Today’s Product Manager 2015

The product manager of today is on the move. As our 7th annual Product Manager Survey reveals, 25% of respondents have been with their current company for less than two years—a 12% increase over last year. And as our respondents last year noted, mergers and acquisitions were sure to shake up the landscape in 2015, and this could very well be a reverberation of that. It is likely quite a few of our respondents have changed companies as a result of one of the many recent deals or perhaps they just choose to jump ship to a company they felt was more stable. After all, today’s product manager does need to be quick on his/her feet.

Despite the fact that overall marketing budgets are up from last year, only 39% of respondents feel their budget is adequate—nearly half were satisfied with their budget last year. Today’s marketer must be even more nimble, flexible, cunning and innovative to deal with the lack of resources—and they already had to be all of those things even when they did have an adequate budget to work with. But the landscape is also changing. Our respondents feel more pressure from biosimilars, generics, payers and the public regarding drug prices. And they expect all of those factors to continue to play a role in 2016.

But one thing marketers seemed to finally gain a grasp on is social media. With the draft guidance released last year regarding social media platforms with character space limitations, Twitter use is way up for brands. So is Pinterest. Product managers have finally realized they have everything the FDA is going to give them and they have embraced social.

Considering just how busy today’s product manager is, we would like to thank everyone who completed our online survey, which was conducted over a 12-week period between June and September 2015 by Litchfield Research. We received more responses from within the medical device industry than ever before (see a full list of respondents’ companies in the tab below) as well as more participation from C-suite level executives. We are also happy to announce that Ryan D. Mancini, Product Manager, Aesculap, Inc., won the random drawing of survey participants and is the lucky owner of a new Apple Watch. Thank you, Ryan, and everyone else who helped provide a comprehensive examination of those working in the healthcare industry today and the challenges they face.

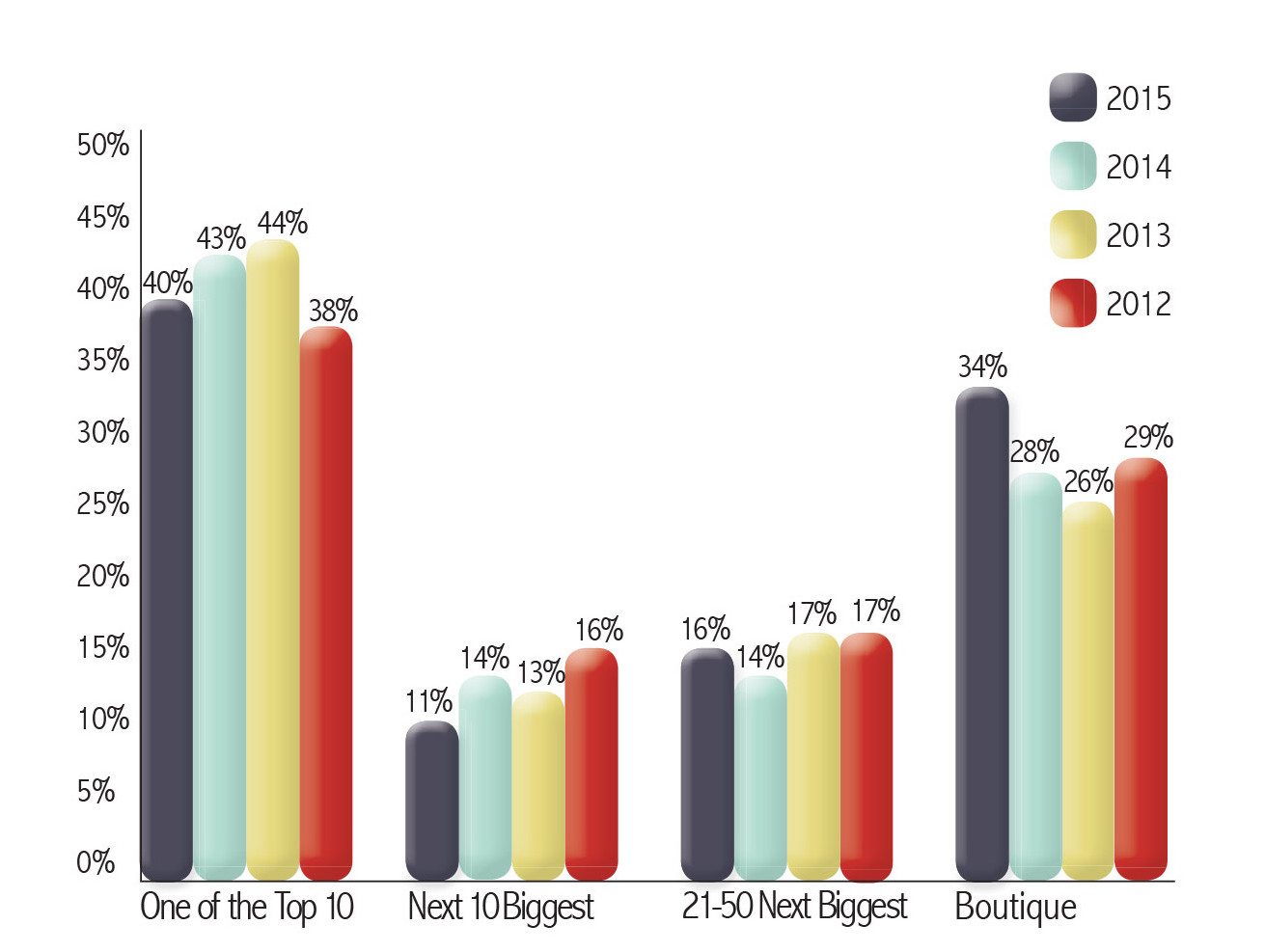

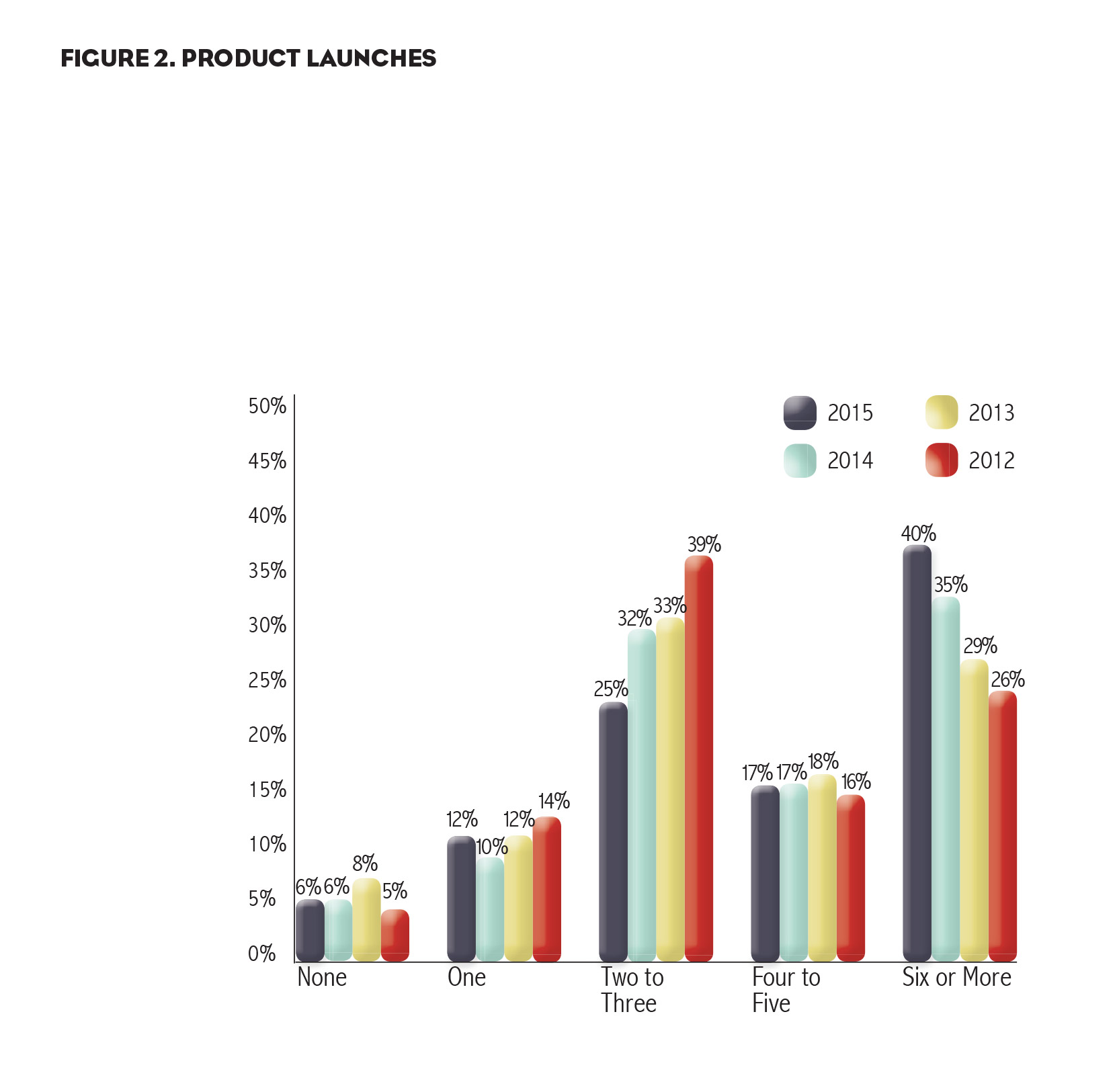

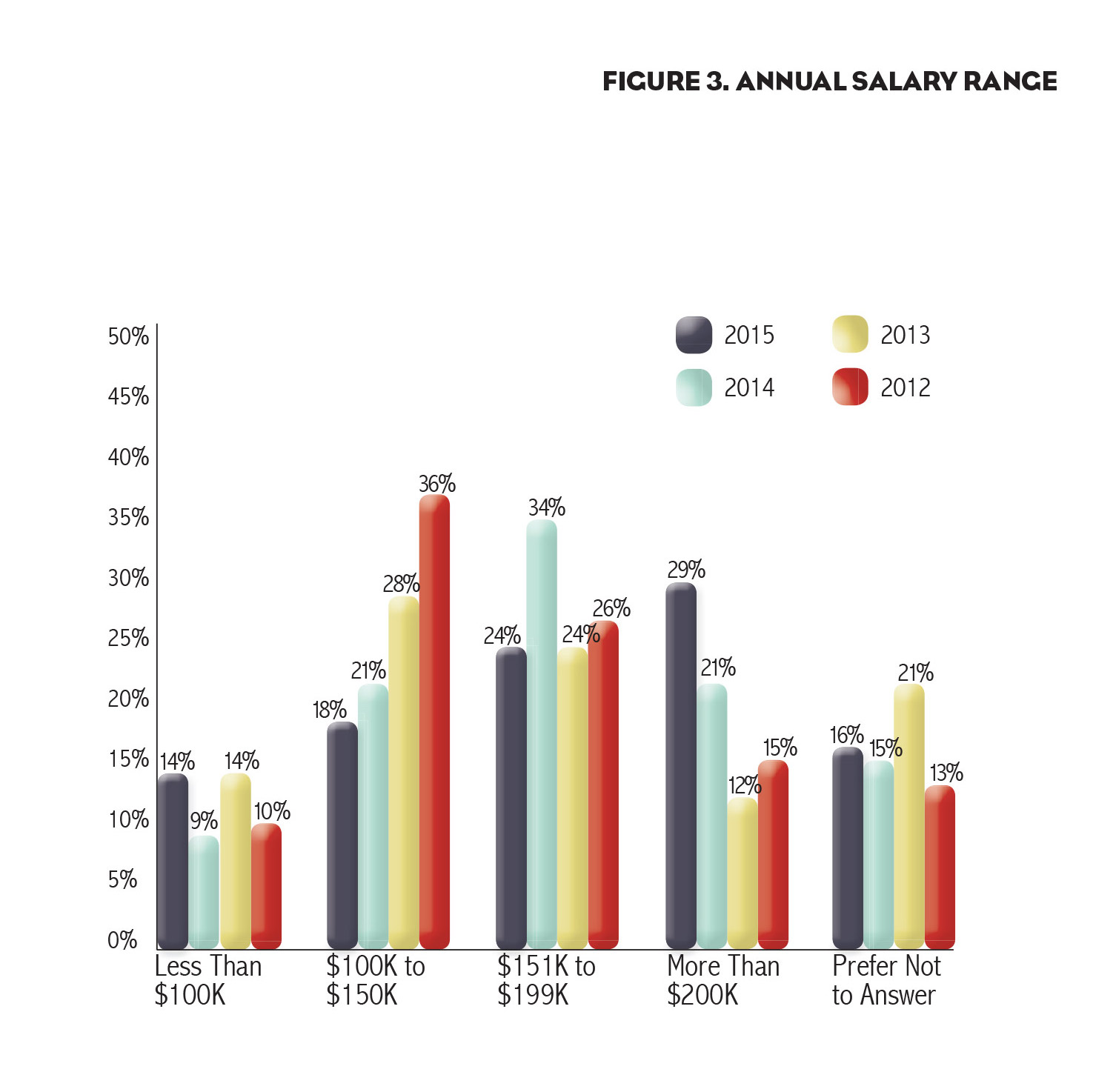

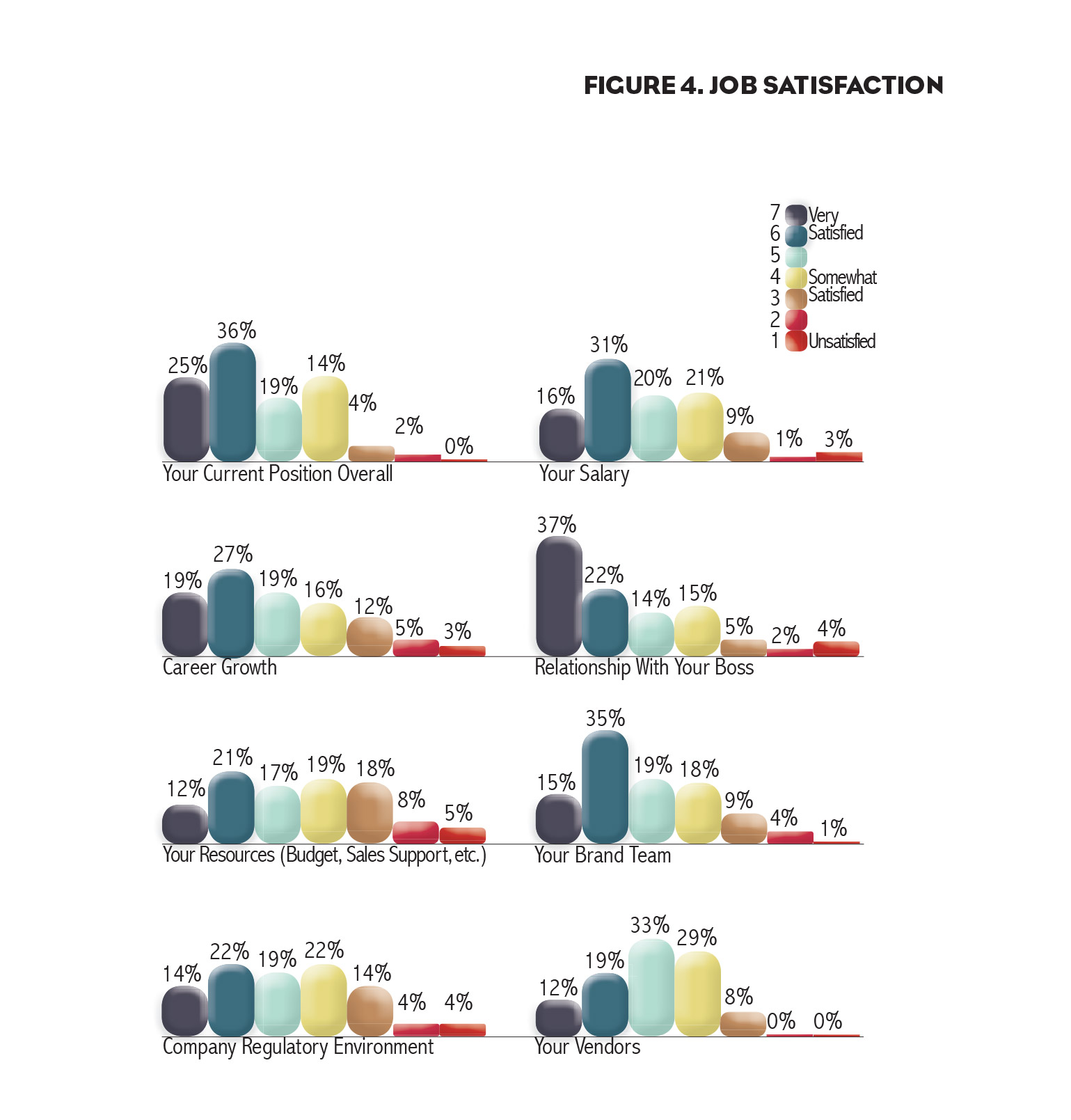

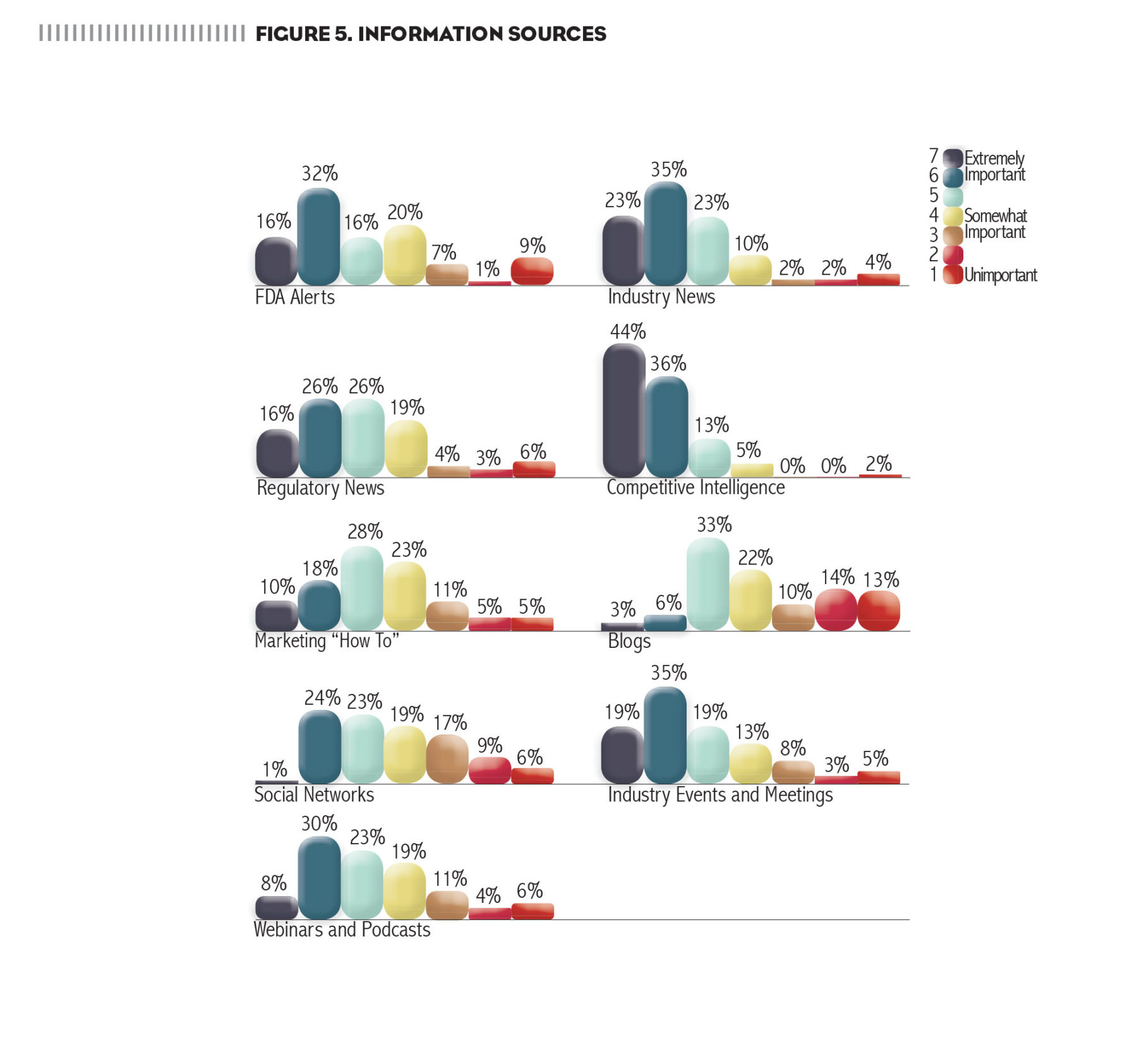

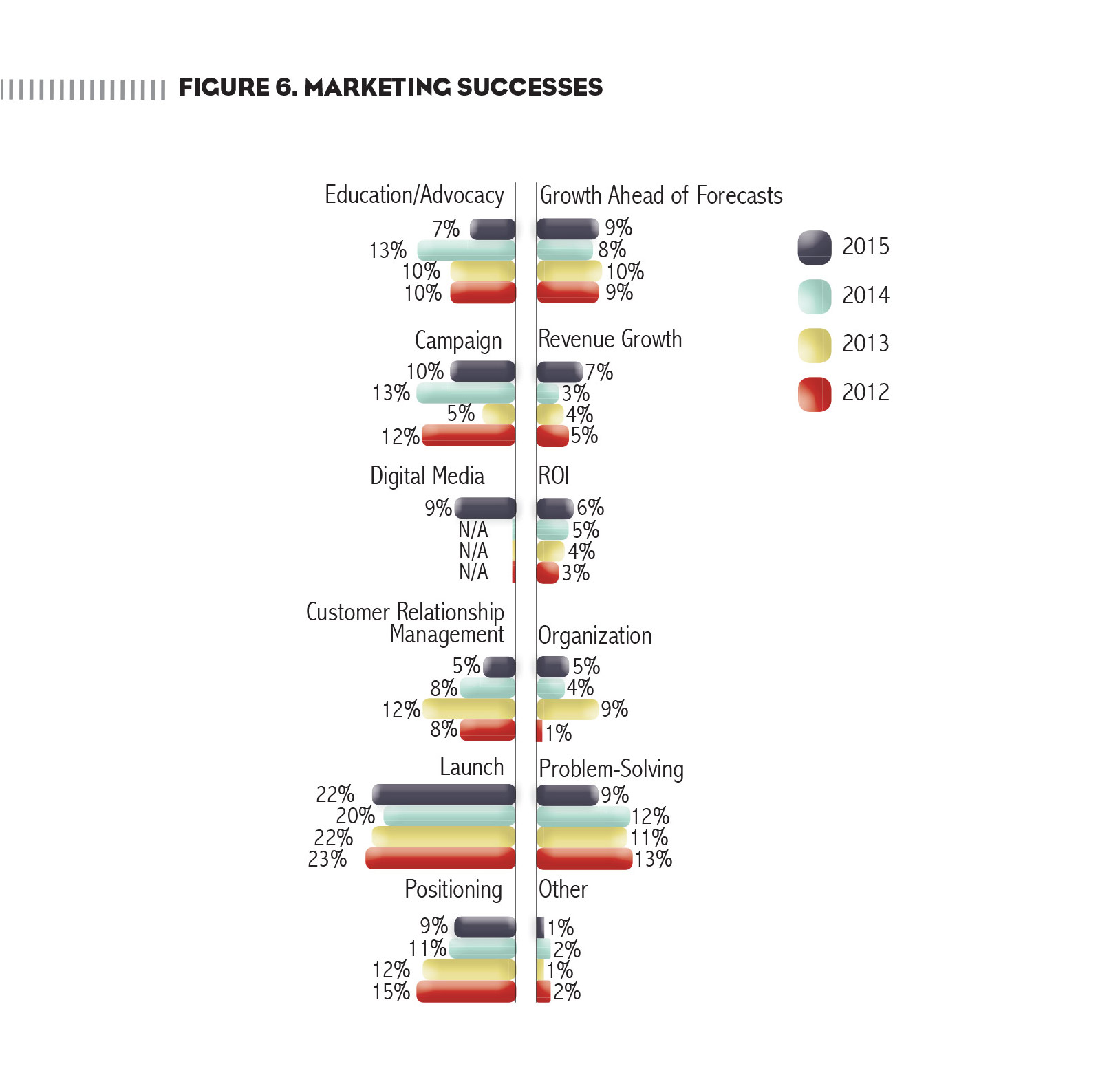

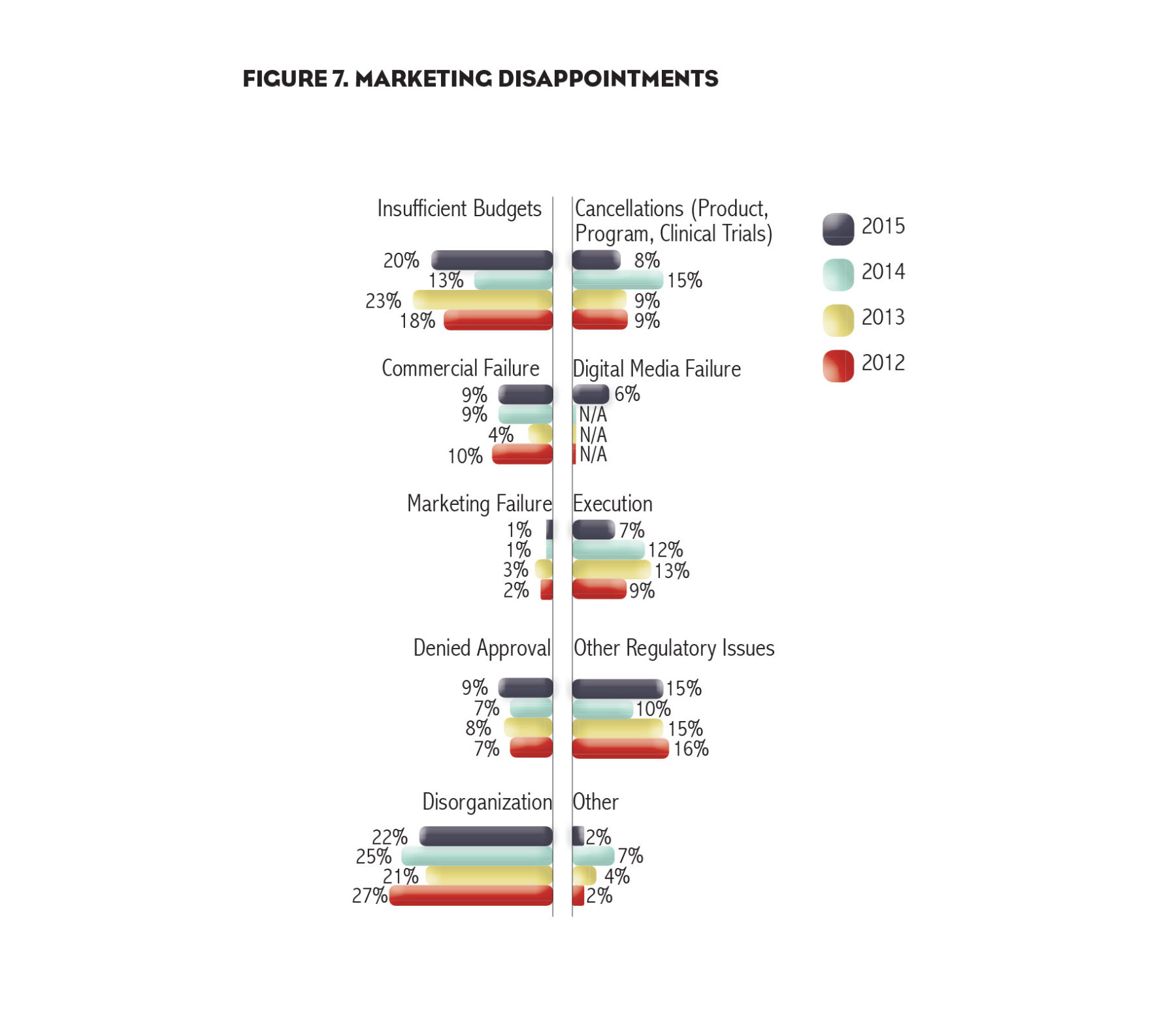

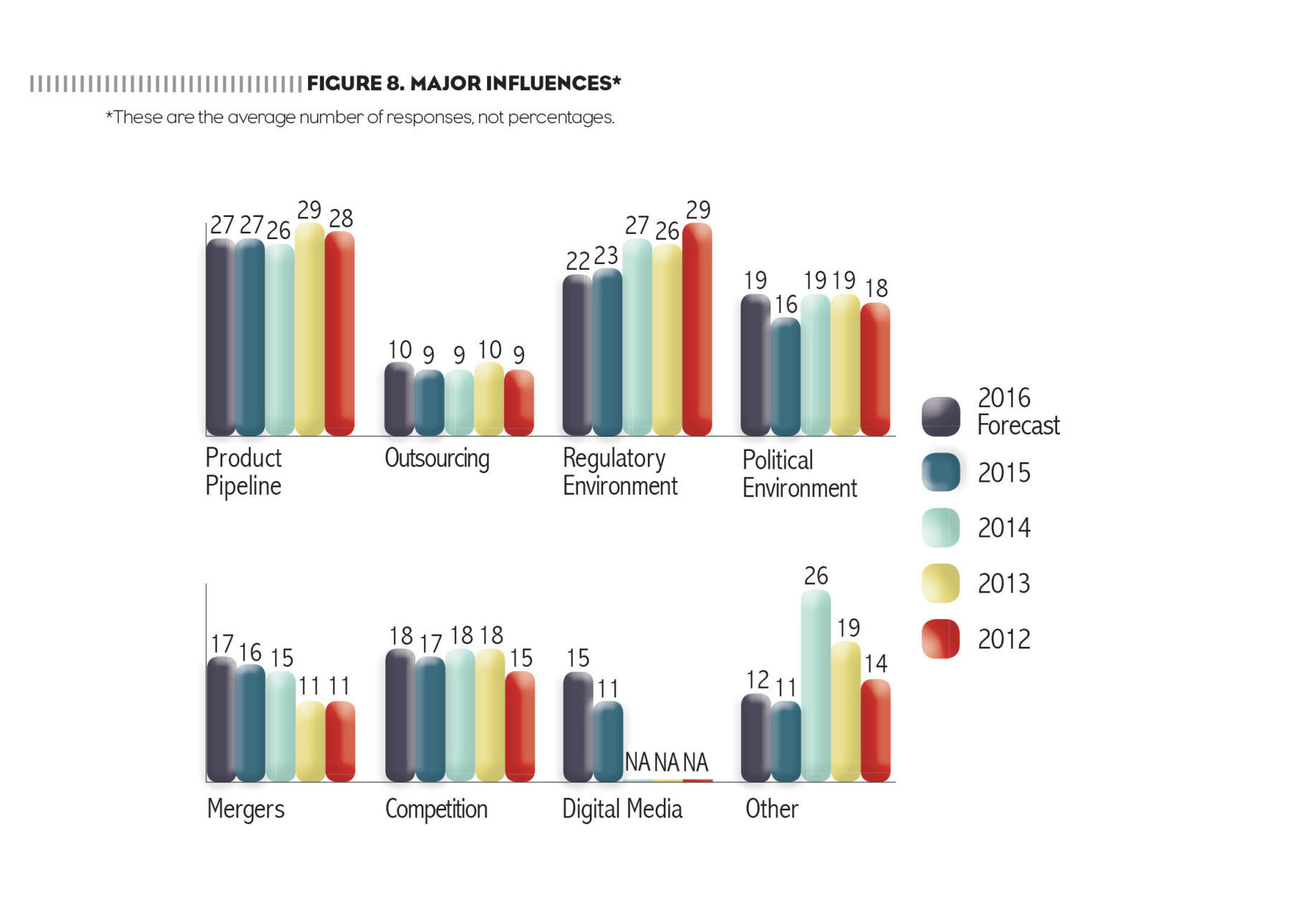

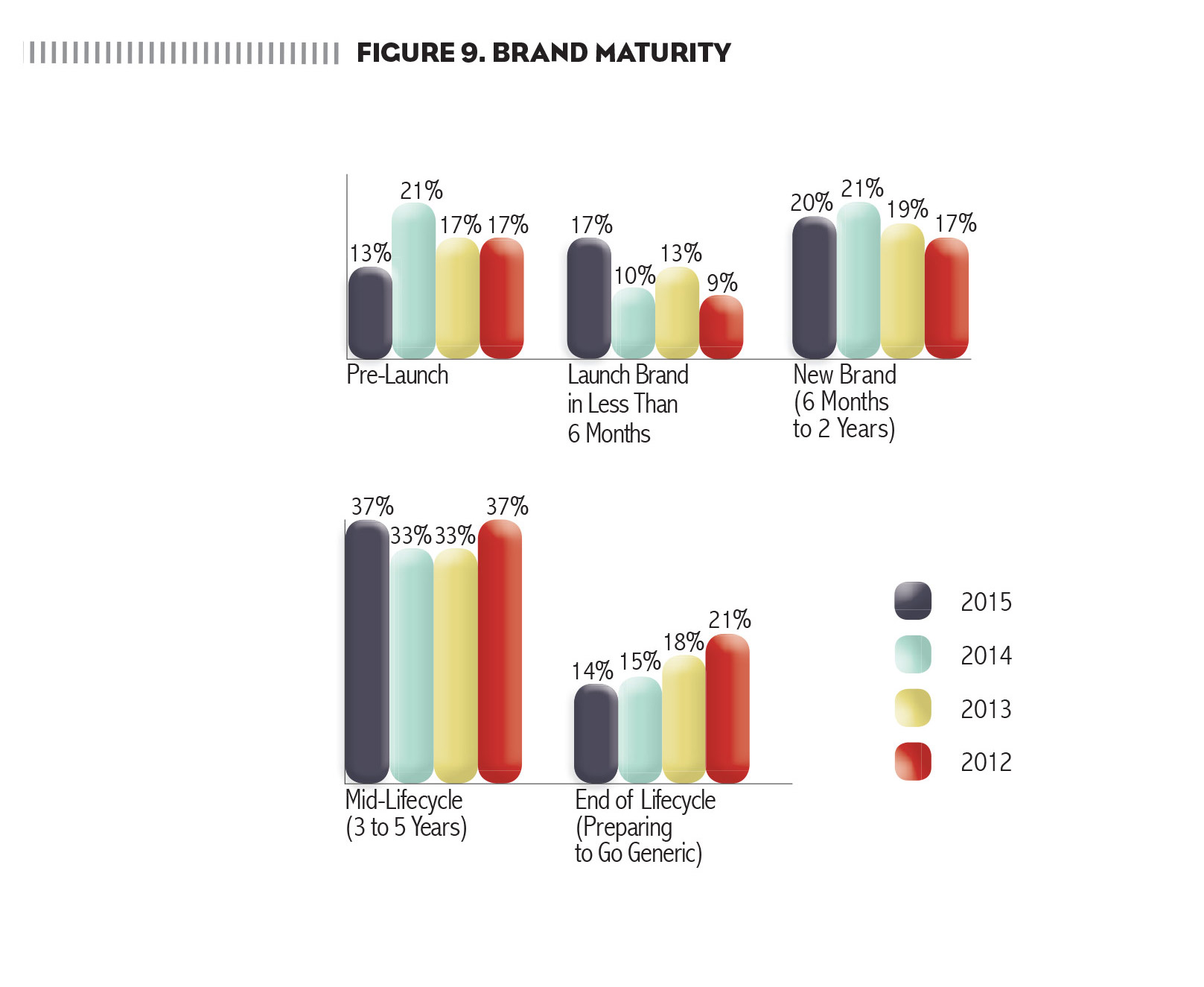

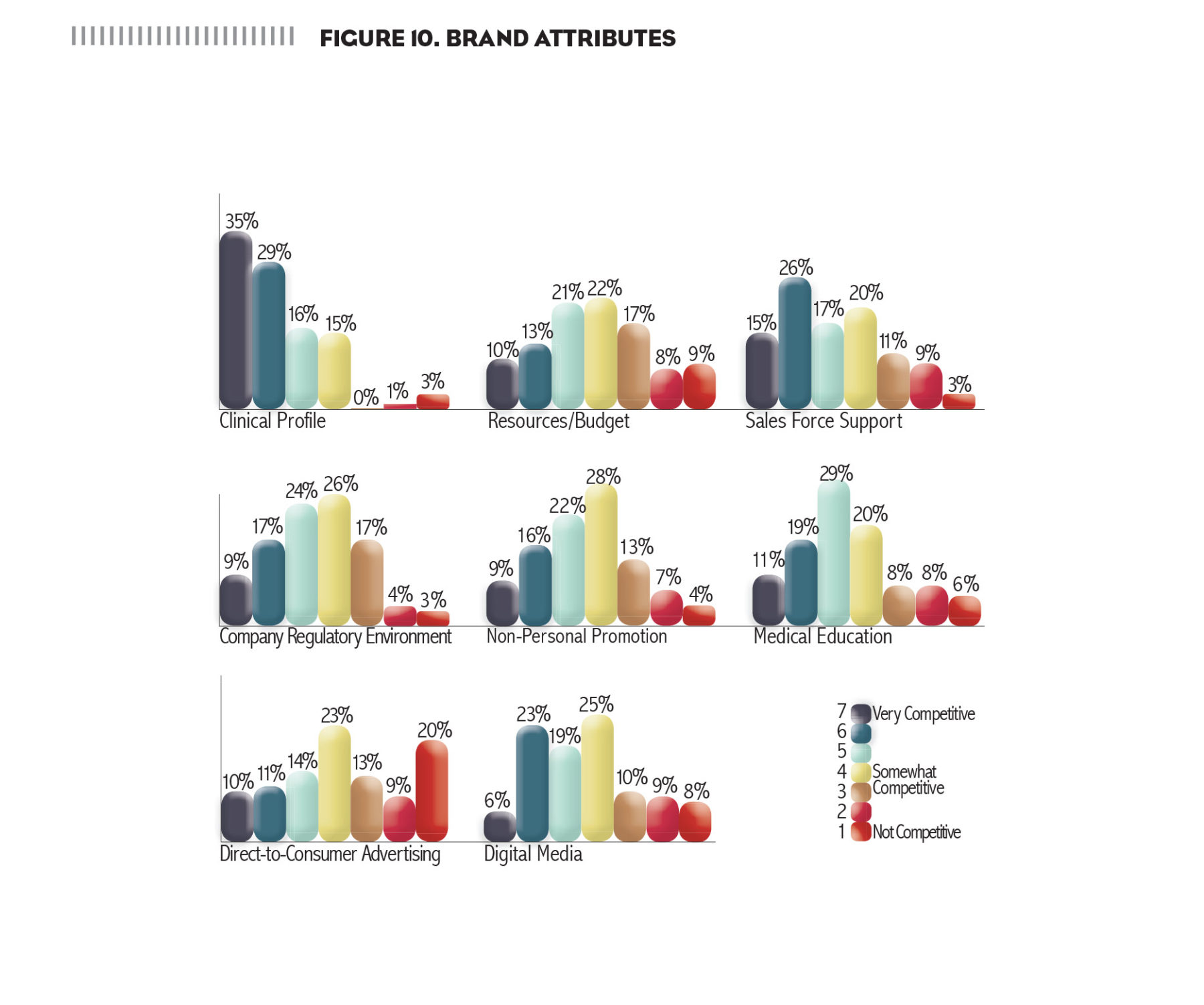

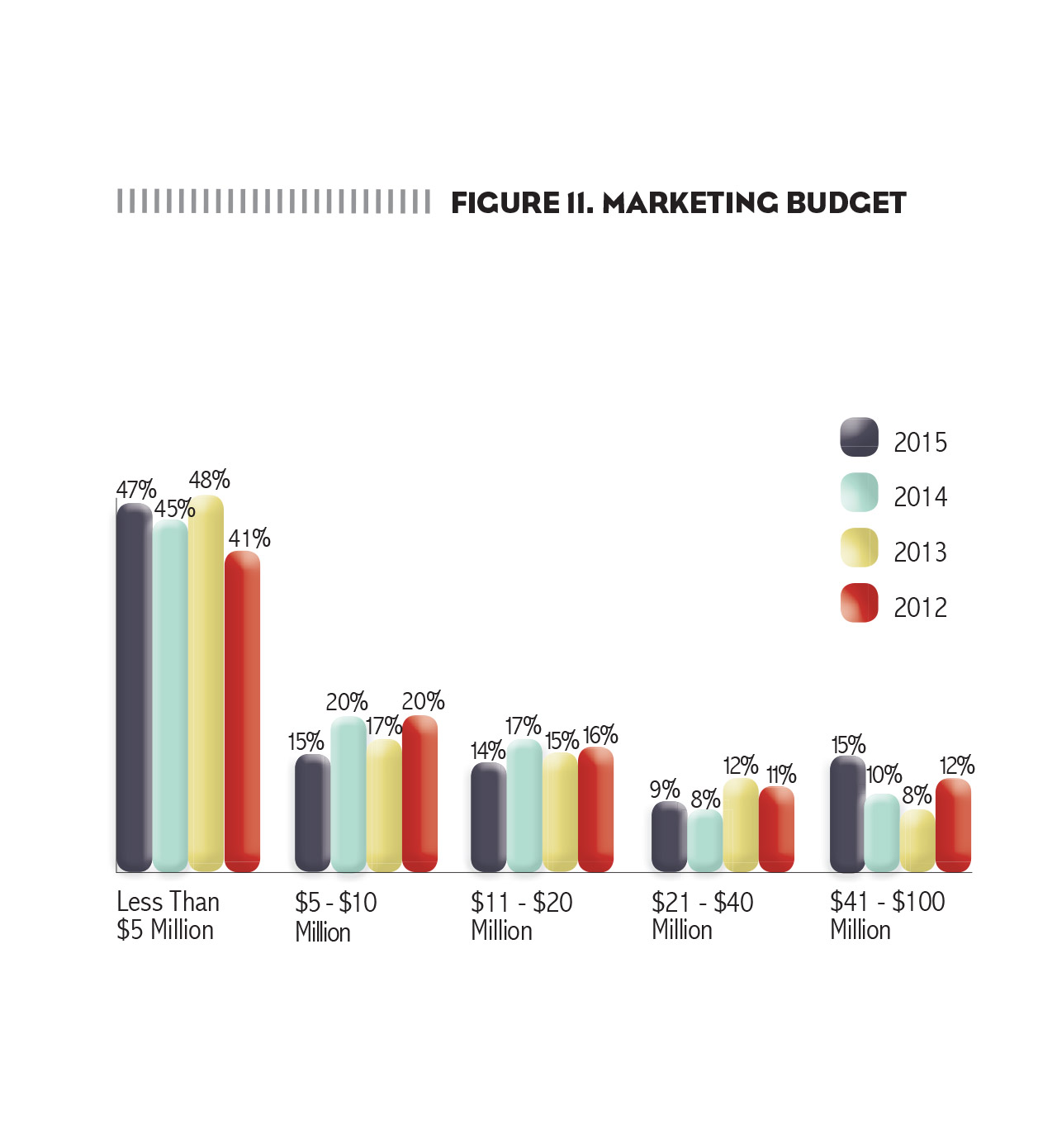

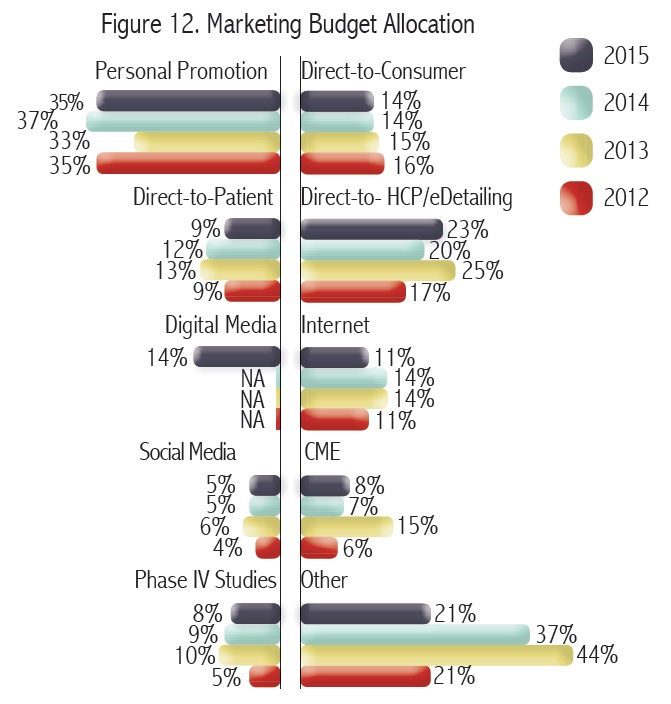

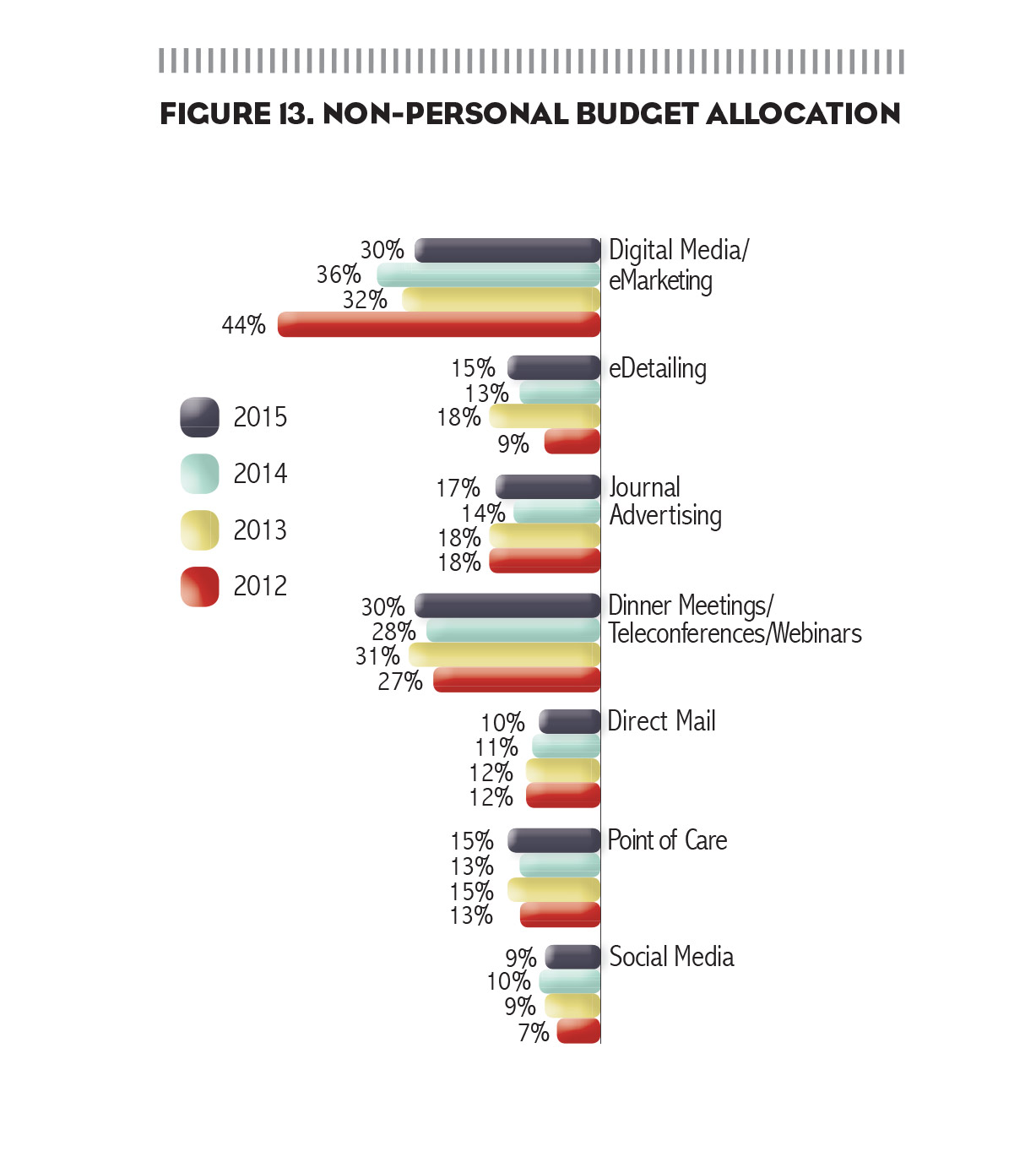

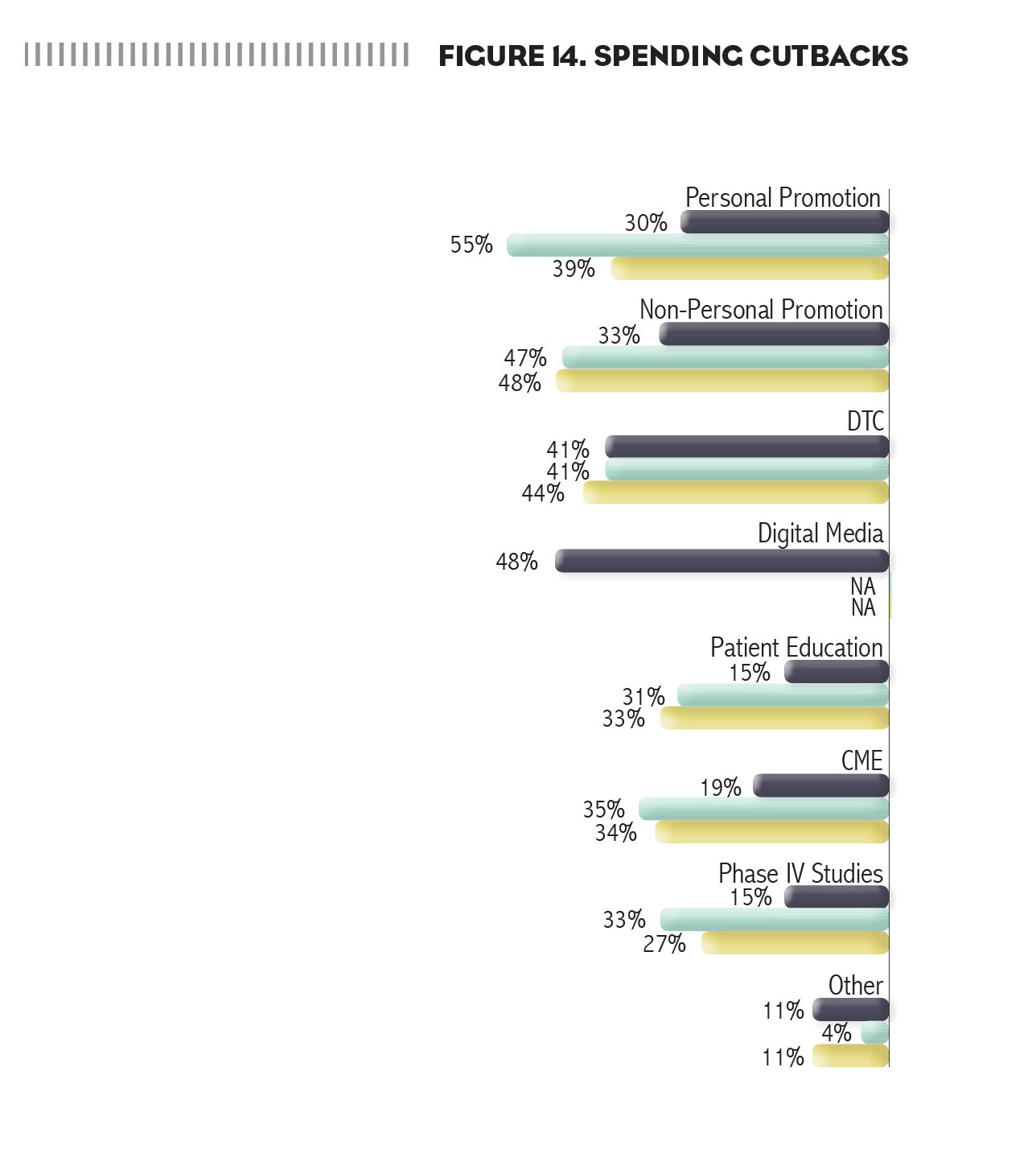

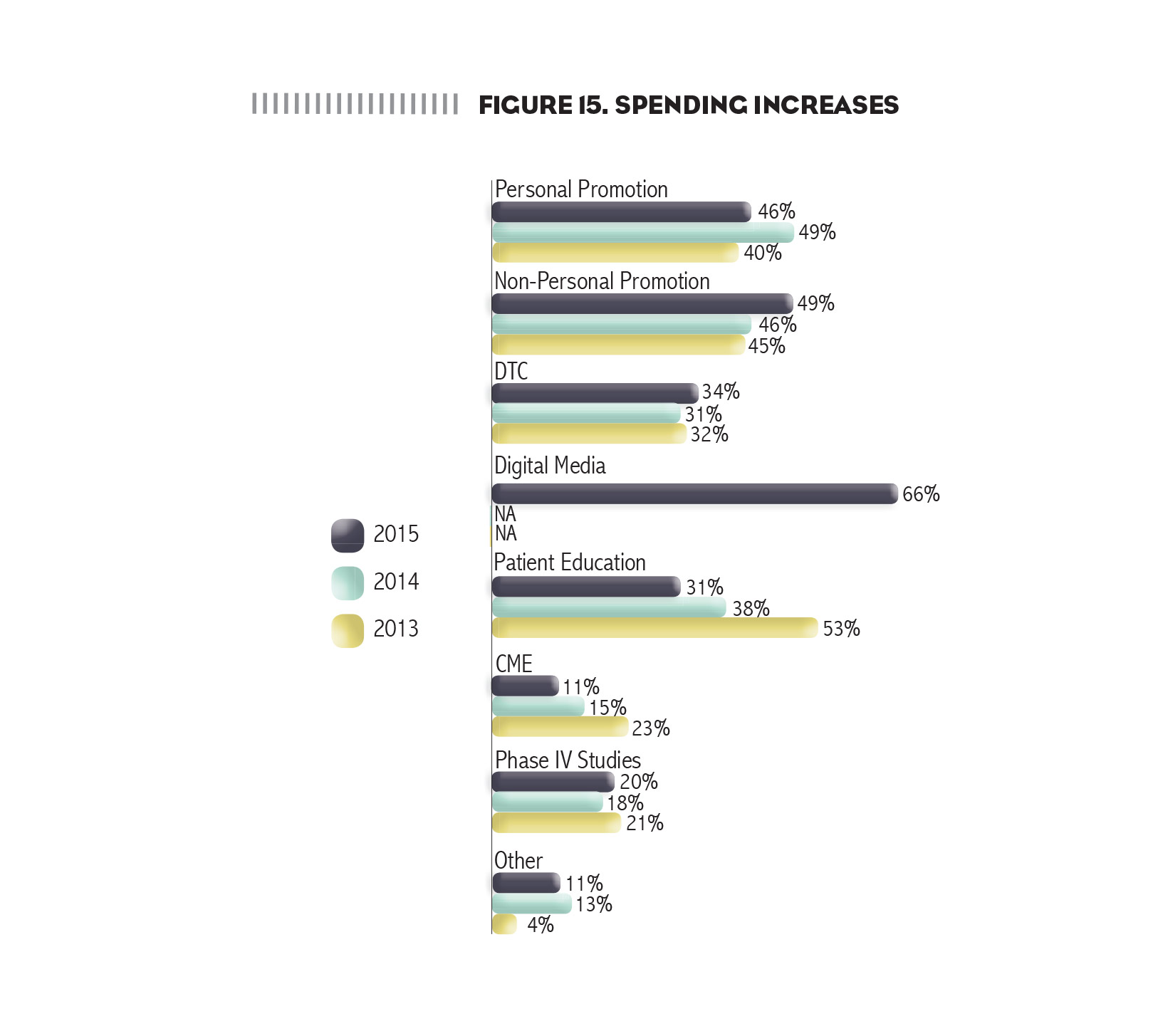

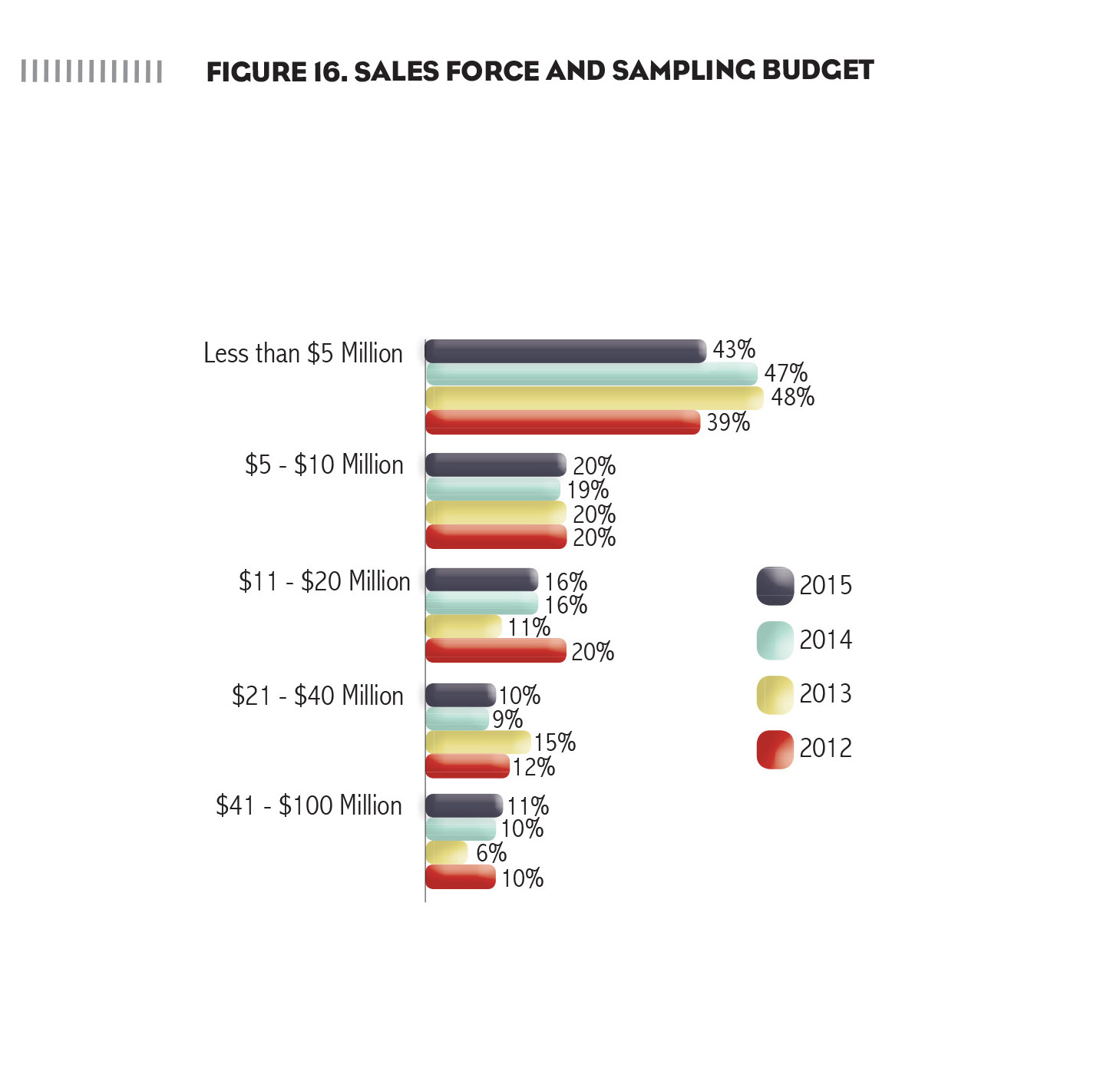

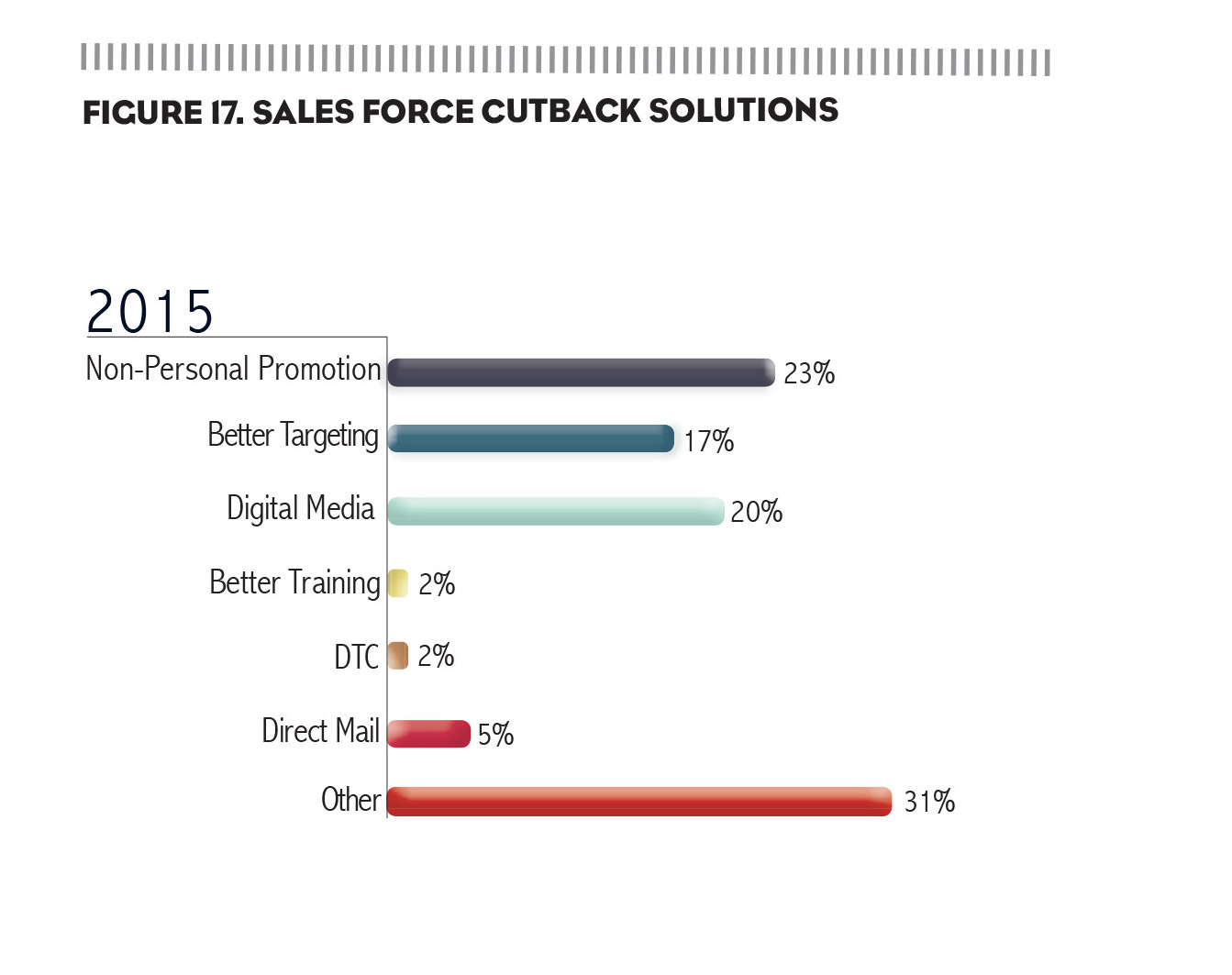

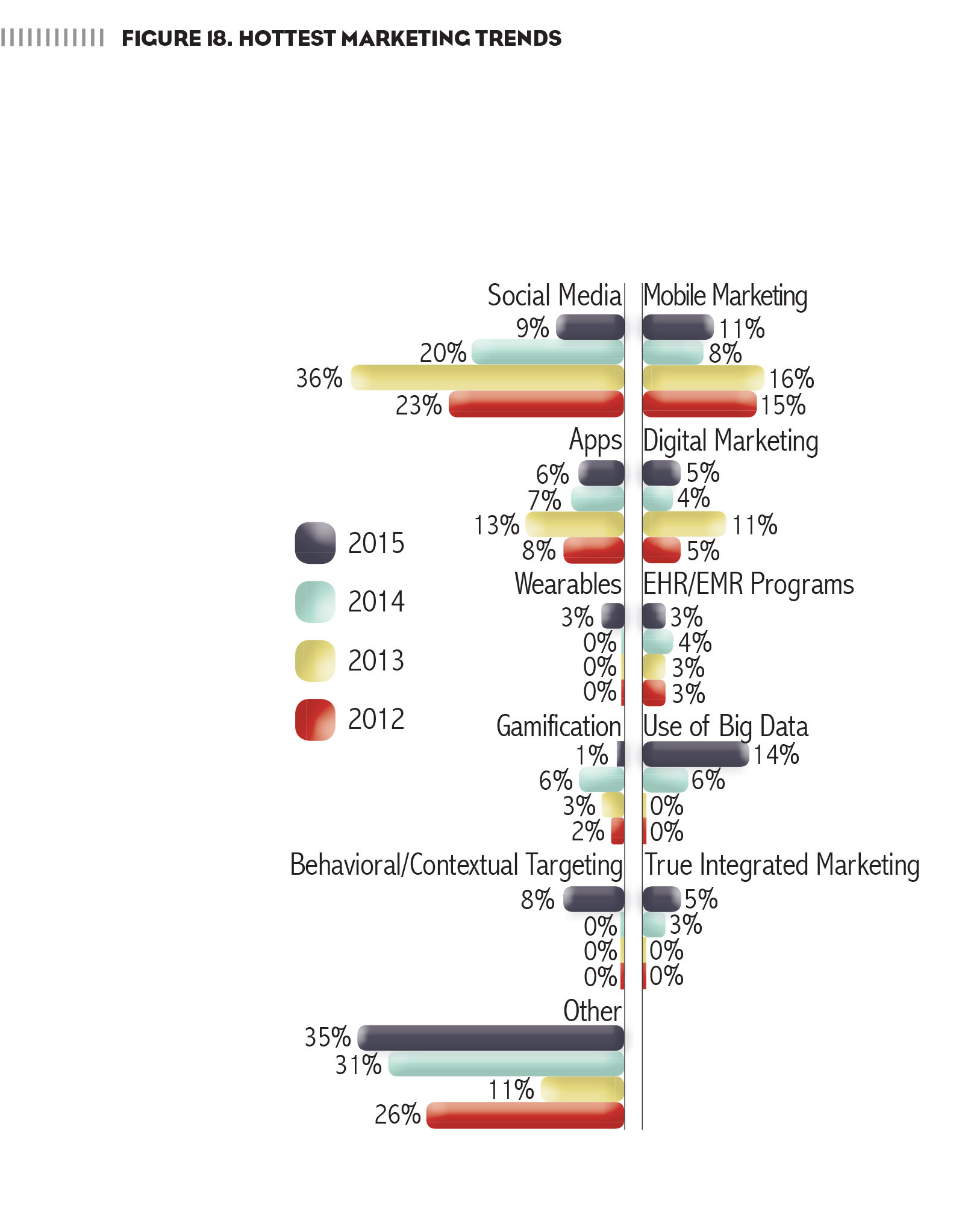

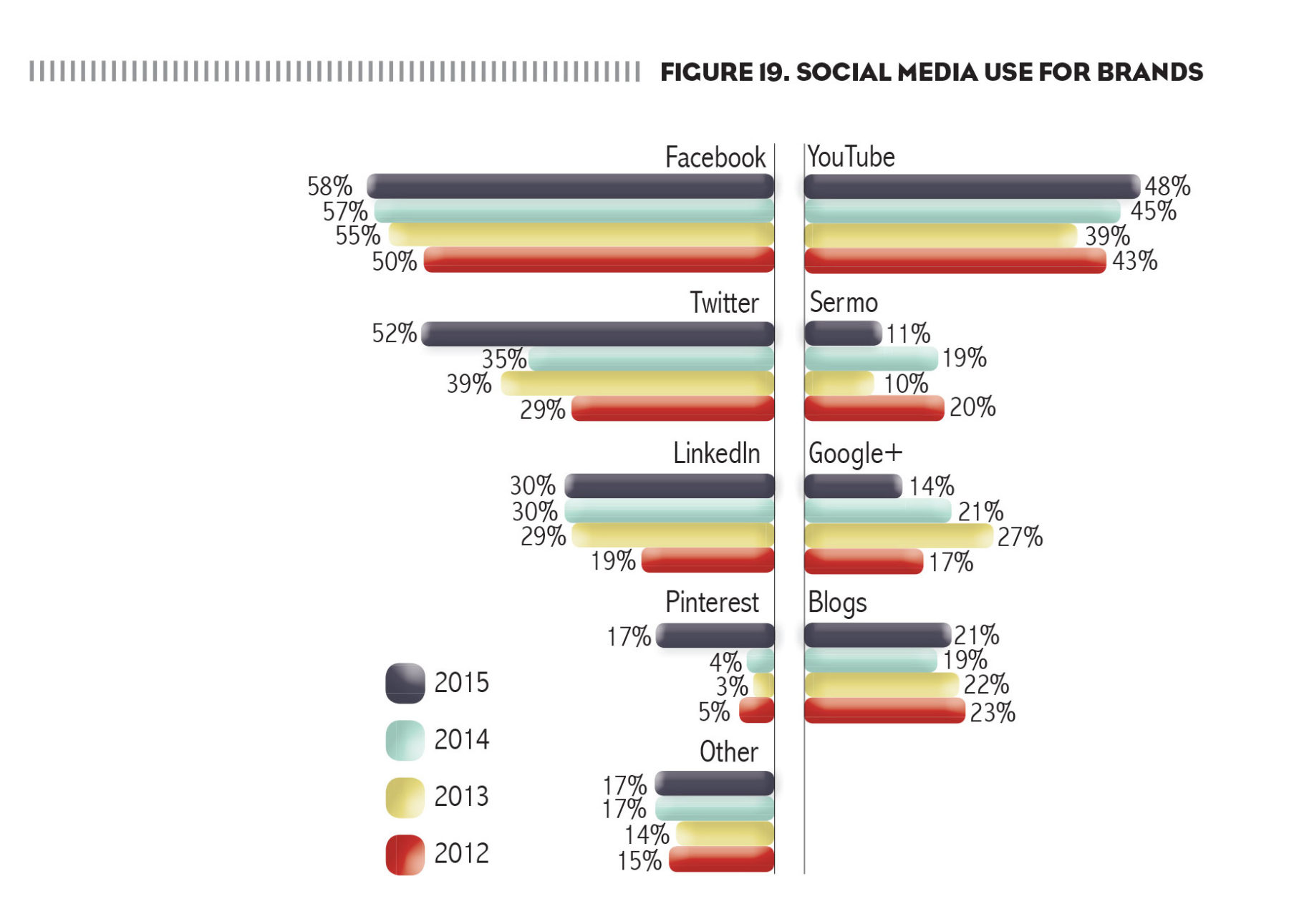

This year’s survey received more responses from within the Medical Device industry (19%) than in any previous year. Essentially, that means this group of respondents is a little more representative of the healthcare industry as a whole compared to just pharma. Over half of the responses, however, still came from Pharma (55% to be exact, which is down from 68% last year) while 16% are from Biotech. Some people didn’t fit perfectly into one of these three categories and instead listed something more specific such as Diagnostics or Specialty Oncology. In terms of the size of the company they work for, the plurality are from one of the 10 largest companies within their respective industry (Figure 1). And more than half (51%) are from a top 20 company. One slight difference from years past: We received 6% more responses from people at a boutique-sized company. Even though the average number of years our respondents worked in the industry dropped from 18 to 16, we received a higher number of responses from C-suite executives. Among our respondents were four CEOs, two Chief Marketing Officers, a Chief Commercial Officer and a Chief Strategy Officer. Of course, the plurality of respondents’ titles is more akin to VP/Director of Marketing (34%) or Product Manager/Director (24%), but regardless of title, the overall brand experience of respondents is a bit higher. Four in 10 have worked on six or more product launches—a 5% increase over last year, which had set a new high for this survey (Figure 2). And yet overall, the average respondent worked on about the same number of product launches as last year’s respondents (3.9 vs. 3.8) as well as total brands (14 both years). But employees aren’t accruing all of that brand experience with one company. In fact, the average number of years a respondent spent with his/her current company decreased from 7.8 to 6.9. Consequently, the number of respondents who have been at his/her current organization for less than two years increased—by 12%. It sure seems as if some of these respondents felt the effects of the constant layoffs and mergers and acquisitions, but at least they have been lucky enough to land on their feet. Nearly 30% of our respondents are making more than $200,000, which is an 8% increase over last year and the highest that percentage has ever been (Figure 3). However, the increased number of C-suite executives probably has something to do with that because despite the increase in the highest salary bracket we ask about, the mean salary of respondents actually decreased from last year ($153,200 compared to $155,000). And the number of people making less than $100,000 increased by 5% (14% compared to 9%). Another indicator that more of our respondents are at the C-suite level, 9% of them said they were authorized to sign off on more than $1,000,000 for an individual initiative. Only 5% had that kind of authority last year. Despite the fact that more respondents had to change organizations in the last two years—or maybe due to that fact—overall satisfaction in one’s current position actually increased over last year. As always, we asked respondents to rate their level of satisfaction on a scale of 7 (very satisfied) to 1 (unsatisfied) for a variety of factors affecting their day-to-day jobs (Figure 4). If we consider satisfaction to be a score of a 6 or 7, then 61% are happy with their current position overall compared to 53% last year. Once again, respondents also seem pleased with their relationships with their bosses (59% in 2015 vs. 62% in 2014) and their brand teams (50% both years). But this year they see more opportunities for career growth (46% vs. 37%), are happier with their salaries (47% vs. 40%) and are more positive regarding their company’s regulatory environment (36% vs. 28%). But not everything is going the way respondents would like. If we consider unsatisfied to be a score of a 3 or lower, then this year’s respondents are not as happy with their current brand resources (31% vs. 25%). And even though the percentage of respondents satisfied with their brand teams was unchanged from a year ago, 7% more of respondents reported being less then pleased with their current team. After a one year sabbatical, social media is once again the top resource for respondents to turn to for information on how to manage their careers. We asked respondents to rate the importance of the resources they use for career information on a scale of 7 (extremely important) to 1 (not important at all). Last year, respondents considered print magazines, the digital editions of print magazines and eNewsletters as their top three go-to resources, which shows a stark difference from 2013 when social media reigned supreme. Not only did social media retake the top spot, but 20% more rated it as important (a score of a 6 or 7) compared to 2014—which is also a 10% increase from 2013. That does not mean print is dead, as print magazines are the 2015 respondent’s second most important resource followed by eNewsletters. As always, RSS feeds and blogs are viewed as the least important, but fellow perennial bottom feeder, mobile apps, is actually on the rise—the amount that considered apps important increased by 10%. Marketers were also asked to rate the importance of the information sources they use to manage their brand on that same 7-to-1 scale (Figure 5). For the most part, respondents in 2015 and 2014 had the same view on where to turn to for insights to help their brands. Competitive intelligence (80%) was overwhelming considered as the most important resource (the combined score of a 6 or 7), and industry news (58%) came in second. But industry meetings and events took over the third spot from FDA alerts as 10% more respondents feel that conferences are key. Social networks, meanwhile, are viewed as less unimportant, but still not a crucial resource for brand information. Practically the same percentage of respondents consider social networks as important (25% vs. 23%), but 9% less of respondents are willing to just dismiss social out of hand. For marketers, there is nothing quite like successfully launching a new product. For the fifth straight year, the plurality of respondents considers a product launch to be their greatest success (Figure 6). But after that, respondents are fairly varied on what they look back on most fondly. Crafting a particularly successful campaign was the second most named response at 10%. And for the first time, we asked respondents to specifically consider their success with digital initiatives, and 9% felt that their work in digital is what they deserve the most kudos for. Meanwhile, one of last year’s top answers was regarding the ability to problem-solve by cleverly navigating a difficult regulatory, resource or other constraint, but that response saw a 3% drop from last year. The biggest drop, however, was the number of marketers taking pride in their work educating patients or working with advocacy groups. That is a tad surprising considering the importance most organizations are putting on patient centricity these days. But what is not surprising is the achievement that rose the most from last year: The ability to grow, or at the very least, maintain revenue figures saw an increase of 4%. It is no secret that today marketers face increased competition from other brands, so the ability to either maintain market share or even surpass expectations is certainly something worth smiling about. One respondent mentioned “opening new markets in additional countries” while another said “launching a specialty hub which tripled Rx in six months.” The sources of respondents’ greatest marketing disappointments are a little different from last year (Figure 7). Yes, once again, dealing with internal miscommunication, red tape, delays, reversals, etc. that destroyed viable market opportunities was the greatest cause of respondents’ stress. But insignificant budgets followed closely behind as the second biggest source of disappointment and rose 7% from last year. Regulatory delays, requests for more data, narrow labeling, special requirements, etc., which reduced commercial opportunity, also rose back up to pre-2014 levels. Which means after a year off from hearing complaints—most likely rightfully so—about a lack of funds as well as frustration dealing with regulatory issues, 2015 is much more in line with what we heard from respondents in every year except 2014. The thing that is different from previous years, including 2014, is the amount of respondents upset over a well-conceived program that failed because of delays, internal disagreements, miscommunication or other factors. Only 7% considered poor execution their greatest disappointment, a 5% drop from 2014 and a 6% drop from 2013. And just like in successes, this is the first time we asked respondents to consider a digital media failure and 6% considered such an occurrence as their No. 1 cause for their current ulcers. Meanwhile, one respondent said his biggest distress is the “lack of quality marketing talent,” specifically old-fashion, insight-driven marketers. Every year, we ask respondents to not only rate the factors that had the most impact on the industry in the past year, but also to forecast what to expect next year (Figure 8). Our 2014 respondents pretty much hit the nail on the head for every major influence except one. Just look at the numbers: Product Pipeline (our 2014 forecasters scored the potential impact as a 28 while our 2015 respondents actually rated it as 27), Outsourcing (8 vs. 9), Regulatory Environment (24 vs. 23), Mergers (17 vs. 16) and Competition (17 vs. 17). The one area they missed on was the Political Environment in which they predicted a score of 23, while the 2015 respondents only felt it was a 16. Perhaps our 2014 respondents believed the midterm elections (which occurred a few months after they already took the survey) would have a larger impact on the ACA. If so, they weren’t completely wrong as the Republicans did manage to get the Supreme Court to review whether a clause in the ACA was constitutional, but as you know the act was upheld. So maybe the real political impact will be felt in 2016 when the country elects a new president. Our 2015 respondents are predicting a 3-point increase in the impact of politics on pharma in 2016, so maybe visions of Trump, Bush, Clinton or Sanders do have pharma insiders excited or scared for what’s to come (we’ll leave it up to you to decide which means which). But before looking too far ahead, let’s examine how this past year actually went. Once again, Mergers kept pace with its increase from last year. In 2015, we saw Actavis merge with Allergan, and then Allergan agree to sell its generics business to Teva, which then dropped its bid to acquire Mylan, which eventually merged with Perrigo. Meanwhile, Pfizer acquired Hospira. Mallinckrodt bought Therakos. And IBM purchased Merge Healthcare to help further develop Watson. And then there are mega-proposals that didn’t happen such as Shire’s bid for Baxalta. Or Horizon Pharma’s continued attempts to get Depomed. It is enough to make your head spin and there is no end in sight. Our 2015 respondents predict the impact of Mergers to grow ever so slightly with a 2016 score of 17. The Product Pipeline continues to have the largest impact, and our respondents are also worried about increased competition from biosimilars and generics. Respondents also mentioned the increased importance of payer marketing in both 2015 and 2016, and the way in which marketers will need to deal with pricing concerns coming from both payers and the public. We also included Digital Media as a new impact to consider and respondents rated it as an 11 this past year, but expect it to be even more important in 2016 with a score of 15. One respondent specifically mentioned an increased focus on multichannel marketing. It is a good thing that marketers find so much satisfaction in launching new products, because this year’s respondents have more brands that will be ready for launch in less than six months than in the history of this survey (Figure 9). In fact, the number of respondents on the precipice of launching a new product increased by 7%. But the biggest difference from last year is the decrease of respondents with a brand in the pre-launch phase, which dropped by 8%. So ultimately, that means the number of new products this year’s marketers are working on overall is about even. More good news for this year’s respondents: They saw a significant increase in their brands’ market share compared to last year’s respondents. In 2014, only 47% saw their market share increase even a little—this year 57% of respondents have experienced an increase. Even though respondents report being concerned about increased competition, they have faced virtually the same amount of direct competitors as last year’s respondents (an average of 4.2 this year compared to 4.3). This year’s marketers are also more confident about how they stack up against their fiercest competitors as 67% feel they are in very good shape—only 60% felt similarly last year. Respondents are, however, down a little on their brand’s individual attributes compared to last year (Figure 10). We asked respondents to rate the competitiveness of several attributes of their brand on a scale of 7 (very competitive) to 1 (not at all competitive). Compared to last year’s respondents, marketers are a little less confident in their clinical profile (64% rated it as a 6 or 7 in 2015 compared to 74% in 2014), resources/budget (23% vs. 29%), non-personal promotion (25% vs. 30%) and medical education (30% vs. 33%). On the other hand, 2015’s respondents feel better about their sales force support (41% vs. 37%) and company regulatory environment (26% vs. 23%). They are even less down on their DTC efforts as only 42% rated it as a 3 or lower while 46% did the same a year ago. For the first time, we also asked our respondents to rate the Digital Media efforts of their brand and the results were mixed: 29% rated it favorably while 27% rated it unfavorably. For all of the news about budget cuts in pharma, our respondents’ average marketing budget is actually up significantly from the last previous years (Figure 11). The mean marketing budget for this year’s respondents is $17.6 million, up from $14.7 million last year and even 2012’s nearly $17 million. But it appears that mean may be skewed by some top-heavy responses—perhaps from the increase of C-suite executives taking the survey—as those with a budget in the $41 to $100 million range rose by 5%. Meanwhile, the number of respondents with a budget under $10 million isn’t that far off from last year (62% vs. 65%). And despite the increase in average budget, only 39% of respondents feel that their budget is high enough to help them remain competitive—nearly half (48%) felt similarly last year. However, marketers are allocating their budgets almost identically compared to last year (Figure 12). Two slight differences are the drop in direct-to-patient advertising, which is down 3%, and then the 3% increase in direct to HCP. Those aren’t necessarily connected, but perhaps this year’s respondents are a little more worried about trying to reach “no-see” physicians compared to patients. The other change: We added Digital Media as an option, which grabbed 14% of our average respondent’s budget. With that addition, our respondents are devoting about 30% of their budgets to digital (Internet, Social Media and Digital Media). The other channels in which marketers are investing include trade shows, customer insights, pharmacies and market development. But going back to that 30% devoted to Digital Media/eMarketing, that figure is actually down 6% from last year when you look at the breakdown of non-personal promotion spending (Figure 13). That money was instead spread out with small increases in eDetailing (15% vs. 13%), Journal Advertising (17% vs. 14%), Dinner Meetings (30% vs. 28%) and Point of Care (15% vs. 13%). In fact, every NPP category dropped at least a little except for Internet/eMarketing, which rose by 4%. Perhaps, marketers are just turning to different digital channels to reach HCPs. Once again, the news doesn’t quite match with our results—for the fourth consecutive year the percentage of respondents who experienced a budget cut within the last year actually decreased. The percentage steadily declined from 42% to 40% to 36% to 23%, which is the largest drop yet. But maybe we have just gotten to the point at which there is less to cut. However, the rate of cuts, for those who did have to deal with a decreased budget, increased by 4% over last year (this year’s respondents saw an average cut of 24% compared to 20% last year). And where our respondents choose to cut from looks dramatically different from last year, but that is probably our own doing (Figure 14). As we have done throughout this year’s survey, we added Digital Media as a choice, where applicable, considering the rise in such initiatives. And that is the area in which respondents were most likely to slash. But that also helps clarify what forms of personal and non-personal promotion marketers were cutting all of those years that we didn’t have Digital Media as an option. We are also seeing significantly fewer cuts in Patient Education (15% vs. 31%), CME (19% vs. 35%) and Phase IV Studies (15% vs. 33%). But it may be too early to read into such drastic changes as the addition of Digital Media has shifted most of this year’s numbers. The other areas that marketers mentioned cutting include conventions/events, HEOR research, pharmacy and savings cards. The dramatic drop in the number of respondents who saw their budget cut did not equate to a significant hike in budgets for our other respondents. Only 32% of respondents saw their budgets go up (compared to 29% last year), which means the plurality (44%) simply saw no change at all. But the average hike is way down from last year—22% compared to 46%. That figure is more in line with the previous year, though still down, as 2013’s respondents saw an average hike of 30% and in 2012, it was 26%. As we typically see each year, the area in which marketers are most likely to cut is also the one they are most likely to invest in when they have the extra cash to do so (Figure 15). A whopping 66% of marketers invested their superfluous cash flow into Digital Media, while most of the other areas remained similar to last year with differences of only 3% to 4%. The one exception: Patient Education, which dropped by 7%. Just as we saw for marketing budgets, sales force and sampling budgets are up from last year (Figure 16). While the increases of only 1% in the top two largest budget brackets ($21 million to $40 million and $41 million to $100 million) are small, there was a 4% decrease in those with a budget under $5 million. Combined, those differences help raise the mean budget to $15.9 million—a $1 million increase over last year. Almost half (47%) also report that their sales force and sampling budget increased over the past year—only 38% saw an increase last year and just 28% in 2013. And the average hike for those with increased budgets also grew from last year—29% vs. 21%. Once again, this seems to go against the endless slew of stories about sales force cuts we have been hearing for the past year. Merck, Amgen, GlaxoSmithKline, Abbott, and more have all reported layoffs. And yet, 55% of respondents report that their sales force actually increased this year. Just less than half of respondents (49%) said the same last year with an average increase of 17%. The average hike of sales forces this year: 25%. However, that does match up more closely with what we heard in 2013, when 54% of respondents had larger sales forces that grew by an average of 18%. Meanwhile, 45% of 2015’s respondents report working with a decreased sales force (compared to 51% last year and 46% in 2013) with an average cut of 19% (17% in 2014 and 19% in 2013). For those who need to find alternative avenues to reach physicians thanks to a depleted sales force, the most common solution is once again non-personal promotion (Figure 17). That means respondents are turning to more digital channels as well as boosting their eDetailing efforts. Others are more focused on improving their targeting techniques. As one respondent put it, “Focusing specifically on high-value targets and areas where we are already winning versus finding new growth opportunities. It’s about getting better where we are already winning.” While another claimed the way to go is “better training for sales forces, reducing clutter in their bag, hyper-focused messaging.” Some other solutions mentioned include a greater emphasis on patients with more DTC campaigns, consolidated territories, white spacing, direct mail, mailing samples, increased CE efforts, reminder calls to top deciles and refocusing share of voice efforts. While one simply said, “Working more hours.” Everyone in this industry can sympathize with that respondent. Finally, after five long years, social media is no longer considered the “hottest new marketing trend” (Figure 18). Yes, we came close last year as Social Media’s 20% was topped only by “Other” at 31%, but the Other category is commonly filled with a hodgepodge of responses rather than one trend that everyone is talking about. Of course, we don’t quite have that this year as Other still dominated with 35%, but Big Data, or more specifically how marketers intend to use it, is the top actual trend that have respondents buzzing. And while it is listed that only 14% of respondents mentioned something about using Big Data that can easily be combined with the 8% that mentioned Contextual or Behavioral advertising since that also relies on Big Data to deliver more targeted campaigns. In fact, when you also factor in the respondents that mention programmatic, geo-targeting, personalization, automation and similar concepts, nearly 25% of respondents are excited about new ways to target digital campaigns. Is one quarter of responses enough to name 2016 as the Year of Ad Targeting? Beyond just targeting advertisements, respondents also mentioned behavioral understanding and prediction, the use of Big Data to track customers every move, and increasing stakeholder engagement through apps utilizing behavioral cues/targeted messaging capabilities. So after years of collecting Big Data, it seems that marketers are finally finding ways to use the information gleaned to their advantage. Of course, some of the old stalwarts remain as well. Mobile Marketing was mentioned by 11% of respondents but nothing too specific about what they plan to do in the space, 6% mentioned Apps and Social Media is still hot for 9% of respondents. The idea of “true” integrated or multichannel marketing was brought up by 5% of respondents, so there are certainly some who believe—probably rightly so—that marketers can create campaigns that better combine the various channels at a marketer’s disposal. A few would like to see marketing directly through EMR systems and 3% look forward to what wearables offer. Additionally, there were quite a few interesting one-off responses such as altruistic marketing campaigns, blogging especially on medical-related topics, Internet of Things, interventional oncologists, marketing to new stakeholders such as payers, population health management, personalized medicine and social gaming. One also mentions, “Virtual detailing and use of more distant access to reach KOLs—especially those in hard to reach academic and university settings.” Others are focused on better ways to reach patients through patient educational brochures, direct to patient support services and by leveraging patient reported outcomes (PROs), while one just claims, “Nothing seems that new.” By this point, it is probably safe to say marketers know they have most of the information that the FDA is going to give them about social media. Anything new that comes from the FDA will probably be in the form of more draft guidances limited to a very specific area, such as the three the FDA released last year, or new information that comes about as the result of a warning letter such as the one Duchesnay received when Kim Kardashian posted a picture of herself with the morning sickness treatment Diclegis on Instagram—and a message extolling its benefits but not its side effects. Then again, that warning letter may not have really revealed anything new, but just reaffirmed rules that marketers hoped deep down weren’t true. But marketers now know the rules and that knowledge has seemed to impact their use of social media for their brands (Figure 19). Yes, most of the figures are nearly identical to last year, but look at Twitter—up 17%. One of the guidances that the FDA released last year was focused on social media platforms with character space limitations. And while many felt the rules laid out in that guidance would limit how pharma could use a site such as Twitter, it seems the guidance only liberated marketers to finally see what Twitter has to offer. The other social media platform that experienced a huge growth was Pinterest—17% this year compared to 4% the previous. The FDA rarely mentioned Pinterest directly, but it did come up in two warning letters in fall of 2014, one to Young Living of Utah and the other to d’TERRA International—both cited false claims about their products. And the FDA draft guidance on correcting third-party misinformation online could help with Pinterest considering the concern about user comments on posts. Perhaps those documents have been enough to ease marketers concerns and encourage use in a platform they have rarely used. But not all social media use grew in 2015. Both Sermo and Google+ dropped by 8% and 7%, respectively. The use of Google+ also dropped by 6% the year before so that continues a downward trend for the site, but Sermo was on the way up. Respondents mentioned a couple of other social sites including Doximity, a professional networking tool for physicians and HCPs, and Yammer, a private social network that helps employees collaborate. Meanwhile, 9% of respondents still don’t use any social media, either because the company doesn’t allow it or speed to market is not worth undertaking. But overall, 73% believe that social media use will increase next year, and now that marketers feel more comfortable with the rules of the road it is a safe bet they will be right. Thanks To Our Respondents From These Companies: 3M Drug Delivery SystemsIndustry Breakdown

Brand Experience

Salary

Satisfaction

Resources

Successes

Disappointments

Influences

Lifecycle

Attributes

Budget Allocation

Budget Changes

Sales Force and Sampling

What’s On the Horizon

Social Media Use

AbbVie

Advanced Medical Systems Inc.

Aesculap

Alcon Laboratories Inc.

Alere Inc.

Alexion

Allergan

Amgen

AngioDynamics

Aqua Pharmaceuticals

ARKRAY USA, Inc.

Astellas

AstraZeneca

Baxter

Bayer Healthcare

BD

BioTek Instruments, Inc.

Boehringer Ingelheim

Boston Biomedical

Braintree Laboratories

Breckenridge Pharmaceutical, Inc.

Bristol-Myers Squibb

Colorado Biolabs Inc.

Cook Medical

Corcept Therapeutics

CSL Behring

DePuy Synthes Joint Reconstruction

Eddingpharm

Eisai

EMD Serono

Entera Health

Essential Pharmaceuticals

Ethicon, Inc.

Everett Laboratories

FemmePharma Global Healthcare

Ferndale Healthcare

Ferring Pharmaceuticals

Fibrocell Science, Inc.

Galderma Laboratories, L.P.

Galen

GE Healthcare

Genentech

GlaxoSmithKline

Grifols

Horizon Pharma

Inovio Pharmaceuticals

InterMetro Industries Corporation

Intuitive Surgical

Ipsen US

Isis Pharmaceuticals

Janssen

Mederi Therapeutics Inc.

Medtronic Neurological

Merck

Mylan

Myriad Genetics

Nexgen Pharma

Novartis

Novo Nordisk

Novocure

Orexigen Therapeutics, Inc.

Oxford Biomedical Research

Pall Corporation

Paragon Vision Sciences

Pfizer

Pierre Fabre

Purdue Pharma

Roche

Sanofi

Sanofi Pasteur

Silvergate Pharmaceuticals

Synergy Pharmaceuticals

Takeda Pharmaceuticals

Teva Pharmaceuticals USA

Tulex Pharmaceuticals

UCB

ViiV Healthcare

Watson Pharmaceuticals Inc.