As specialty pharmaceutical products are becoming increasingly complex due to more technology-driven drug development, the path to payer coverage is complicated by the need to understand emerging therapeutics, unique delivery systems, and personalized patient support programs. For pharma marketers to achieve success across markets, they must adapt strategies to various payer channels. But any roadmap to better coverage is not complete without ways to improve access. So, marketers must also learn to navigate administrative systems and develop practical solutions to assist providers and patients alike whether they are launching a new-to-market specialty product, a new indication, or defending their position in a competitive therapeutic area.

A Shifting Landscape

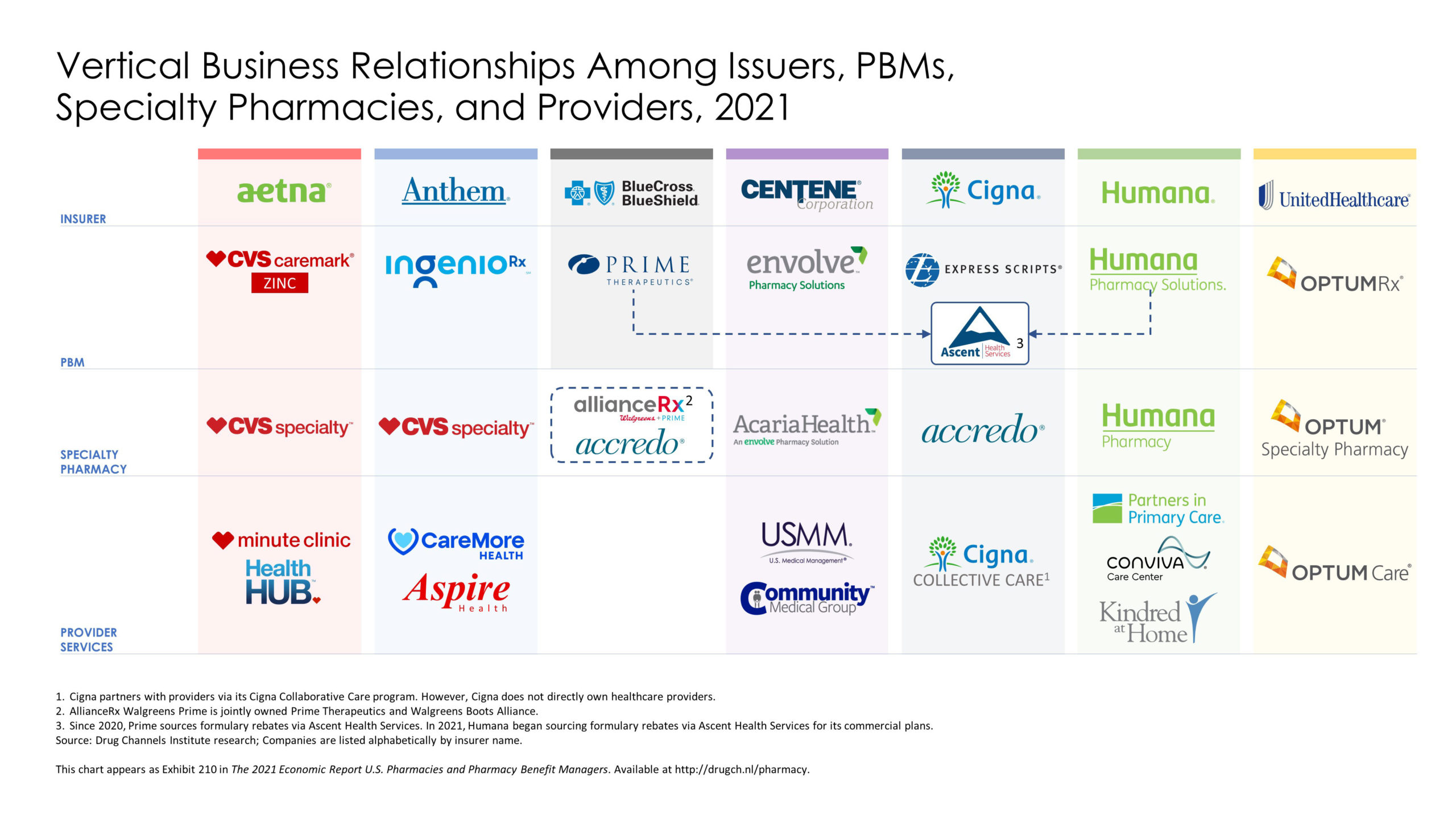

Payer vertical integration, including acquisition of specialty pharmacies, has changed the landscape and underscores business implications of integrated decision-making.1

Insurers have gained control of downstream pharmacy and provider organizations, making it easier to implement integrated management approaches such as site of care and formulary management strategies (see Figure 1).2

Coverage by Market Segment

Coverage by Market Segment

Commercial health plans and pharmacy benefit managers (PBMs) continue to manage specialty products through plan-sponsored tiered formularies, with patient cost-sharing differentials steering access to preferred products. Specialty cost sharing is often a percentage of the drug cost (i.e., 30% for the preferred specialty tier) with a higher percentage (i.e., 50%) collected for non-preferred products. Commonly seen in specialty pharmacy, high out-of-pocket (OOP) costs present a significant barrier to access for many patients.

As mentioned in a recent RxBenefits blog, employers are looking for other ways to address the growing impact of specialty medications on employer healthcare costs, including carve-out strategies from the pharmacy benefit.3 This approach can add administrative complexity and result in gaps in coverage if benefits are not managed properly. Health plans and PBMs instead are leveraging their vertical business relationships to develop integrated programs that address the needs of the “whole patient” and bringing these solutions to self-insured employer group customers. Marketers should look beyond the product specialty at hand and consider engagement opportunities with primary care and behavioral health providers where appropriate.

Increasingly, exclusionary formularies are expanding across market segments in therapeutic classes where sufficient competition exists to drive preferred contract pricing. Medicaid formularies are generally exclusionary since differential cost sharing is limited; and Medicare formularies likewise tend to be exclusionary, with a percentage cost share applied for covered specialty products. The unique structure of Medicare Part D impacts patient cost sharing over the course of the benefit year and is an important consideration for developing strategies to ensure patients have uninterrupted access to specialty drug treatment.

Each formulary type (commercial, Medicaid, and Medicare) offers an appeals process allowing for exceptions based on medical necessity or prior failure of a covered drug. Helping prescribers and larger health system administrators navigate these various coverage and benefit policies is an important aspect of managed markets access strategy.

Key Considerations for Improving Specialty Drug Coverage

If you are in need of strategies to help ensure more optimal coverage of your specialty product, then keep these six aspects in mind:

- Regulatory Knowledge: Marketers must have a working knowledge of or retain experts on regulatory policy to leverage opportunities for engagement with their payer, HCP, and specialty pharmacy customers (i.e., Part B policy, Part D coverage gap, and policies concerning rebates).

- Innovative Insurance Coverage Platforms: Innovative health insurance providers (i.e., Sidecar Health, Oscar Health, and others) offer less restrictive formularies and instead focus on managing coverage and benefits with financial tools such as reference pricing and coinsurance tied to drug cost, net of rebates, and discounts. Market access professionals should stay up to date on innovative insurance coverage platforms and watch for some components to become mainstream.

- Specialty Drug Management Companies: Differences in medical versus pharmacy benefit for specialty drug coverage highlight the need to engage with intermediaries that specialize in managing specialty drugs under the medical benefit. These include market leaders Express Scripts/Accredo/eviCore, CVS Health Specialty, OptumRx/Optum specialty management, Magellan Rx/Magellan specialty management, and Prime Therapeutics, as well as lesser-known entities such as Archimedes, Envolve Specialty Management, and HealthSmart Rx Solutions. Program components include robust clinical management solutions, billing error management, site of care and channel optimization, a health economics coverage platform, and a comprehensive program for supply chain optimization.4Pharmaceutical manufacturers should engage with these management companies and their networks of specialty pharmacies leveraging aligned areas of focus that are of interest to their common payer customers.

- Personalized Coverage: Individualized treatment and coverage approaches offer new mechanisms for securing access on a patient-specific basis. The need for personalized treatment provides access versus an “all or nothing” coverage decision (i.e., genetic markers as predictors of success in oncology/rare disease; and the role of specialty pharmacies in interpreting/validating test results prior to dispensing).

- Differentiated Clinical Characteristics: Clinical differentiators for products in crowded categories offer a means of gaining streamlined access through coverage determination policies and procedures. Aligning differentiated clinical characteristics with generally accepted treatment guidelines strengthens positioning and provides support for gaining access through formulary exception processing.

- Pre-approval Surveillance: Since FDA approval no longer guarantees access, even for approved indications, pre-approval surveillance is critical to anticipating payer management approaches and building programs to mitigate obstacles to a successful launch plan.

Promote Transparency in Pricing and Access

Besides securing better coverage from payers, it is also important to help providers navigate administrative systems to actually facilitate coverage of the product as well as help patients to quickly access it. To do so, focus on these four areas:

- Program and Systems Support: Patients prescribed specialty medications generally need to start treatment promptly to achieve desired health outcomes. Specialty patient enrollment programs, coupled with ePrescribing and electronic prior authorization (ePA), improve speed to therapy by automating the enrollment process and reducing overall administrative burden for providers.5 Programmatic support to encourage connectivity between the prescriber’s EHR system, specialty pharmacies, and hubs would help streamline access.

- Competing for Coverage Versus Biosimilars: The U.S. biosimilar market landscape and development pipeline present challenges and/or opportunities for pharma marketers, depending on each manufacturer’s business development strategies. Biosimilar competition is a consideration when providing product support in any of the following therapeutic areas: oncology, supportive care, insulin (rapid-acting and long-acting), ophthalmology (innovators Lucentis and Eylea), TNF blockers, immunosuppressants, bone health (Prolia and Xgeva), infertility, and growth hormone. Whether launching into the biosimilar space or defending an innovator position, pharma manufacturers should engage in the development of value frameworks to gain early insights and prepare for market positioning.

- Limited Distribution Specialty Pharmacy Relationships: Explore the role specialty pharmacies play in managing access. According to the CSI 2019 survey of manufacturers, almost 85% of manufacturers manage some or all their products through a limited-distribution model. While more significant levels of limited-distribution drugs (LDD) are found in specialty areas such as oncology and neurology, LDD activity is increasing across the board, including in respiratory, gastroenterology, and ophthalmology.6 With limited distribution and exclusive access to specialty drugs becoming more common, pharmaceutical marketers must have a clear line of sight and understanding of the supply chain, ensuring that patients with rare and complex conditions have unencumbered access.

- Innovative Programs to Mitigate the Impact of Patient OOP Expenses: Make it easy for specialty pharmacy financial managers to access funding for individual patients. Payers, providers, patients, and their advocates are looking to optimize manufacturer copay assistance programs to improve customer choice and adherence to prescribed therapy. One national health plan-owned specialty pharmacy reported that about 50% of their patients receive some type of financial support from drug manufacturers and charitable foundations.7 Specialty pharmacies and specialty benefit management companies employ dedicated copay assistance teams to help customers secure the assistance they need by navigating manufacturer-sponsored programs. Streamlining this process is one way pharmaceutical manufacturers can eliminate economic/cost-sharing barriers to access their products.8

Conclusion

Understanding payer and specialty pharmacy business relationships as well as financial drivers and how they influence decision-making is fundamental to negotiating access. Successful approaches align market access strategy with the unique needs of each market segment (i.e., commercial and government programs), while adapting to the regulatory environment. Personalized treatment approaches can be leveraged to drive medical and coverage policies that support differentiated access and full coverage for appropriate patients. Measurable improvements in access can be achieved by identifying practical solutions for navigating administrative procedures in place to enforce coverage policies.

Looking ahead to 2025, manufacturers who were surveyed about the future of specialty pharmacy drug distribution and access reported “plans to enrich the patient journey by improving interventions, expanding adherence integration, allowing open access, and enhancing integration between e-technology, HUBs, and specialty partners. Moreover, 80% of manufacturers are actively looking at ways to create value-based reimbursement programs for their products.”6

Finally, marketers should develop customer-centric strategic approaches and innovative solutions that are aligned to the overall business objectives and adaptable to different therapeutic areas and market dynamics. In this complex marketplace, operating within a framework that allows flexibility to meet changing business needs clearly makes sense.

References:

1. Fein AJ. “Drug Channels News Roundup, March 2021: Sanofi’s Gross-to-Net Bubble, Express Scripts Rebates, Health Insurance Hustle, and Vertical Integration Illustrated.” Drug Channels. Accessed February 23, 2022. https://www.drugchannels.net/2021/03/drug-channels-news-roundup-march-2021.html.

2. Fein AJ. “Insurers + PBMs + Specialty Pharmacies + Providers: Will Vertical Consolidation Disrupt Drug Channels in 2020?” Drug Channels. Accessed February 23, 2022. https://bit.ly/35VZmPY.

3. Campbell M. “How the Shift to Specialty Medications Changed Pharmacy Benefi”s.” RxBenefits. Accessed February 23, 2022. https://www.rxbenefits.com/blogs/how-a-historic-shift-in-the-clinical-landscape-changed-pharmacy-benefits.

4. “Archimedes Announces Launch of MEDiQ, A Next Generation Solution for Managing Specialty Drugs Under the Medical Benefit.” News release. Archimedes; August 10, 2021. Accessed February 23, 2022. https://bit.ly/3t3b18n.

5. “Specialty Patient Enrollment.” Surescripts. Accessed February 23, 2022. https://go.surescripts.com/2021-specialty-patient-enrollment-lp-0.

6. “CSI Specialty Group.” 2019 State of Specialty Pharmacy Report®. October 1, 2019. Accessed February 23, 2022. https://academynet.com/sites/default/files/csi2019spreport.pdf.

7. “Humana Specialty Pharmacy.” Accessed February 23, 2022. https://www.humana.com/provider/pharmacy-resources/tools/specialty-pharmacy.

8. “Specialty Pharmacy Management Across Benefits.” Cigna. Accessed February 23, 2022. https://www.cigna.com/employers-brokers/pharmacy/specialty.