Patient out-of-pocket drug cost is a primary component of the medication adherence equation. Dr. William Shrank and colleagues from Harvard and CVS Caremark evaluated over 10 million prescriptions to assess prescription abandonment, concluding that “sticker shock” is real and many patients walk away from therapy when the cost is too high.1 With this as a baseline, it makes sense that reducing patient copays would boost therapy starts and adherence. And that commonsense expectation has been proven true: Multiple published studies demonstrate that copay assistance programs increase adherence.2-4 Furthermore, new information suggests that adherence rates are indeed rising.5 Yet poor adherence continues to confound brand managers throughout pharma. Why is that?

For one thing, while patient out-of-pocket (OOP) cost may be the biggest piece of the adherence puzzle, it’s still just one piece among several. For instance, in its report, Adherence to Long-Term Therapies: Evidence for Action, the World Health Organization identifies five interacting factors: Social/economic, therapy related, patient related, condition related, and health system and health team. So, in designing adherence efforts, brand leaders should consider a broad mix of strategies. Indeed, several non-financial tactics show real promise in boosting adherence: Medication synchronization programs, direct-to-patient messaging, and strong HCP-to-patient communication (including delivery of oral and printed patient education materials.)

Despite the success of alternative tactics, the search for the “dominant driver” of poor adherence often leads back to medication access generally, and patient OOP cost specifically. And the truth is, the perfect copay support program has yet to be created; providers are still innovating, measuring, and refining. Moreover, the playing field is in constant flux, complicating the work of serving stakeholders (including, most of all, patients). Let’s pull back the curtain on some of the expanding challenges in the world of copay and access.

Challenge #1

Overcoming today’s copay challenges is more difficult than ever.

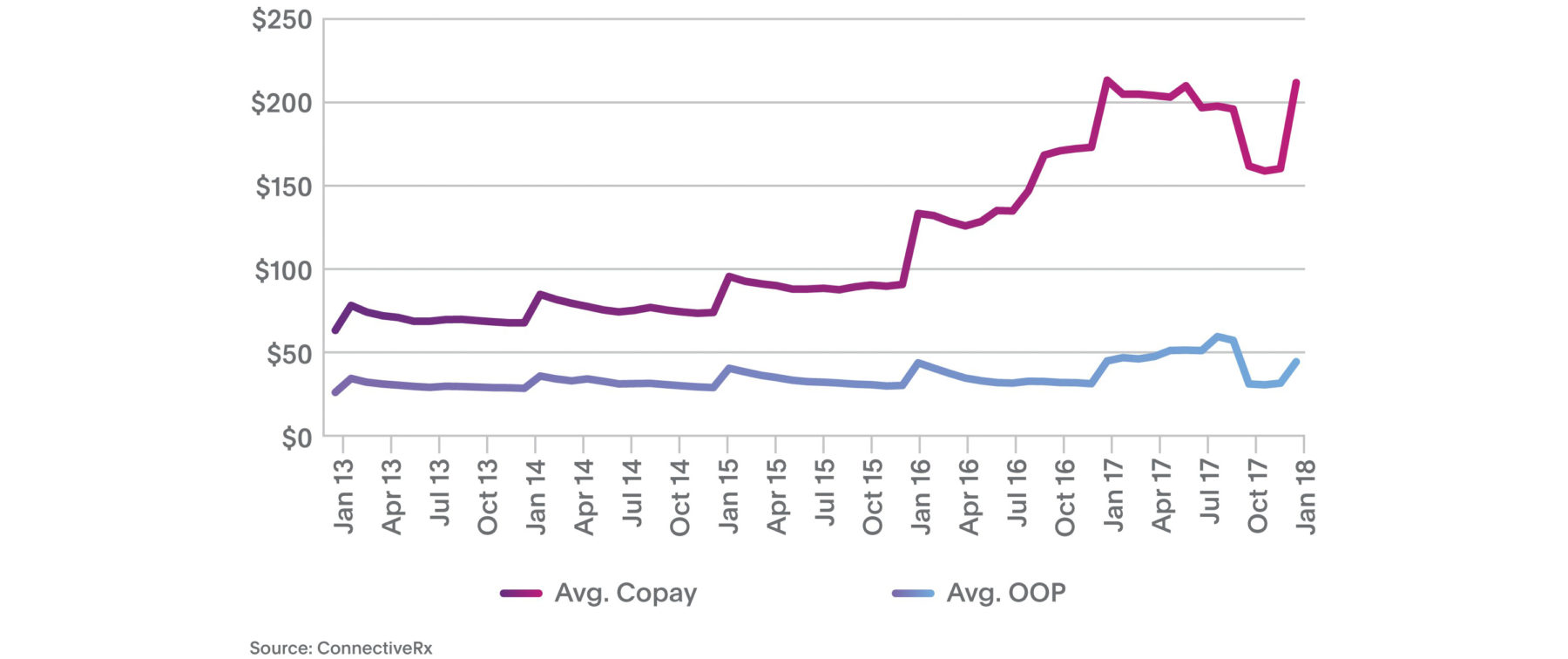

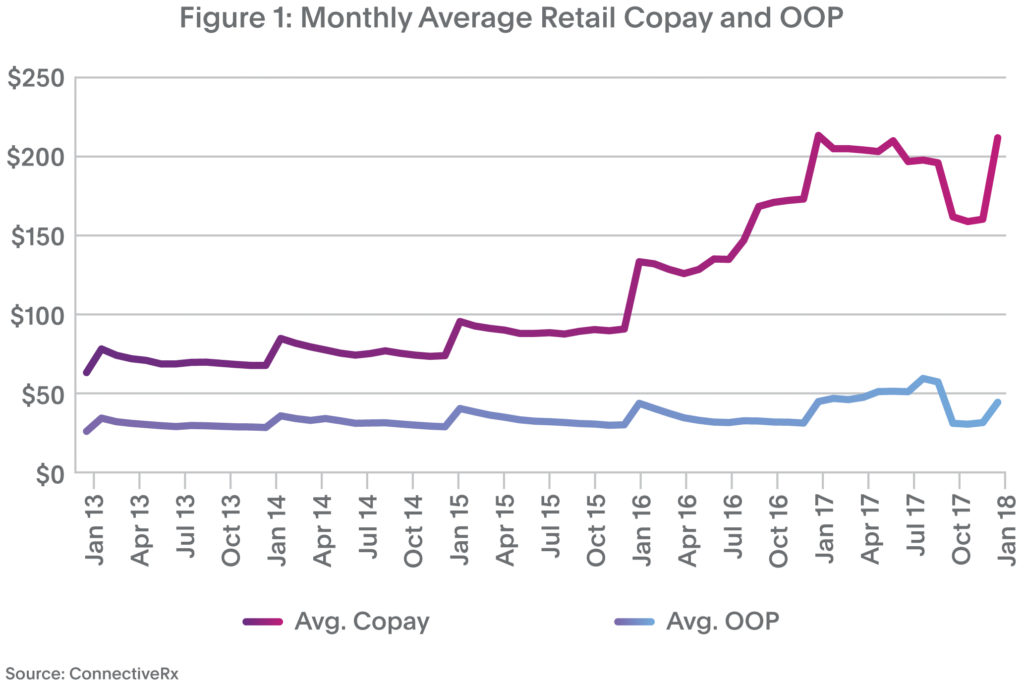

It seems that with every step we take to help patients maintain reasonably priced medication access, the hill gets a little steeper. Take average copays, for instance. As shown in Figure 1, average retail copays for patients using copay programs spiked to $212 in January 2018 versus $133 in January 2016. At least some of the “January deductible-reset spike” is due to expanding use of high-deductible plans.

Challenge #2

Challenge #2

Winning the broader access battle gets harder every year.

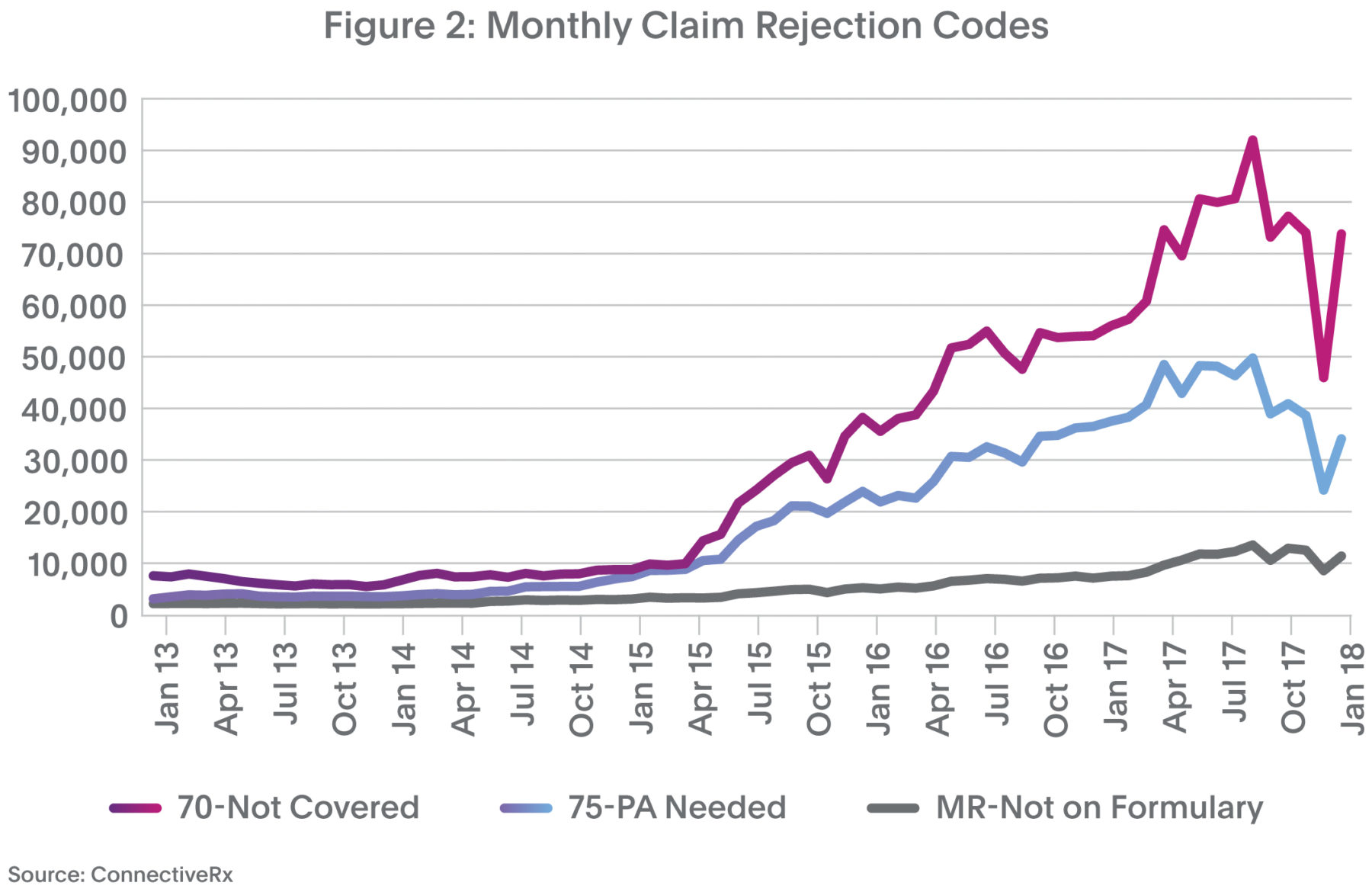

Today’s access challenges go beyond high copays. Throw in NDC blocks, step edits, prior authorizations (PA), accumulator adjustment programs, etc., and the magnitude of drug access hurdles becomes clearer. This pain has grown dramatically. In Figure 2, notice the multifold rise in claims rejected because a product is not covered (code 70) or a PA is required (code 75).

These obstacles foster higher prescription abandonment and lower adherence.

These obstacles foster higher prescription abandonment and lower adherence.

Challenge #3

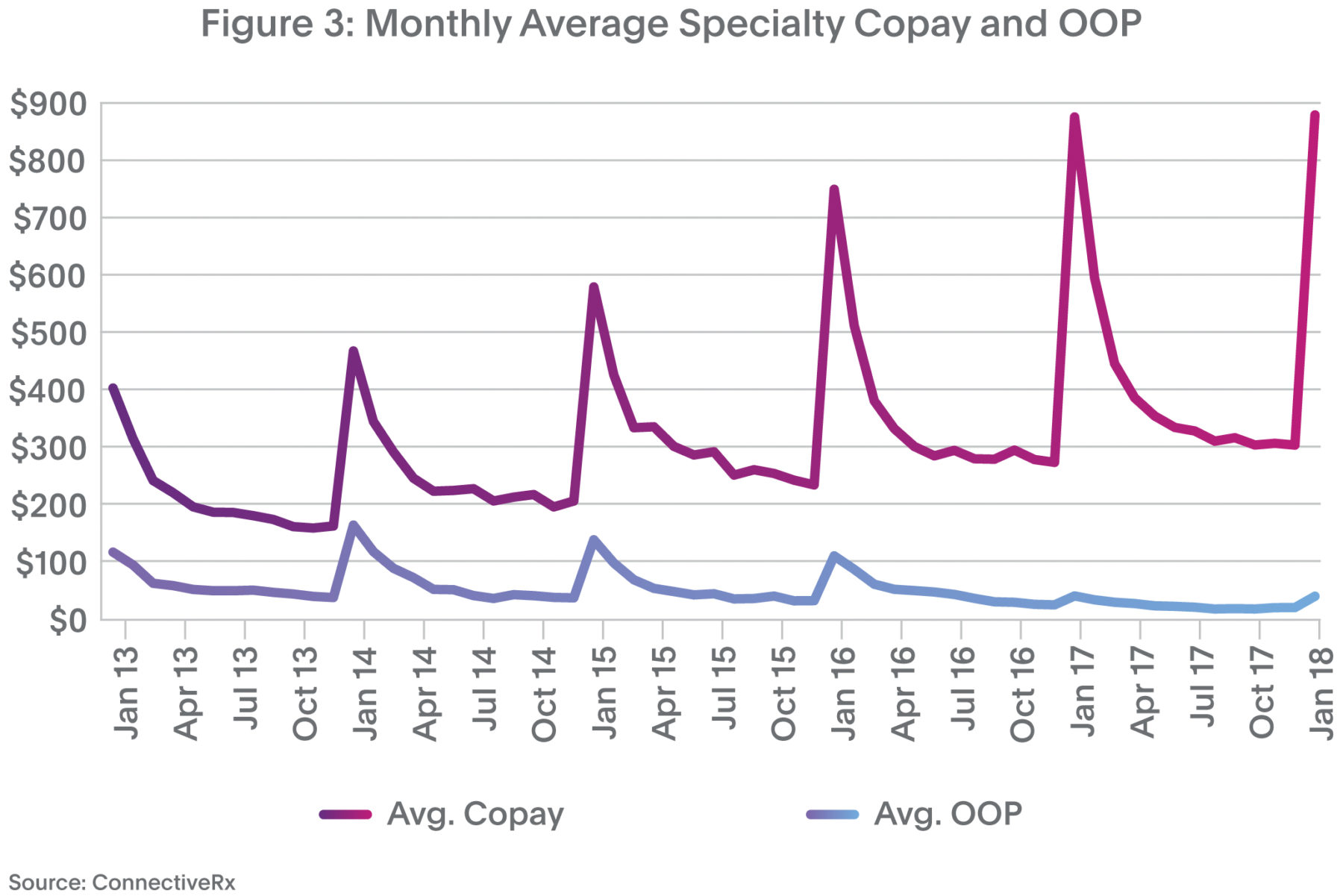

Providing optimal support for specialty brands is increasingly complicated.

As specialty products expand their share of the branded pharmaceuticals market, payers increasingly target them. As a result, the challenge of gaining and maintaining access to these medicines gets more difficult by the month. To start with, the spike in January copay is even more pronounced in the specialty market than in retail (Figure 3).

Furthermore, manufacturers and their hubs are scrambling to support HCPs and patients as they navigate a multitude of access hurdles such as high deductibles and coinsurance, only to encounter additional blocking tactics as described in Challenge #2.

Furthermore, manufacturers and their hubs are scrambling to support HCPs and patients as they navigate a multitude of access hurdles such as high deductibles and coinsurance, only to encounter additional blocking tactics as described in Challenge #2.

How are copay providers adjusting to meet these challenges?

Copay providers are working overtime to clear the path to better adherence. Here are three of the latest developments:

- Novel copay delivery channels. It’s not just cards, websites, and email anymore. We’re seeing continued growth in delivering copay offers via SMS/MMS (text) and in prescribers’ EHRs. Both of these are in-workflow channels that deliver offers where and when they’re needed.

- Enhanced service combinations. New analytics and technology are enabling copay providers to partner with other suppliers to deliver integrated service combinations. For instance, advanced adjudication methodologies now enable copay processing to be integrated with an eye toward other access hurdles (e.g., PAs or NDC blocks) so that patients receive seamless support.

- Expanded reimbursement options. In new reimbursement models, patients and prescribers can receive payment via Automated Clearing House (ACH) transactions. Advanced payment processing streamlines the management of supporting documentation, incorporates multiple levels of automatic and manual edit checkpoints, and includes data integration with an array of third-party vendors.

In the end, the battle for full adherence promises to be ever present. But working together, we will continue to strive to see that every patient has ready access to the medicines they need.

References:

- Shrank W, et al. “The Epidemiology of Prescriptions Abandoned at the Pharmacy.” Annals of Internal Medicine. 2010;153(10):633-640.

- Daugherty J, Maciejewski M, and Farley J. “The Impact of Manufacturer Coupon Use in the Statin Market.” Journal of Managed Care Pharmacy. 2013;19(9):765-772.

- Starner C, et al. “Specialty Drug Coupons Lower Out-Of-Pocket Costs And May Improve Adherence At The Risk Of Increasing Premiums.” Health Affairs. 2014;33(10):1761-1769.

- Daubresse M, et al. “Effect of Prescription Drug Coupons on Statin Utilization and Expenditures: A Retrospective Cohort Study.” Pharmacotherapy. 2017;37(1):12-24.

- Turcu-Stiolica A, et al. (2018). “Analysis of Financial Losses due to Poor Adherence of Patients with Chronic Diseases and Their Impact on Health Economics, Financial Management from an Emerging Market Perspective, Ph.D. Soner Gokten (Ed.).” InTech, DOI: 10.5772/intechopen.70320.