a way to overcome. In 2013, marketers are forced to work with smaller budgets and on more brands while dealing with staff downsizings and facing more no-see physicians. One positive—and a surprising bit of news—despite a consistent stream of reports from pharma companies about reduced sales forces, more than half of our respondents are actually working with an increased sales force from last year. And even those who aren’t have found creative solutions to compensate for the losses. Marketers have also taken more pride in improving their company’s internal organization, the No. 1 named achievement of 2013, as they find better ways to get the most out of their brand team and company.

We are incredibly grateful to every one of the marketers who took the time to respond to our online survey, which was conducted over a five week period between May and June 2013 by Litchfield Research. We received responses from over 230 people from all over pharma including Pfizer, Merck, Bristol-Myers Squibb and AstraZeneca (see the “Thanks to participating companies” tab for the other respondents’ companies). And thanks to them we have a comprehensive examination of influential factors to look out for in 2014, sales force cutback solutions, the hottest new marketing trends, and more.

Industry Breakdown

From large companies to small, pharma to medical device, marketing to sales and newbies to veterans, our survey of product managers presents a varied yet full 360-degree examination of the industry. While seven out of 10 respondents come from pharma, another 18% work in biotech and 9% are employed at a medical device company. Of course, some of our respondents made sure to indicate that their company did all three (or at least some combination of those three). They fell into the 4% who choose “Other” as their industry of employment, along with people at diagnostics and medical supplies companies.

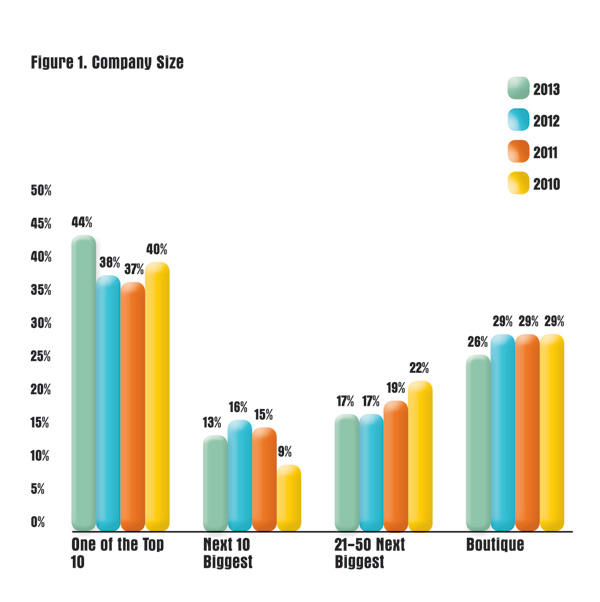

However, this year our responses are a tad more top heavy. When it comes to the size of the companies where respondents work, 44% are at one of the top 10 in their respective industry compared to 38% in the previous year (Figure 1). In all, nearly 60% are at one of the 20 largest companies in their sector, with the smaller companies also well represented as 26% of respondents work at a boutique-sized company.

Brand Experience

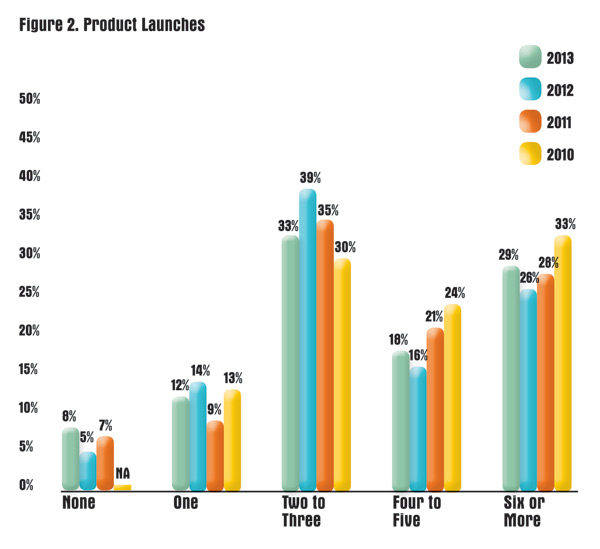

Just as last year, the average respondent has worked in the industry for about 15 years. Yet this year’s crop has worked on an average of 13 brands, compared to the average of 11 last year. That means that 2013’s respondents have worked on the same amount of brands on average as our product managers from 2011, despite the fact that in 2011 the average respondent had been in the industry for an average of 18 years. This could be a sign that companies are requiring a little more of each employee due to the constant cutbacks and staff downsizings. As Figure 2 shows, even the number of product launches that respondents have worked on has slightly increased with 29% working on six or more (up from 26% in 2012) and 18% working on four to five (up from 16%).

The amount of time that respondents have spent with their current employer is also very similar to last year with an average of 7.3 years compared to 7.5 in 2012. However, the number of people who have been with their employer between six and 10 years has increased by 9% while the people in the 11 to 15 range decreased 7%. In terms of their current job titles: 25% are Directors of Marketing, 28% are Product Managers, 5% are Product Directors, 6% are Vice Presidents of Marketing, 4% are eMarketing Managers and 10% work in sales.

Salary

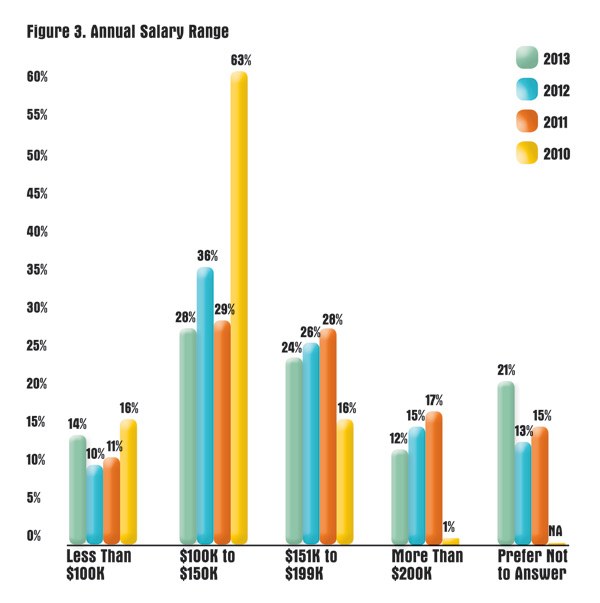

Overall, and perhaps expectedly, salaries are down across the board (Figure 3). The number of people making over $200,000 decreased 3%, those in the $151,000 to $199,000 range are down 2% and even the people making between $100,000 and $150,000 dropped 8%. Of course, that means that the number of people making less than $100,000 had to go up, and up it went by 4%. And to further drive the point home, the mean salary of the respondents from this year is down to $108,200 versus $145,000 last year. That happy boost we saw in 2010 is definitely establishing itself as an outlier.

Satisfaction

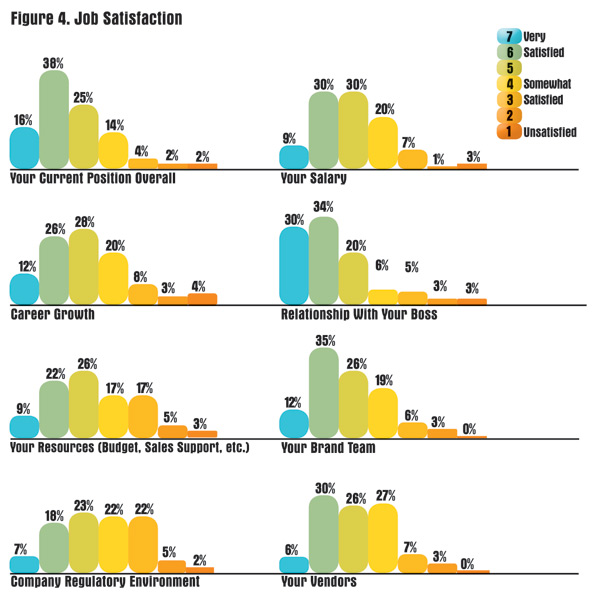

It seems as if the constant downsizing, decreasing salaries and increasing lack of resources is taking a toll on product managers’ job satisfaction. It is down in almost every area we asked about—not drastically mind you—but respondents are a little more willing to express their frustration (Figure 4). We asked respondents to rate their satisfaction levels on a scale of seven (very satisfied) to one (unsatisfied). When it comes to their current position, only 54% rated their satisfaction level as a seven or six compared to 58% last year. Respondents are also a little less pleased with their salaries (39% vs. 45%), career growth opportunities (35% vs. 40%), brand teams (47% vs. 53%) and their company’s regulatory environment (25% vs. 28%). A growing unease about the resources for their brand (budget, sales support, etc.) resulted in a 6% increase of respondents rating this area with a three or lower. But on the bright side, respondents are still very satisfied with their relationship with their boss.

Resources

To get the info they need to help them manage their careers, product managers are increasingly going digital. We asked them to rate their career information sources on a scale of seven (extremely important) to one (unimportant) and social media came out as the top resource with 39% rating it with a seven or a six. Product managers also seem fond of getting their news sent directly to their inboxes with eNewsletters coming in second with 36% rating it as a top resource.

Next up are magazines, both the print version (35%) and digital version of the print magazine (34%). And in what should be a shock to no one, the biggest gainer from last year is mobile apps, which went from 19% rating it as important to 26%. Meanwhile, product managers rated blogs (22%), online magazines (20%) and RSS feeds (12%) as the least important resources for career info. Some respondents went outside the box to name career websites such as Monster, the ever-popular FirstWord Pharma, personal networking and plain old word of mouth as their go-to resources.

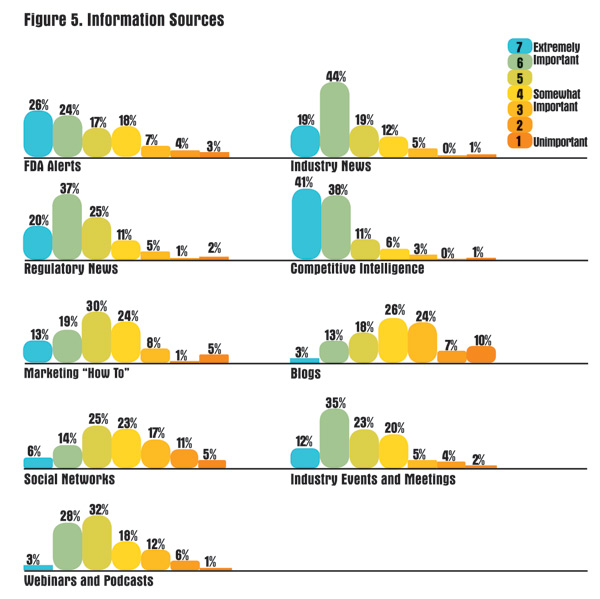

However, not much has changed in terms of the information sources that marketers rely on to manage their brands (Figure 5). We asked marketers to rate these sources on the same seven-to-one scale and once again competitive intelligence was overwhelming (79%) rated as the most important resource. While industry news remained in the second spot, regulatory news took a 6% jump to overcome FDA alerts as the third most important resource. So it seems this current environment is forcing people to keep a closer eye on the latest regulatory updates. Otherwise the bottom five remain in the same order as last year: Industry events and meetings, marketing “how tos,” webinars and podcasts, social networks and blogs.

Successes

No one category of achievement really dominated when our respondents named their greatest marketing success (Figure 6). While launching a new product had the plurality of responses, it was only named by 22% (similar to last year’s 23% but down from the 42% of 2011). Positioning a product to improve its performance remained the runner up (actually it was a co-runner up) yet it dropped by 3% from last year. The co-runner up was customer relationship management, which proved that it is continuing to become more of a focus for pharma marketers as it increased by 4%. But the largest gainer was actually organization or setting up internal programs/systems/people, which jumped 8%. Only three people named organization last year, so not only does it seem that product managers paid more attention to setting up an efficient internal system in 2013, but they also took more pride in their ability to do so. This could be due to the increase of downsizes and the need to restructure brand teams, which may have put a larger priority on finding a way to get the most out of your staff. If you are wondering about that 1% who chose “Other,” a few of our respondents couldn’t single out just one achievement so they went with all of the above.

Disappointments

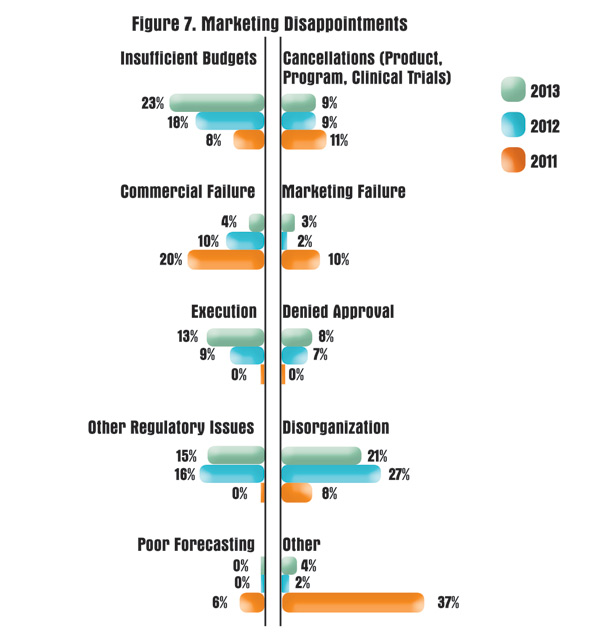

While organization became more of an achievement for our respondents, disorganization that destroyed viable marketing opportunities—including internal miscommunication, red tape, delays, reversals, etc.—actually became less of a source of failure this year, dropping by 6% (Figure 7). However, it was still named by 21% of our respondents, making organization the second highest source of disappointment in 2013. At least that is an improvement over last year when it ranked first. This year that honor belongs to an insufficient budget, which became slightly more of a problem with a 5% increase.

Meanwhile, last year’s number four, commercial failure—in which a product or program failed because of positioning or competition—dropped 6% to near the bottom of the list. It is hard to say what contributed to this decline, but not all marketers felt that their programs were more successful this year. The lack of execution—or when a well-conceived program fails because of delays, internal disagreements, miscommunication or other factors—took over the fourth spot and increased by 4%. Following poor execution are cancellations in which internal decisions were made to terminate a product or program. Considering that three of the top five named disappointments all involved problems with a company’s internal operations, it is not hard to understand why marketers felt such a sense of accomplishment when they were able to make some organizational improvements in their company.

Influences

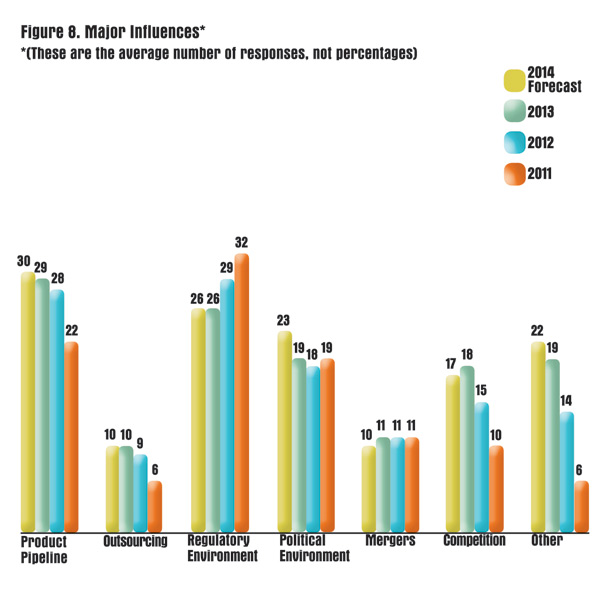

Every year, we ask our respondents to not only name the factors having the most significant impact on the industry in the past year, but to also look ahead and offer their predications for the next year (Figure 8). Well our 2012 respondents must have had one clear (and fully functional) crystal ball because they did a great job of foreseeing what to look out for in 2013.

We give our respondents 100 points to work with and we ask them to assign a value that represents the influence of each of the factors listed so that it adds up to 100 in the end. Last year’s group figured that the product pipeline would have the greatest impact on the industry in 2013 (finally overtaking the regulatory environment’s four year reign) with an average score of 30 points. And lo and behold, our 2013 respondents named it the No. 1 factor with a score of 29. That trend holds true with many of our categories. The regulatory environment was predicted to be at 25 and it came out with a score of 26, outsourcing was 9 vs. 10, and mergers was predicted correctly at 11. That means the only discrepancies involved the political environment and competition from other brands. Our 2012 predictors saw politics making a larger impact at 25, but it only ended up at 19, and competition came out at 18 after a forecast of only 14. So obviously last year’s respondents overestimated the effect that the Affordable Care Act or a potential change in presidents could have on the pharma industry. Of course, much more of the ACA will be implemented in 2014, so it is not a surprise that once again our respondents are predicting that politics will play a larger role in the healthcare industry in the next year. In terms of competition, perhaps product managers just felt the dried-up pipeline would make it a little easier on some brands, but it seems that turned out to be untrue.

Over the past couple of years, respondents have also become more willing to look past the six major factors to look out for that we typically list for them and offer up some of their own. This year that list includes a growing concern over generics, a tendency to only invest in “me too” products, the global economic recession, managed care, payer activism, a reliance on an outdated commercial model, reimbursement cuts and price pressure, as well as the continued shift to multi-channel marketing promotion. All of these factors were also named by our respondents as major influencers to look out for in 2014, along with three additions: Continued recovery and new growth, healthcare reform and a multicultural strategy. Otherwise, our respondents see 2014 playing out very similarly to 2013.

Lifecycle

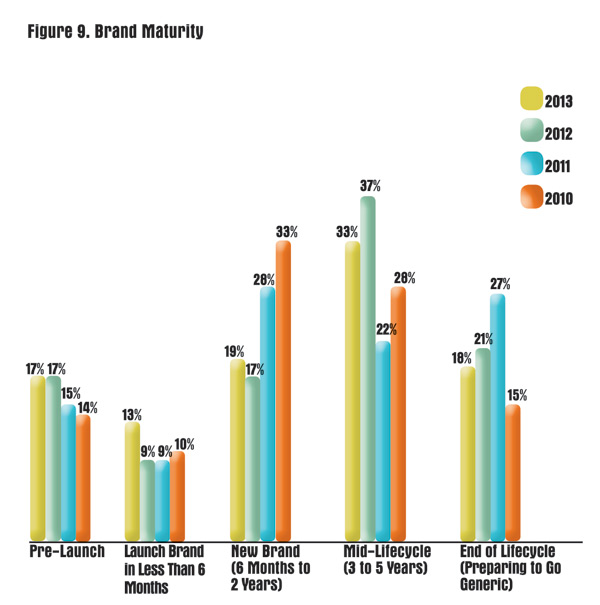

With all the talk of a dry pipeline, it is nice to see that this year’s product managers are getting ready to launch some new blood into the marketplace (Figure 9). Even though the amount of respondents with a brand in the pre-launch phase remains unchanged at 17%, there was a small increase of 4% in the number of people who are about to launch a new product in less than six months. And at 13%, it is also the highest that number has been in four years. There was even a small increase in the new brand category (six months to two years); however, at 19% it is still well below where that figure was in 2011 and 2010. And despite drops in both the mid-lifecycle range (three to five years) and those at the end of their lifecycle, over half of respondents are still approaching the end of their exclusivity window and must prepare to face off against generics.

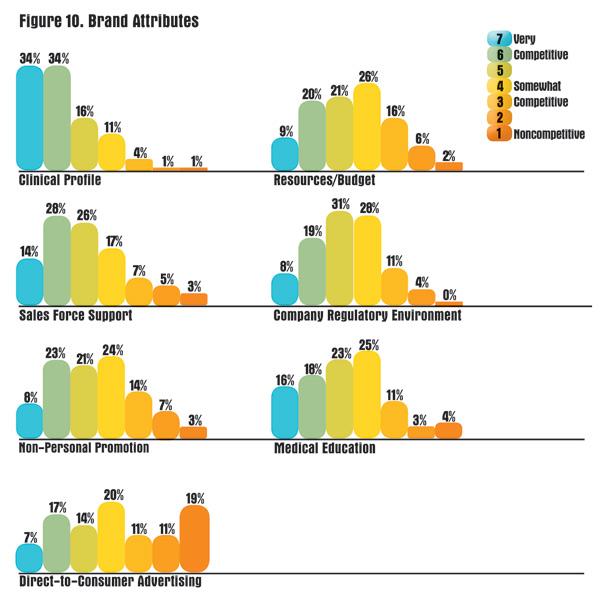

Attributes

Last year, each brand on average faced 6 direct competitors (which tied our high from 2010), and this year that number inched up to 6.4. Yet, two-thirds of respondents still feel good about how their brands stack up against their fiercest competitors.

However, when it comes to each brand’s individual attributes, respondents are a little less satisfied with how they are doing in a few areas (Figure 10). We asked respondents to rate various attributes of their brand on a scale from seven (very competitive) to one (not competitive at all). Somewhat surprisingly, not only did respondents name sales force support as the second most competitive attribute, but their faith in it actually rose with 5% more people rating it as a seven or six. Respondents also felt more confident in their company’s regulatory environment as the number of people who rated it at a three or lower decreased by 13%.

Respondents, however, have become less satisfied with their brand’s resources/budgets as 14% more rated it as a three or lower, and their brand’s DTC efforts as 7% more gave it a low rating.

Budget Allocation

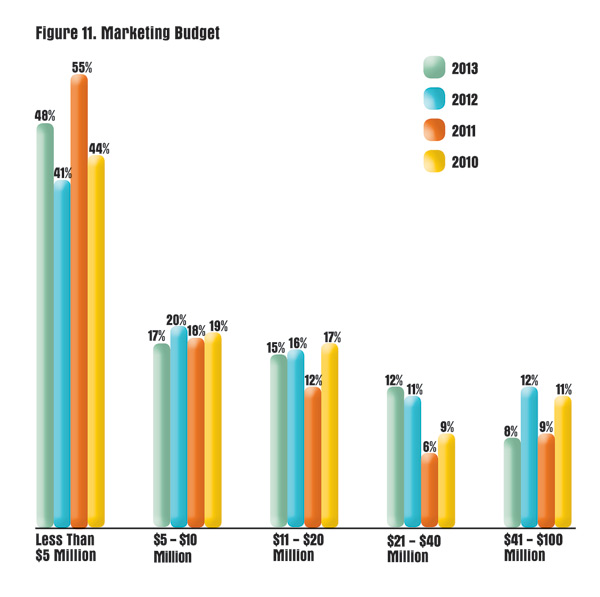

After experiencing an uptick last year, marketing budgets have once again decreased (Figure 11). The average budget of last year’s respondents was $16.9 million, but this year that figure is down to $14.03 million—however, that is still up from the average of $12.7 million in 2011. While there was a 4% drop in the number of people working with a budget between $41 and $100 million, the next two largest budget ranges—$21 to $40 million and $11 to $20 million—remained relatively steady over the past year. However, more people are forced to work with less as witnessed by a 7% increase in those operating with a budget under $5 million. But even with this decline, respondents’ feelings about their ability to stay competitive with their current budget remains unchanged from a year ago. Just over half feel their budget is adequate.

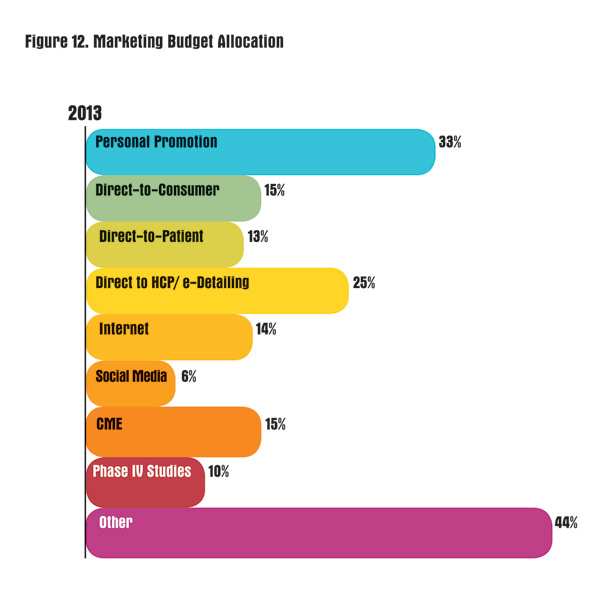

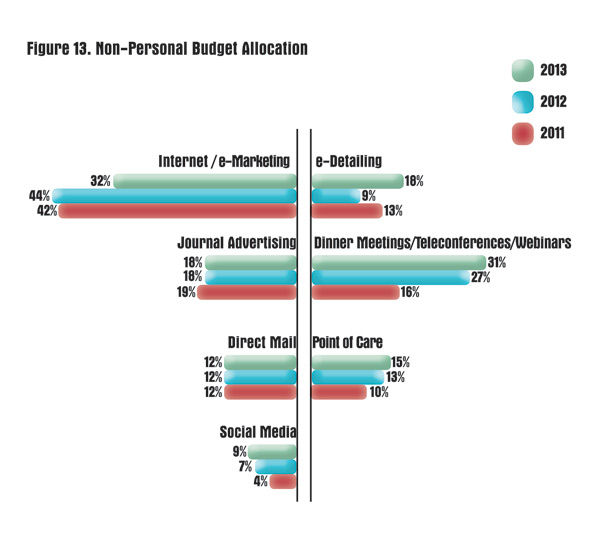

Two recent trends seem to be showing up in how marketers are allocating their budgets: The shift toward patient centricity and the increase of no-see docs (Figure 12). Not only is Direct-to-Patient spending up 4% from last year, but some respondents also said that they are putting more money toward patient advocacy groups. Marketers are also putting more dollars into trying to reach doctors where sales reps can’t. Direct-to-HCP/e-Detailing is up 8%, spending on CME rose 9% and Internet and social media each saw small bumps of 3% and 2%, respectively. This trend also proved true when we asked respondents just about their non-personal promotion spending (Figure 13). While marketers are putting a little less of the NPP pie into Internet/e-Marketing, they have doubled the share that goes into e-Detailing. Point of care marketing and social media marketing also experienced small increases of 2% each.

Budget Changes

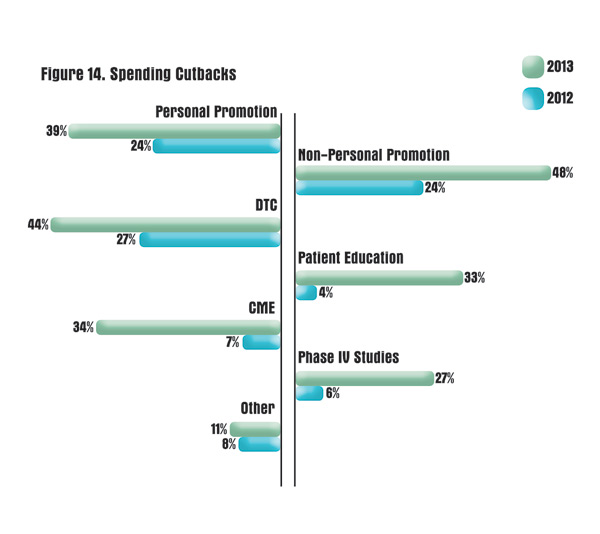

As you have probably heard, companies are slashing marketing budgets left and right, but at least, for now, those cuts have not become any more drastic over the last year. Four in 10 respondents reported that their budgets had been reduced (compared to 42% last year) with an average cut of 20% (compared to 22% a year ago). This year’s most popular cutback was in non-personal promotion, although last year’s whipping boy, DTC, is still losing a large chunk of money when marketers are told that something has to go (Figure 14).

One thing to keep in mind as you review the difference between cuts as displayed in Figure 14: Last year, we only asked respondents to choose the one area where companies were cutting back the most, while this year we let them choose any and every area where spending is being slashed. Even though it is not a true apples-to-apples comparison, you can still examine the rates at which areas are being cut compared to each other. For instance, marketers in both years were a little more resistant to cut Phase IV studies and patient education. Marketers also listed some other areas where they have been forced to cut, including tradeshows, CRM, research and even new innovations.

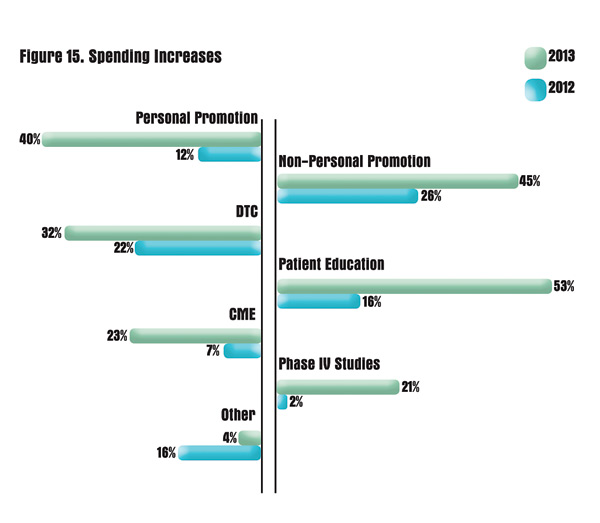

Now for some good news. Nearly three in 10 respondents reported that their budget has grown since last year (compared to 26% in 2012) with an average bump of 30% (versus 26% last year). Where is all of this extra cash going? To patient education, of course (Figure 15). Once again, this is not a true comparison as respondents could select multiple areas worthy of extra spending this time around, but patient education was only the third most popular answer last year. Now, more than half of respondents are making sure to pour more money into it. This is just another example of how the industry is making more of an effort to put the patient at the front and center. Personal promotion also became more of a priority this year, so it would appear marketers are still trying to give as much help as they can to the reps who actually do get in to see the doctor.

Even with the overall decrease in budgets, very few marketers actually saw their brand lose market share. Only 13% experienced any loss in market share while 16% said that it rose considerably for their brand and another 39% said that it was up at least modestly. That leaves 32% who remained at status quo.

Sales Force and Sampling

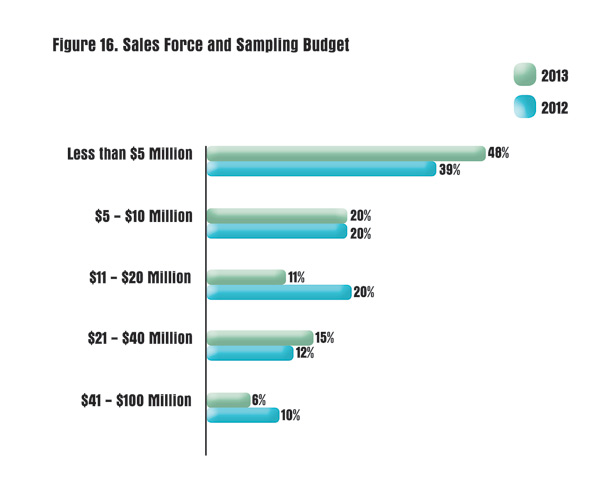

Every day it seems like a new company is announcing a downsizing of its sales forces, so once again we wanted to gain a little insider perspective on how product managers are dealing with these changes. Sales force and sampling budgets are down overall from a year ago (Figure 16) with an average budget of $13.1 million compared to 2012’s average of $15.8 million. There was a 4% decrease in those with a budget in the highest range ($41 to $100 million) and a 9% drop in the mid-range budget of $11 to $20 million. Of course, this also means that more people were forced to work with a budget under $5 million—that range rose by 9%.

Just as last year, about six in 10 respondents said that their sales force and sampling budget was cut. However, the average overall decrease of 16% was a little less than last year’s average of 20%. Shockingly, while budgets going toward sales forces declined, 54% of respondents actually reported that the size of their sales force increased with an average growth of about 18%. This is a complete turnaround from last year when 55% said that the size of their sales force decreased by about 21%. This year—in case you have yet to do the math yourself—only 46% reported a smaller sales force and for those who did the average cutback was 19%. Those respondents who did have to deal with a smaller sales force were kind enough to explain how they managed the reduction.

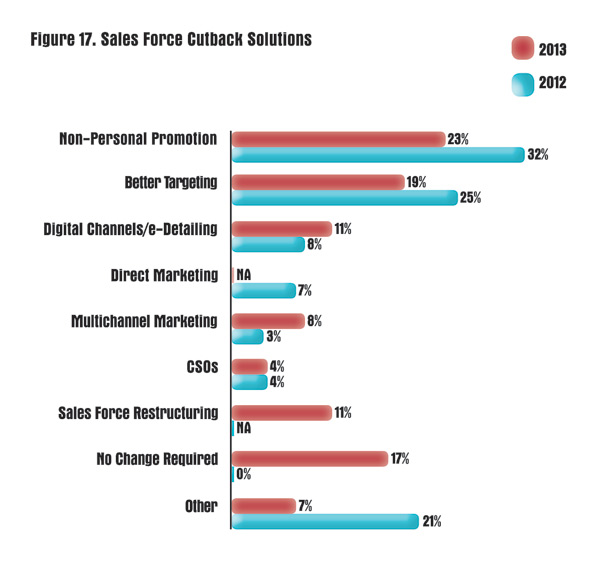

Once again, increasing non-personal promotion was the most named solution to overcome the disadvantages of a smaller sales force, but not by the same margin as last year (Figure 17). Instead there was a little more variance to the tactics mentioned—that and the fact that 17% of respondents said that no change was necessary. Not one person said that last year. A couple of people indicated that it was because their sales force stayed the same, while others said there was no need to make changes because the sales force was now aligned to where it should be for their organization.

Better targeting was also a popular answer, which included strategies such as cutting out trips to secondary cities, a refocusing on top customers, and an emphasis on reducing the frequency but improving the depth of exchange in the sales call. This year, 11% named sales force restructuring or realignment as the way to go, which no one explicitly named last year. For instance, one respondent said that they were reorganizing account managers to focus on top prescribers and leveraging field medical science liaisons and patient call centers to drive increased demand for the product. Other people are exploring alternative channels such as social media, e-Learning/ePromotion, CME and telesales. A select few were outsourcing the responsibilities to CSOs or other organizations.

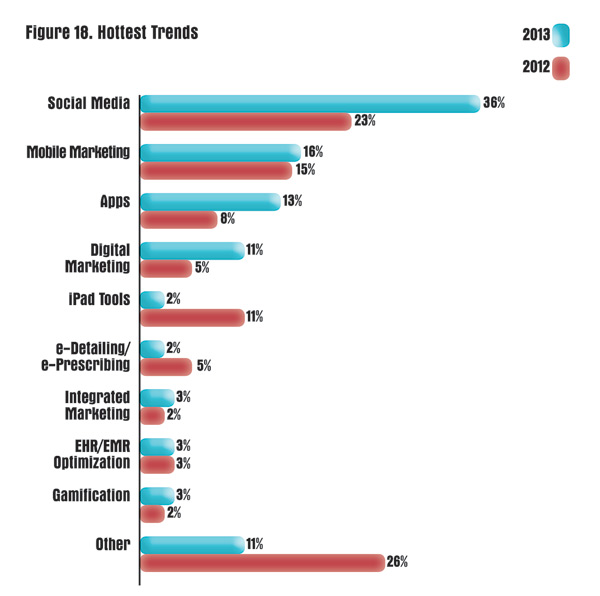

Hottest Marketing Trend

Social media seems to be making a comeback. After only being named by 26% of our respondents last year, social media once again regained the plurality of mentions as the hottest marketing trend with 36% (Figure 18). Even though social media has been around for quite some time now, pharma has yet to truly embrace it—which is why pharma marketers can still refer to it as a hot new thing. So for pharma marketers, this trend is less about what is new with social media and more about how pharma can do it right (while avoiding FDA backlash). Or as one of our respondents put it, “Pharma has yet to tap into [social media] successfully. We need someone to take the leap forward.”

Others feel the focus should be on (and has been on) mobile. “It will continue to be the widespread uptake of smartphones as the next information dissemination and communication platform,” one respondent said. Mobile marketing was named by 16% of our respondents while apps were named by 13%—both highs in the history of this survey. Mobile and apps offer marketers some unique advantages. For instance, as one respondent mentioned, they can be used for real-time mobile promotion and tracking in retail as well as for augmented reality promotional events and convention exhibits. Someone else mentioned using gamification in patient apps that take advantage of HCP insights.

Not everyone was so specific with their responses. One person simply said: “Digital still appears to be the hottest. However it does not seem that anyone has cracked the code so the model is to spread your spend to cover all bases.” People mentioned several digital initiatives that went beyond social and mobile. One respondent said that the industry should take advantage of the commercial space that is available during television and movie content via Internet streaming. There was also one mention of Google Glass, two people said Twitter and others simply said greater customer engagement.

Several brought up new strategies that do not necessarily have anything to do with digital, including focused roundtable ad boards; more outcome-based papers due to healthcare reform; increased Rx to OTC switches; marketing diagnostics along with pharma products; movement marketing; content marketing within a marketing automation framework; contextual targeted marketing; and funding research with the NFP, NGOs and advocacy groups so that pharma can own results within patient populations.

Finally, one respondent reminded us all not to get caught up in what it is the hot new thing. “There is no hot marketing trend. Develop the right products for the right patient situation and then communicate this clearly and simply. The channels of dissemination (social media/Internet/others) are secondary in importance to the former.”

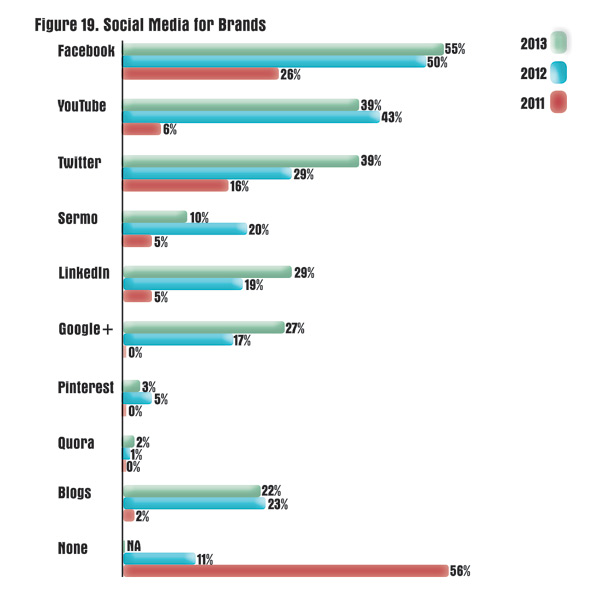

Social Media Use

Last year, only 76% of respondents predicted that social media use would increase over the next year. That was the first time that number ever dipped below 80%, and yet this year’s survey reveals that social media use for marketing has actually increased significantly over last year (Figure 19). Yes, oddly enough the use of YouTube decreased by 4%, but almost every other channel went up. Facebook use increased by 5%; Twitter, LinkedIn and Google+ all rose by 10%; even a couple of more marketers started to use Quora on behalf of their brands. Meanwhile, Pinterest has yet to really take off (for pharma at least) and marketers seemed to have shied away from using Sermo to reach physicians—but overall it certainly seems as if social media is truly hot again.

A few respondents even went off the books to name some social sites we didn’t list including iVillage (a site that offers expert advice on subjects such as pregnancy, beauty, food, recipes, health, home and entertainment) and ReachMD (a multi-outlet healthcare programming source by medical professionals for medical professionals that includes its own radio station).

Furthermore, our respondents expect this boom in social media use to grow even more over the next year. Once again, over 80% predict that social media use by marketers will increase, while only 3% expect it to decline and 16% expect it to remain the same. Last year it seemed as if people were becoming disenchanted with social media—or just disinterested. That’s because they have been waiting years for the FDA to issue guidelines regarding social media marketing and had yet to receive them. But maybe the time has finally come and pharma is ready to embrace social media. Maybe the promise of guidelines from the FDA by July 2014 has given people a little incentive to dip their toes in the water. Or maybe the promise of guidelines by July 2014 made people realize that they can no longer just continue to wait for something that may never arrive. That it is time to just jump into the abyss. Of course, it is a little less dramatic than that as marketers can use the guidelines the FDA has established in other mediums as a rudder in the choppy waters of social media. But the point is that it seems pharma is finally done waiting and the industry is starting to pave its own path in social media.

Thanks to Our Respondents From These Companies

3M

Abbott Laboratories

Aesculap

Alcon Laboratories

AliMed, Inc.

Alkermes

Almirall

AMAG Pharmaceuticals

Amarin Pharma, Inc.

American Regent

Amgen

Amylin Pharmaceuticals

Apotex Corp.

Astellas Pharma US, Inc.

AstraZeneca

Bayer Healthcare

Biogen Idec

BioMarin

BioSyent Pharma, Inc.

BioTek

Biotest Pharmaceuticals

Blue Ocean Medical

Boehringer Ingelheim

Breckenridge Pharmaceutical, Inc.

Bristol-Myers Squibb

Capsugel

Centocor Ortho Biotech, Inc.

ConvaTec

Cornerstone Therapeutics

CryoLife

CSL Behring

Cubist Pharmaceuticals

Daiichi Sankyo

Dey Pharma

diaDexus, Inc.

Eli Lilly & Company

Eisai

EMD Serono, Inc.

Endo Pharmaceuticals

Ethicon

FemmePharma Global Healthcare, Inc.

Ferring Pharmaceuticals

Forest Laboratories

Galderma Laboratories

Galectin Therapeutics

Genentech

Genzyme

GlaxoSmithKline

Grifols, Inc.

Horizon Pharma

Hospira

Intas Pharmaeuticals

InterMune, Inc.

Janssen

Johnson & Johnson

Kimberly-Clark

Kowa Pharmaceuticals America

Mallinckrodt Pharmaceuticals

MedImmune

Medtronic

Merck & Co., Inc.

Millar Instruments, Inc.

Millennium Pharmaceuticals

Myriad

Novartis

OraPharma

Pfizer

Pharmics, Inc.

Prometheus Laboratories

Sagent Pharmaceuticals, Inc.

Sandoz, Inc.

Sanofi

Sanofi Pasteur

Shire Pharmaceuticals

Smiths Medical North America

STEMCELL Technologies

Stiefel Laboratories, Inc.

Takeda

Terumo Cardiovascular Systems

Teva Pharmaceuticals

Thermo Fisher Scientific

Topix Pharmaceuticals, Inc.

Tranzyme Pharma

UCB

Upsher Smith Laboratories, Inc.

Vermillion, Inc.

Watson Pharmaceuticals

Wockhardt USA