Understanding the diverse international HTA environment and the nature of individual agency decisions is of growing importance for the development of an optimal health economic and outcomes research strategy.

Today, there are a growing number of health technology assessment (HTA) agencies around the world, some more prominent and systematic in their approach, but all undertaking some form of HTA evaluation. Their approval and reimbursement decisions vary considerably, even when reviewing similar efficacy, safety and economic data, with a consequent variable impact on a drug’s market access profile. And the situation continues to evolve; even countries with more mature processes are still searching for the optimal HTA model.

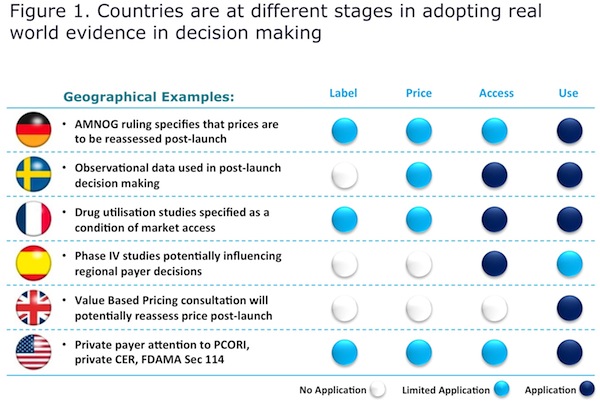

For health economics and outcomes researchers, the diversity and heterogeneity of HTA agencies create enormous challenges, including constantly changing evidence requirements, inconsistent availability of appropriate data, variability in methodology and interpretation of that data, and ultimately demonstrating product value across disparate markets. Real-world evidence, for example, is one data element that is used increasingly in decision-making but to different degrees in different countries (Figure 1).

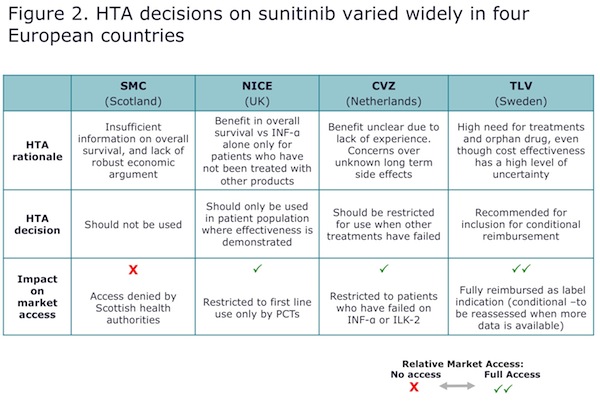

The extent to which HTA outcomes and guidance vary across countries can be seen in the case of sunitinib for renal cell carcinoma (RCC), which received very different ratings from four independent European HTA agencies focused on cost-effectiveness. As shown in Figure 2, the rulings ranged from full (conditional) reimbursement by the TLV (Tand-och Lakemedelsformansverket) in Sweden to complete denial of access in Scotland following review by the SMC (Scottish Medicines Consortium), reflecting their very different perceptions of the drug’s “value”.

Growing Need For a New Understanding

Understanding the diverse international HTA environment and the nature of individual agency decisions is thus of growing importance for the development of an optimal health economic and outcomes research strategy. The challenge is being able to leverage prior learnings and incorporate them as far as possible into the clinical trial program to ensure a positive early reimbursement decision from each of the respective HTA bodies. For manufacturers developing a market access strategy, this requires answers to a number of key questions:

- Did the HTA agency evaluate similar products previously – either a clinical comparator or pricing comparators? If so:

- Did they interpret the clinical data in the same way?

- What were the key drivers of negative/positive appraisal decisions?

- How likely is it that an appraisal by one HTA will impact appraisals by others?

- How can the learnings from previous appraisals be strategically leveraged to maximize the likelihood of a positive reimbursement decision?

- If the new product is first-in-class, is there another disease state that could be used as a proxy to assess how HTA agencies are likely to appraise it?

To address these issues, there is a clear need within HEOR to monitor the influence of the information being provided to HTA agencies and leverage it for the improvement of research over time. This knowledge can serve as the basis for:

- Discussions with clinical development to determine the design of the Phase II/III program in relation to: the comparator or comparators that are likely to be faced in reimbursement decisions across multiple jurisdictions, the endpoints (primary and secondary) and effect size.

- Discussions with commercial functions to inform decisions around pricing, launch sequencing and the access level that is likely to be achieved, for forecasting and other functional purposes.

- Formulary and reimbursement submissions as the basis for designing economic evaluations, modeling assumptions, cross-country communication and pricing negotiations.

Systematic Approach to Data Collection

The optimal approach to collecting HTA data will vary by organization size, level of sophistication and the involvement of local affiliates. Responsibility may be assigned to a global HEOR group, local operating companies or an external vendor, depending on availability of manpower, resources and budget. In terms of timing, monitoring ideally should begin prior to the design of pivotal Phase II/III studies by engaging payers or advisors at HTA agencies early in development to establish key endpoints, continually appraise them, and update as decisions are made.

The collection process should give consideration to HTA reviews on competitors but also data on the new compound itself—which can serve as an important internal resource for applying key learnings across the organization’s portfolio of products. Addressing future launches and/or indications that may be planned for the same compound is also important. The ultimate goal should be a systematic process that includes: regular updates as decisions are made by HTA agencies; details of discussions leading to decisions (where available); and provision for tracking future reviews to anticipate competitor activity.

A key issue from a company perspective is to ensure that the collection of data is combined with systematic analysis, i.e., understanding not only the decision that was reached but also the rationale or discussions around it to facilitate forward planning for the type of challenges the compound might face related to reimbursement.

The value of systematic collection lies in the immediate access to the data, which is shared across all functional areas within the company and resonates in a way that can influence decisions at key points during research and development (R&D). Done well, such a process can enable:

- Avoidance of potential pitfalls in future submissions and a better understanding of data requirements in each market

- Identification of possible data gaps within the clinical trial program and other targeted HEOR projects

- Understanding of the methodologies (accepted/rejected) around health economic models that should be implemented early on or at the time of submission

- Development of more innovative tactics in price negotiations with the HTA/reimbursement authorities by learning from competitor successes and failures

Application of HTA Data in Oncology

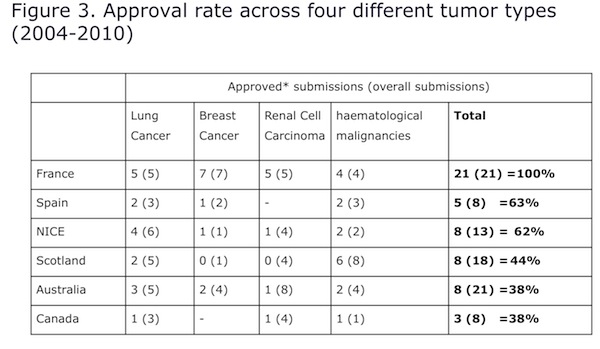

Oncology is one key therapy area that has attracted increasing attention from payers in recent years following major scientific breakthroughs and strong growth in sales. Based on HTA decisions, product uptake rates vary from one country to another. Analysis of submissions in six countries (France, Spain, England, Scotland, Australia and Canada) between 2004 and 2010 shows that approval rates across four different tumor types (lung, breast, RCC and hematological malignancies) averaged close to 60% (Figure 3).

For RCC only, the approval rate was 32%—the lowest among the four cancers. From a country perspective, France had the highest percent of HTA approvals for RCC while Australia and Canada had the highest number of rejections. This variation among countries remains true for other tumor types.

Also evident is the growing number of submissions for lung cancer in recent years. In general, positive reviews have also been on the rise, reflecting advancements in treatment for this disease. However, in breast cancer, where medical progress has been more pronounced, the market is somewhat crowded compared to other tumor types. Thus, while the number of submissions is also similarly on the rise, there is no clear trend regarding positive and negative approvals by these agencies. However, in the case of hematological malignancies, almost all submissions were approved, reflecting the unmet needs in this area.

1. Drivers of negative outcomes

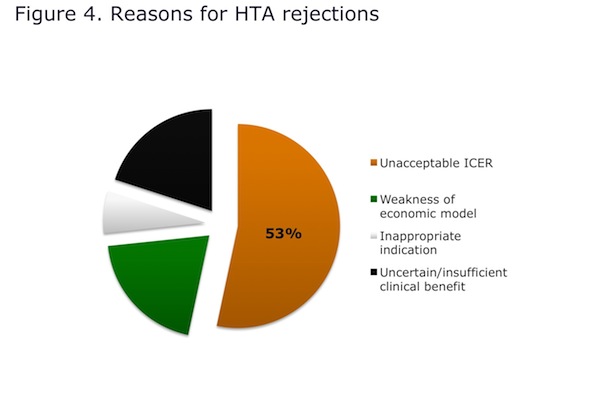

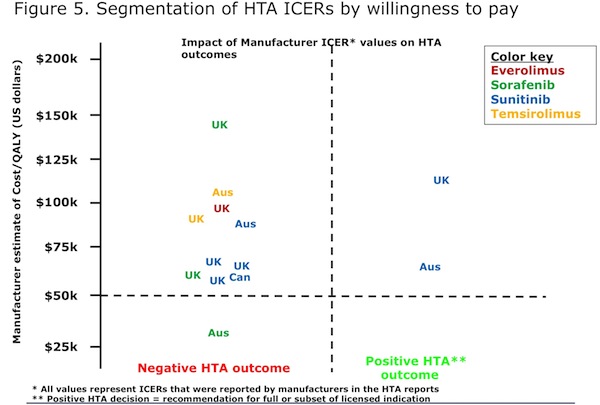

Most HTA rejections in RCC were the result of unacceptable economic analysis, specifically “unacceptable ICERs”—a label that is open to wide interpretation (Figure 4). More granular analysis of HTA decisions for RCC in Australia, Canada and the UK shows that most of the ICERs exceeded a $50K willingness-to-pay threshold, resulting in a negative outcome (Figure 5). However, in two cases where the ICER was also above this level (Australia, UK) sunitinib was approved for use. Why?

- Australia: In 2007, the manufacturer of sunitinib approached the Australian PBAC three times for feedback. On the first occasion, there was no economic model included in the dossier so the submission was rejected outright. The second time, the cost/utility for adverse events had been omitted and progression-free survival proxied for overall survival. Finally, on the third attempt, the manufacturer was able to address all the previous requests and, through price negotiations, reduce the ICER to an acceptable level and ultimately gain access in the country.

- UK: Also in 2007, several submissions were made for sunitinib in the UK, where potential denial of access to the drug had triggered a public outcry. Through the ensuing negotiation process, NICE began to rethink its framework for determining reimbursement, particularly in relation to the issue of prolonging life for patients with few therapy options. Sunitinib was eventually approved for a subset of patients where the drug had proven survival benefits compared to immunotherapy. NICE has since been giving more consideration to equity issues and the possibility of applying some form of weighted threshold for different diseases.

2. Impact of survival data

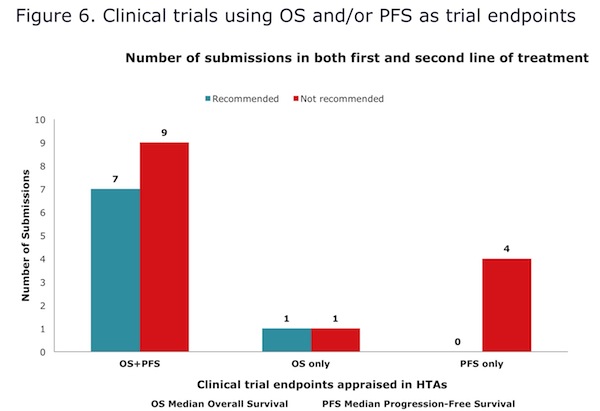

A further interesting and very relevant analysis is the degree to which overall survival (OS) versus progression-free survival (PFS) has impacted HTA decisions. On the basis of the data collected, there is no discernible salient association between OS and PFS and HTA impact in this particular tumor type. However, it is of note that all trials using PFS without OS were rejected (Figure 6).

3. ICER differentials

Historical HTA data for RCC reveals significant disparities between the ICER estimates submitted by manufacturers and those developed by the agencies themselves, due largely to different assumptions in economic models. This signals potentially protracted negotiations to adjust the numbers during a period when time is of the essence and pricing discussions would also be ongoing. The key message here is that by ensuring robust data and a reasonable price behind the ICER, there is an opportunity for manufacturers to reduce the negotiation period from approval to reimbursement/access, and by doing so, also minimize the opportunity costs of time lost during that process.

Take Home Learnings

Every situation is different; the lessons vary from one tumor type to another and each approach must be tailored. Knowledge of emerging comparators, products in the pipeline and other developments that will shape the future must also be drawn into the mix. However, purely based on the historic data, there are some key lessons to be learned in this area:

- Robust evidence from well-designed trials: Clinical trials must be flawlessly designed and trial data used appropriately when submitting to HTA agencies, especially in terms of the patient group, line of therapy, outcome measures, and increasingly in the case of RCC, as well as in other tumor types, treatment sequencing and use in combination.

- ICERs: Price negotiations are increasingly based on ICERs. The ICER is essentially an analytical tool employed by HTA agencies for price reductions, re-negotiations and commercial arrangements. The fact than an ICER is high does not necessarily imply automatic rejection. Even if a drug is deemed not cost-effective, there are other vehicles by which manufacturers can gain access in those countries.

- Value-based pricing and risk-sharing agreements: In 2014 the UK will move into value-based pricing, signaling the need for even greater consideration of volume/price trade-offs between sub-populations, and a premium price versus broader indications and a lower price; in Italy and a number of other countries, the use of risk-sharing and commercial arrangements is growing. Future performance is thus becoming just as relevant as data from clinical trials for price and volume negotiations—and increasing the importance of RWE. Value-based pricing will be more common in the future and payer management is likely to increase, despite the low budget impact of RCC.

- Country implications: In Canada, the UK and Australia, few products were reimbursed and approved, especially in RCC. The access opportunity for new products in RCC will be similar to current therapies in the near future, with the greatest payer hurdles in these countries.

- Survival endpoints: All trials using PFS without OS as an endpoint were rejected. Trial endpoints must be carefully chosen: traditionally challenging markets demand both OS and PFS; in other markets, PFS may be sufficient for access and uptake as second-line positioning. Purely basing trials on OS is lengthy, difficult and financially burdensome but these are areas that need to be considered more carefully.

- Quality of life: Although most quality of life data favored the products under assessment, most corresponding HTA outcomes were negative (apart from France). It is possible that if future products for RCC are able to avoid or reduce certain toxicities, especially Grade 3/4 adverse events that require suspension of treatment and therefore risk compromising efficacy, then those products are likely to be heralded by these agencies.

Future Impact of HTA on New Products

HTA decisions are becoming increasingly influential in the success of new compounds as more countries establish HTAs and require formal submission, impacting not only HEOR but all functional areas involved in the drug development process, including pricing, market access and government affairs. As HTA engagements grow ever more complex, with greater emphasis on RWE, a coherent strategy is imperative to maximize the likelihood of positive reimbursement.

In order to manage the evolving trends, monitoring HTA data has a valid and growing role to play in informing HEOR and reimbursement strategies. There is a greater need not only for real-time access to HTA data in different countries but also for the intelligence behind the decisions and the way they are made so that this can be leveraged in internal decision making. With a growing number of NMEs in the pipeline, there will be more and more HTA engagements and a greater number to consider for their impact on development. At a time of immense constraints on resources, finding the most efficient and expeditious way of doing this will be key.

This article summarizes presentations from the IMS Symposium “International HTA trends and implications for an optimal health economic research strategy”, held during the ISPOR 17th Annual International Meeting in Washington, DC, in June 2012.