Although the concept of Integrated Health Systems (IHSs), aka Integrated Delivery Networks (IDNs), is not new in the healthcare space, recent and rapid changes due to healthcare reform, as well as financial pressures on the healthcare market, are generating greater and swifter integration across traditionally siloed channels. The increased focus on quality and coordination of care, as well as financial challenges, leads to more centralized decision-making and greater levels of control.

What Exactly is an IDN?

At the fundamental level, the largest limiting factor is not lack of money, technology, information, or people but, rather, the lack of an organizing principle that can link money, people, technology, and ideas into a system that delivers more cost-effective care (i.e., more value) than current arrangements. An IDN is a network of organizations that provides or arranges to provide a coordinated continuum of care services to a defined patient population and is willing to be held clinically and fiscally accountable for the outcomes and health status of the population served.

The various services and stakeholders that may or may not comprise an IDN—such as hospitals or hospital systems, large medical groups, long-term care, outpatient centers, pharmacy, and/or managed care—lead to a very fragmented and nebulous market. So, the question remains: In such a fragmented space, how do manufacturers effectively build a cohesive strategy? Understanding IDNs would help pharmaceutical, biotech, and medical device companies unravel the layers of various types of IDNs, most popular being an Accountable Care Organization (ACO).

Then What is an ACO?

ACO, proposed as mechanism to slow rising healthcare costs and improve quality, is a form of IDN—an integrated care delivery model that promotes coordinated care and rewards value over volume. Groups of providers jointly held accountable for achieving measured quality improvements and reductions in the rate of spending growth, ACOs constitute networks of clinicians and hospitals who share responsibility for clinical and financial outcomes. They focus on the total patient, including acute, chronic, preventative, wellness, maintenance, and rehabilitative needs, and promote evidence-based medicine, patient engagement, and coordination across providers.

What’s Happening Today?

The enterprise customer business model is changing with more focus on patient engagement, coordinated care, and improved outcomes. With the consolidations in the marketplace and the evolving business models, the pace of change has significantly increased. In addition to the consolidating marketplace engendering more and larger enterprise customers, the roles and business priorities of these customers that directly relate to pharmaceutical use are changing, such as:

- Increased accountability/risk sharing, which is driving a focus on higher quality and outcomes at lower cost.

- Development of evidence-based disease management tools/clinical pathways and the need to measure/manage against them.

- Investing in patient support beyond the traditional provider-patient appointments.

- Discharge management and core coordination efforts in many disease areas.

Historically, pharmaceutical companies have had challenges meeting the unique needs of these most sophisticated customers, and the performance within these groups continues to be a challenge. The traditional marketing model typically is not effective given the high proportion of “no-see” physicians and the increased decision-making at the institutional rather than individual physician level.

A study by IQVIA showed:

- 50% prescribing business flowed through IDNs.

- IDNs reduced brand share by 20% to 25% nationally.

- IDNs reduced overall Rx volume by about 10%.

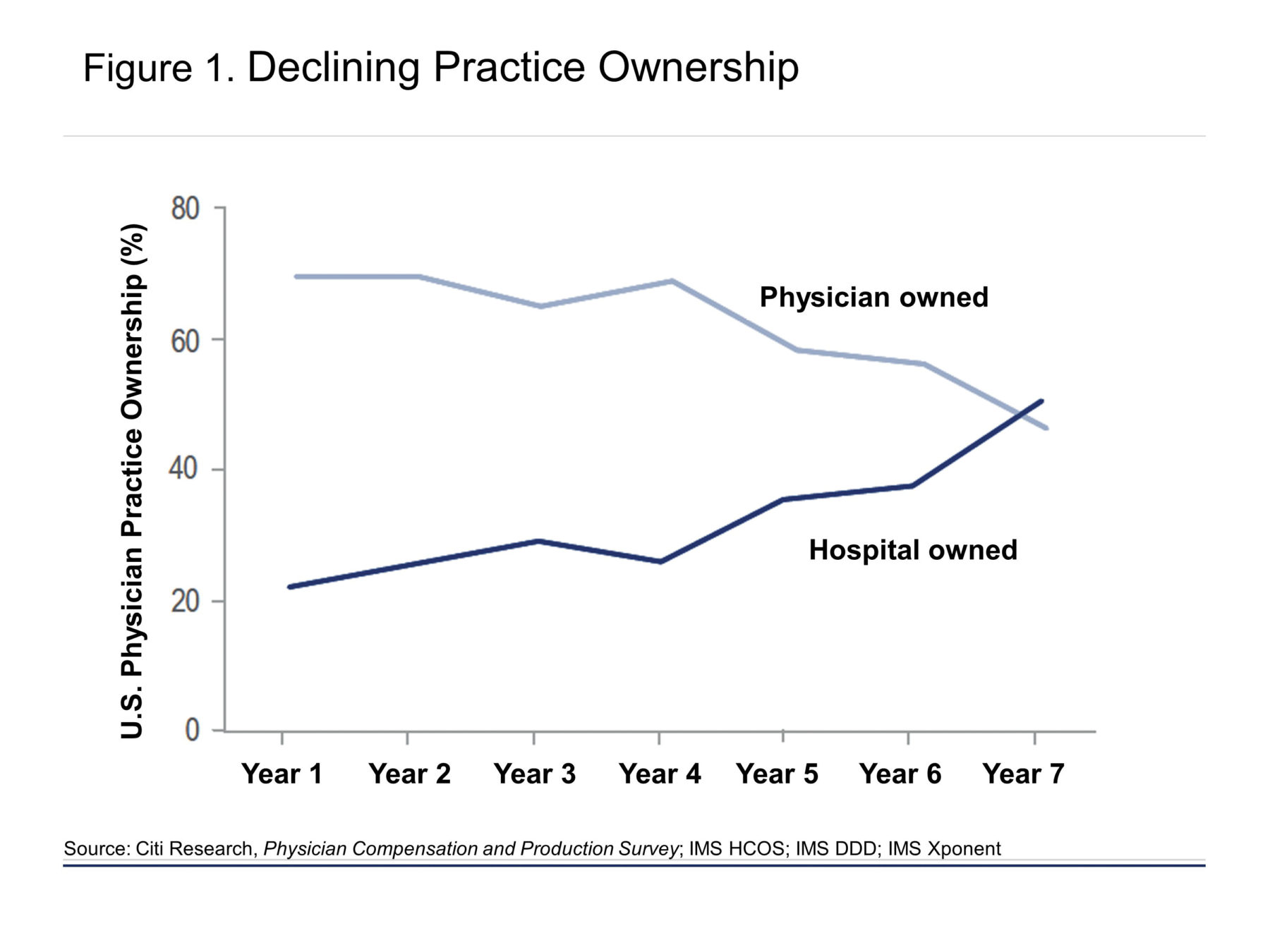

Deteriorating practice economics have triggered major changes to the structure of the delivery system. Private practice is eroding in favor of larger, hospital-affiliated settings (Figure 1), which is eroding returns from traditional physician details (Figure 2). The majority of U.S. physicians are now employed or affiliated with a hospital group or an insurer as a result of more practice mergers and hospital acquisitions.

The changing landscape is making traditional promotional tactics less effective. Equivalent detailing effort has a different impact depending on the IDN and physician affiliation. New customers and organizational forms are exerting meaningful influence on prescribing dynamics. The impact of IDNs is growing, with integrated payer/provider entities now exerting more influence on product selection than managed care in certain geographies. Although IDNs’ control has steadily increased over time to a level comparable to that of payers, both nationally and locally, current investment in IDN access lags investment in payer access, a trend that will need to change going forward.

Pharma companies now fully recognize the traditional commercial model is insufficient. As a result, a significant number of alternative elements have been trialed (both broadly applied and piloted), and continued change is on the horizon, with 83% of respondents expecting to further restructure their commercial model in the next two to three years based on our commercial survey conducted at the end of last year.

In adopting these changes, alternative personal selling models (e.g., key account management for institutional providers) are deemed most successful. However, results have been more mixed on “what” is provided—e.g., content, offerings, and services have not been as successful as expected. More broadly, pharma companies continue to wrestle with broader barriers to evolving the commercial approach.

Pharma executives, in light of these results, need to:

- Adopt and ensure best practice execution in strategic moves showing the most promise broadly.

- “Redesign” the offerings, services, and digital models not yet delivering needed value (mainly through incorporating a more “customer-centric” view of value/appreciation).

- Address operational barriers required to evolve to a more complex and sophisticated commercial approach—including setting goals and establishing metrics to determine the ROI of new commercial model pilot programs to guide future decision-making and investment.

The Emergence of IDNs

The IDN customer may take on a variety of forms:

- Non-integrated Group Practices and Hospitals. Examples: Hospital Corporation of America (HCA) and Tenet Healthcare.

- Multi-specialty Group Practices, including or not including hospital affiliation. Examples: Harvard Vanguard Medical Associates, Atrius Health, Hill Physicians, Magellan Health Services, and International Multiple Sclerosis Management Practice.

- Integrated Delivery Networks. Examples: Henry Ford Health System, Mayo Clinic, Barnabas Health, and Cleveland Clinic.

- Fully Integrated Delivery and Financing Systems. Examples: Kaiser Permanent, Geisinger Health System, Banner Health Network, Optum Health, and Partners Healthcare.

New organizational structures have arisen from existing regional differences: By early 2013, there were approximately 1,200 IDNs, a 70% increase in one and a half years. Customers bearing financial risk have growing economic incentives requiring evidence showing tangible value—customer-centric evidence of real-world value is becoming increasingly important, with emphasis on clinical efficacy, quality, and value.

Strategies for Engagement

Engaging IDNs effectively requires a reconsideration of the traditional commercial model based on reach, frequency, and patient metrics. Embracing a more account-centric model is necessary to adapt to the growing influence of IDNs.

Some examples of approaches emerging throughout the industry include:

- Hybrid Sales Forces are being piloted and rolled out given that internal functions such as Sales Operations, Sales Analytics, and Marketing are under pressure to transcend traditional functional silos.

- Managed Care Account Management are leveraging their skills and experience throughout commercial organizations.

- Changes in internal business processes and analytical frameworks are being made to better emphasize the need as developing and deploying the right skills with which to engage IDNs is proving to be complex.

- Localized Customer-centric Models are being applied as customers evolve, because it is critical to tailor engagement models to local needs using novel metrics beyond reach and frequency.

- Outcomes-based approaches to marketing strategy and execution that can help align with customer priorities. Unlike the traditional approach—which focuses on what growth opportunities will maximize product utilization; what behaviors to drive; what segments to target; how to activate those segments; how to go to market; and how to manage brand performance—the outcomes-based approach focuses on:

- Customer-valued outcomes: What outcomes are valued by direct customers and stakeholders.

- Optimizing product utilization: What outcomes will drive sustainable growth.

- One view of the patient, physician, provider, and payer: For which direct customer and stakeholder segments drive outcomes.

- Engage on the customers’ terms: How to engage and motivate target segments to drive outcomes.

- Strategy built to execute at the local level: How to go to market locally.

- Realize value in weeks not months: How to measure outcomes and manage brand performance in real time.

In our opinion, at least six critical elements to consider for an IDN engagement strategy assessment are:

1. Customer Segmentation—Segmenting IDN Accounts

To understand the range of maturity of IDNs, a behavioral segmentation is useful across key dimensions. It is also useful to understand IDN accounts on their operating priorities and structures:

- Accounts that have different priorities—what are they?

- Are all needs equally valuable to address?

- Which accounts align best with your therapy area capabilities?

- How do brand strategies align with IDN needs?

- How best to systematize ways of working to address priorities?

2. Assess and Understand IDNs Operating Priorities

It is crucial to understand specific IDN objectives, reflecting their geographies, patient populations, organizational structures, payment models, and other operating drivers.

- Patient engagement: Target the right intervention to the right patient—the challenge is delivering more “wow” experiences to grow and retain the patient base. Design support mechanisms to engage patients in their care—the challenge is investing in interventions that will deliver outcomes.

- Physician engagement: Identify and establish best treatment practices—the challenge is to identify treatment protocols based on meaningful evidence. Make decisions using evidence and value criteria—the challenge is aligning physicians on care standards to improve quality and take out variation; use research linking genetics, biomarkers, imaging, etc.

- Operational effectiveness: Identify and establish best treatment practices—the challenge is using benchmark information to identify opportunities. Drive out care variation to lower costs—the challenge is the right intervention for the right patient to avoid paying for ineffective care and improve care coordination collaboration.

The key is to determine how to align the engagement approach and offerings with these objectives.

3. Identify Key Decision-makers and Influencers

Leading institutions are establishing centers of excellence around patient experience and innovation. Engaging with IDNs will require engaging with many stakeholders within the system—not only with traditional medical/pharmacy directors and physicians at the practice levels but also with VPs for Innovation and Patient Safety, Directors of Innovation, CEOs of the health system, as well as CEOs of affiliated hospitals. Therefore, it is imperative that the engagement interface will have to be at the multi-stakeholder level rather than just at the physician level. Based on the changing healthcare landscape, provider decision-making is becoming more “corporatized.” Evolution toward value orientation and centralized control (the “corporatized provider”) demands some fundamental shifts in engaging with IDNs by pharma.

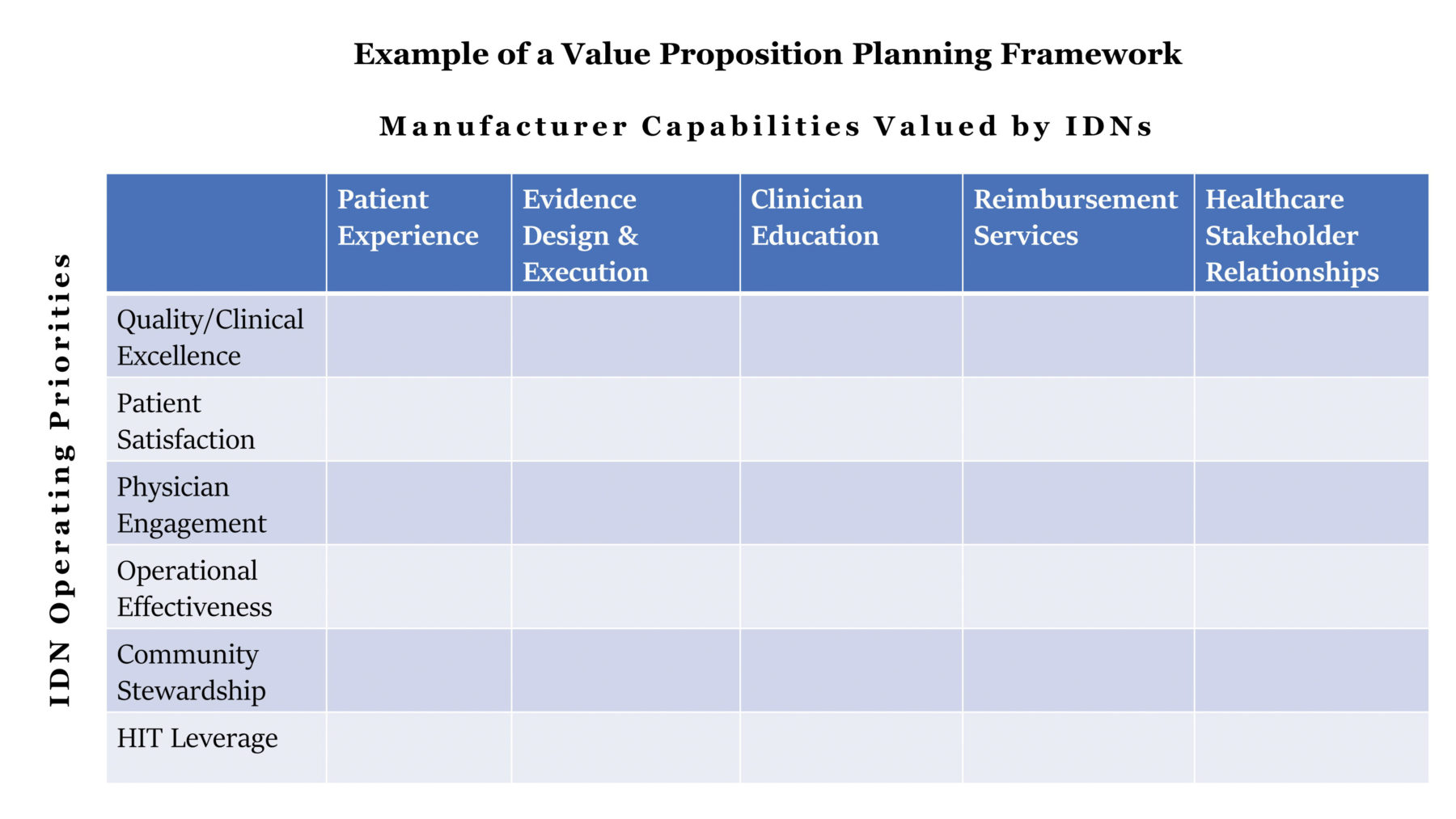

4. Introduce Capabilities that IDNs Value

Segmentation of IDNs is a starting point. However, it is important to create a value proposition for each micro-segment of the IDNs, which is key to an effective engagement strategy (Figure 3). The value proposition should address the following aspects:

- Operating priority of the IDN.

- Require a stronger, more strategic segmentation of IDN customers.

- Consider scalability and deployment of the messages.

- Mandate strong collaboration between Brand, Managed Care, Medical, and HEOR to use this framework to create alternatives.

5. Align the Commercial Model to Deliver and Measure the Capabilities and Outcomes IDN Customers Want

This mandates a pharma commercial model redesign, including new roles, processes, and ways of working both at the sales operations and field deployment from:

- Roster Maintenance: Multiple roles and positions per sales force member.

- Sales Crediting: Novel metrics and data sources at sub-national level.

- Incentive Compensation Administration: Novel metrics as well as IC plan design fostering coordination.

- Performance Reporting: Sub-national tailoring to local customer needs and performance metrics.

- Alignment and Call Plan Maintenance: Locally tailored business rules and approval process.

6. Real-World Evidence (RWE) is a Tool for Strategic Engagement

RWE can be used as a currency for discussions with IDNs on the following issues of interest to IDN stakeholders as well as in engagement strategy: Quality measures; decision support; physician P4P metrics; P4P schemes; population wellness; PRO tracking; evidence support; franchise evidence; KAM; quality measures; patient subpopulations; and patient journey tools.

Conclusion

The emerging healthcare ecosystem is already moving towards building new commercial capabilities. However, a transition plan is needed given the complexities involved in implementing these capabilities:

- Knowing which capabilities differentiate and accelerate market acceptance is key.

- Customer-facing capabilities are often prioritized, but enabling capabilities ensures long-term value.

- Capabilities are more than roles—they are cross-functional and must be built by multi-disciplinary teams.

- Capabilities must become embedded throughout the organization.

- More importantly, the “changeover” must not diminish traditional customer capabilities.

The views and opinions expressed in this article are of the authors and do not necessarily reflect the views or position of IBM organization.