Today’s Product Manager 2016

The product manager of today is, indeed, busy. While you could say that has always been true, our 8th Annual Product Manager Survey reveals they may be juggling even more responsibilities than usual. Exactly half of our respondents are working on six or more brand launches, which is a 10% increase over last year. But not only are product managers responsible for more brands, they have to carry a heavier workload as their teams are either too small or just not cutting it. Only 37% of respondents are happy with their current brand team—that figure has routinely sat around 50% during the history of this survey. So yes, the product manager of today is busy.

Product managers are also busy dealing with new influences on the industry. For the first time, the product pipeline is not the top issue keeping product managers up at night. Now, it is the payer landscape. Shocking, right. Navigating this new landscape has had the biggest effect on their jobs in the past year and they expect that challenge to continue next year. Of course, something else is on their minds when it comes to next year—our next President. And respondents have concerns no matter who is elected. They already have seen both candidates try to paint the pharma industry as the bad guy in this election—blaming them for the escalating cost of healthcare. In fact, their greatest concern is the increased pressure the next President will put on drug prices, not to mention further scrutiny of potential mergers and DTC advertising.

But then again, product managers always need to remain on their toes. This year’s respondents tell us about how they plan to handle the entrance of biosimilars to the market, what can be done to get around ad blocking technology, and which of the many novel marketing opportunities are worth investing in next year. They also share their thoughts about the overall health of the industry, and whether they will get a reprieve with larger budgets or will be forced to work even harder with fewer resources.

As always, we thank the many respondents (see their companies in the tab below) who took time out of their incredible busy schedules to complete our survey conducted by Litchfield Research between April and July 2016. Without you, we wouldn’t be able to provide this comprehensive analysis of today’s product managers and the challenges they face.

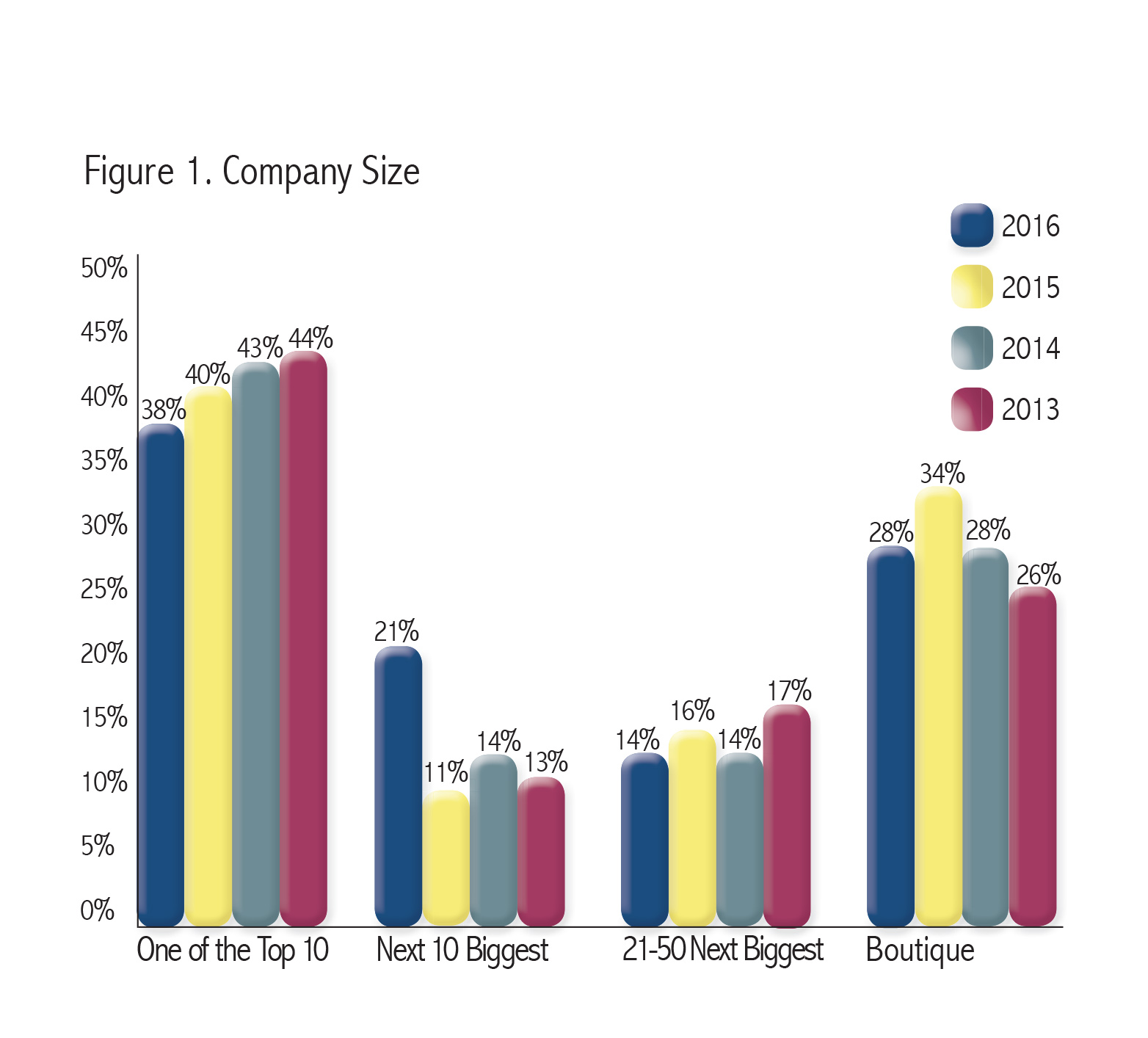

Industry Breakdown

The majority of this year’s respondents work in the pharmaceutical industry (65%) compared to 15% in biotech and 11% in medical device. These numbers are very much in line with previous years, with the exception of 2015 when we had more representation from the medical device industry (19%). A small number of respondents were from more specialized industries, such as vaccines, and a couple work in both pharma and medical device. Another difference from last year, more in line with the previous two years (2014 and 2013), is the number of respondents who work in one of the 20 largest companies within their respective industry (Figure 1). Once again, nearly 60% of respondents are currently at one of these companies compared to about 50% last year. And similar to last year, a few heads of companies, including three CEOs responded, although the majority (53%) has titles similar to Director of Marketing or Product Manager.

Brand Experience

Even though this year’s respondents worked in the industry about the same length of time as last year’s (an average of 17 years compared to 16), they seem to have far more responsibility. For the fifth consecutive year, the number of respondents who worked on six or more brand launches increased (Figure 2). But this year that number has grown by 10% (compared to a 5% growth last year and 4% the year before). The numbers lead us to speculate, as in previous years, that product managers are being asked to handle more brands as companies downsize, but this seems to be the largest support of that theory yet. Of course, it is also possible that brand managers are just being asked to work on a more diverse portfolio with several smaller brands as the number of blockbusters decreases—or they are just growing more ambitious.

Another fairly significant difference from past respondents: Time spent with their current employer. This year, 31% have only been with their current company for two years or less compared to 25% in 2015 and 13% in 2014. In fact, the average number of years a respondent has worked at their current company has decreased from 7.8 years in 2014 to 6.7 years in 2016. This is also a continuing trend that we have seen over the past few years and could be attributed to company downsizes as well as mergers and acquisitions.

Salary

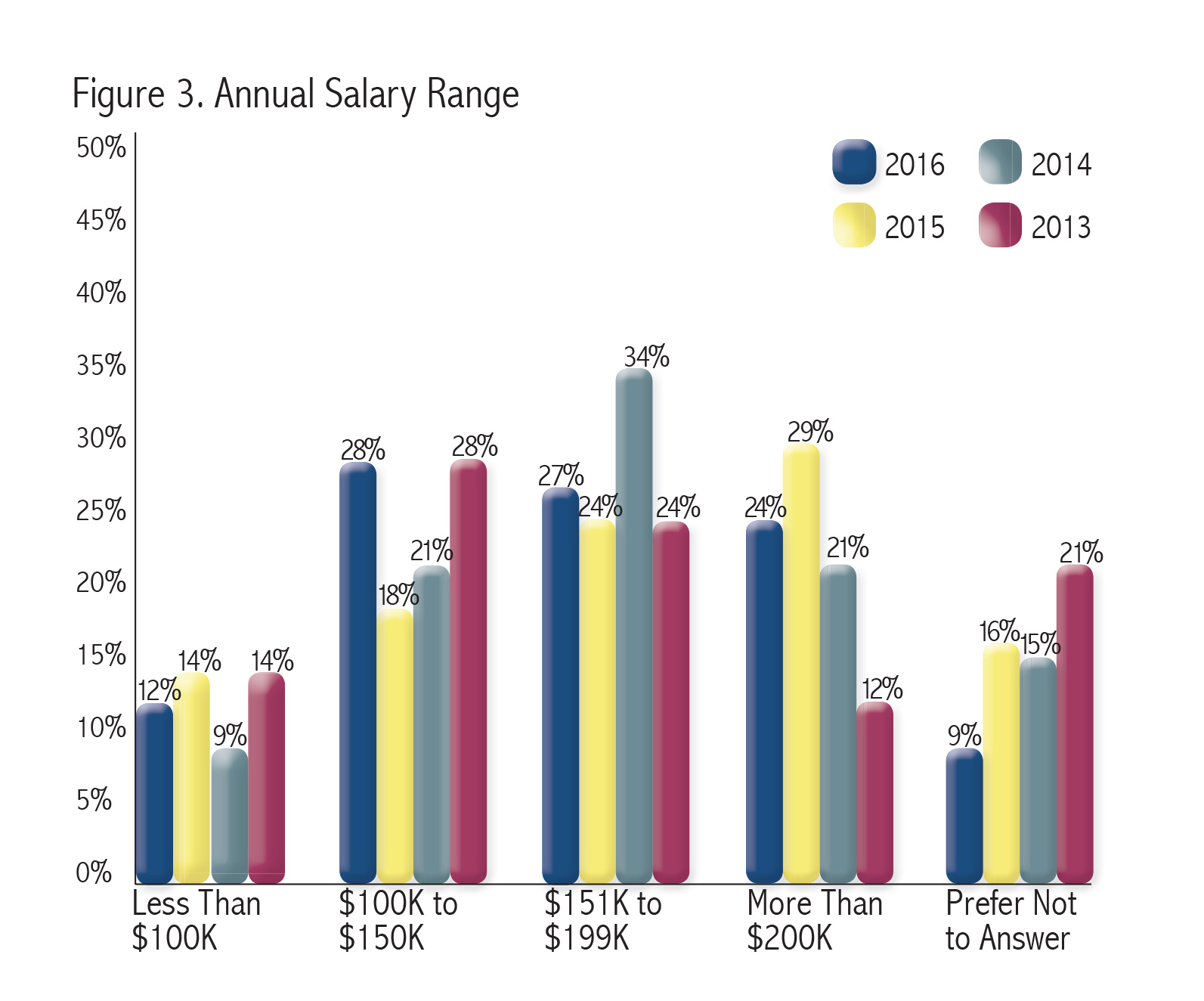

The average salary of respondents is a bit down from previous years ($150,352 compared to $153,200 in 2015 and $155,000 in 2014), but the amount of respondents making more than $200,000 is still higher than every year except 2015 (Figure 3). While the number of respondents making that amount of money did drop by 5%, the overall increase since 2013 could, in part, be attributed to an increase in responses from C-suite executives. The only other significant change in salaries compared to previous years is an increase of people making between $100,000 to $150,000, which is up 10% from last year and 7% from 2014, but is right in line with what we saw in 2013. But that could simply be due to the willingness of more people to share their salary figure as only 9% choose not to respond to the question compared to 16% in 2015 and 15% in 2014.

Satisfaction

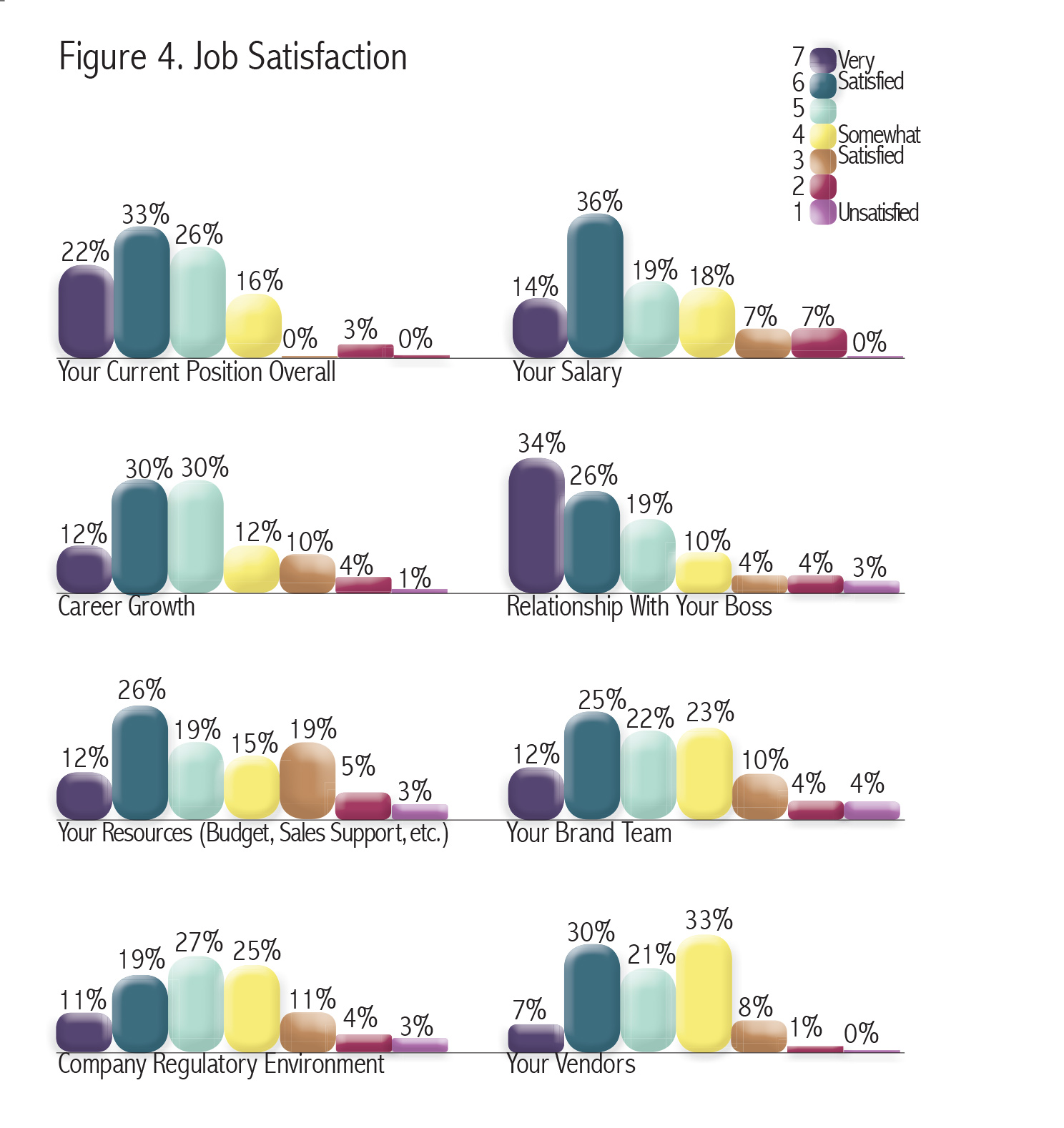

Respondents, we found, are a little less satisfied with their current position than last year. As always, we asked respondents to rate their satisfaction level for a number of factors that relate to their current job on a scale of 7 (very satisfied) to 1 (unsatisfied). In terms of their overall position, only 55% were satisfied (a score of a 6 or a 7) compared to 61% in 2015 (Figure 4). It most likely doesn’t have anything to do with their salary as 50% reported they were happy with the amount they bring home compared to 47% last year, or their relationship with their boss as 60% are perfectly pleased with the person they report to.

The biggest culprit for the increase of unsatisfied respondents seems to be their brand teams. Only 37% are happy with the group they work with, which is the lowest that satisfaction level has ever been reported. In fact, we typically find about half of respondents are satisfied with their teams. So perhaps marketers and brand managers are being asked to work on more brands with smaller teams, which is leading to more work. Or the teams are just filled with less experienced marketers. Respondents were also a little less pleased with the regulatory environment they are forced to work in (30% satisfied compared to 36% in 2015), which could also be a source of frustration.

Influences

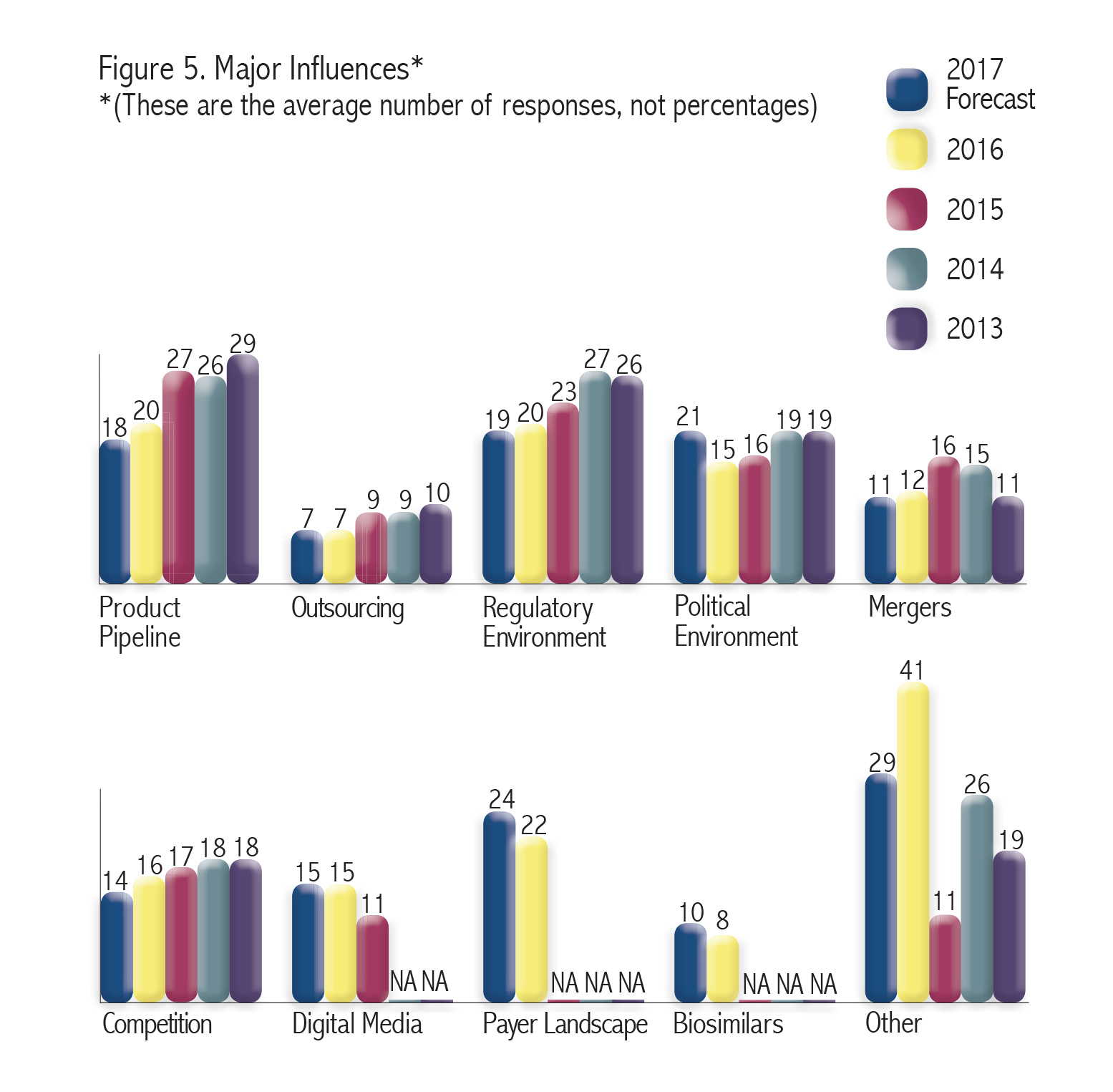

Based on our 2015 respondents’ projections, it appears things haven’t gone as everyone thought they would for the life sciences industry in 2016. Every year, we ask our respondents to rate the factors that they believe had the biggest influence on the industry during this current year, as well as to predict what will have the greatest effect in the next year by rating several factors with a score that ultimately must equal 100 (Figure 5). But our 2015 respondents’ crystal balls must have been a little foggy as few of their predictions rang true.

They rated the Product Pipeline as the factor most likely to influence how the industry operates in 2016, with an average score of 27, but our 2016 respondents rated its influence as a 20. That is also the lowest score the Product Pipeline has received in the history of this survey. Considering the fear of a dwindling pipeline is always a constant concern among our respondents, it bit surprising to see its influence level drop. But that may be due to a couple of changes we made to the survey.

This year, we added two new categories: Payer Landscape and Biosimilars. Those just happened to be the most popular write-in influences from the previous year, so we felt it was important to include them. (As a quick aside, this year’s most popular write-ins: Startups, Genomic/Genetic Testing, and Innovation.) Sure enough, Payer Landscape jumped to the top of factors impacting the industry. Respondents rated it as a 22, and only see its impact growing as they predict a score of 24 next year. That is not at all surprising considering the growing influence of payers and the contentious debates about drug pricing that have been a constant in the press throughout this year. Meanwhile, biosimiliars are not yet a major concern for respondents (only an average score of a 7 this year and 10 for 2017).

Even with those changes, it is still interesting to see how a couple of the categories that 2015 respondents felt would have a major impact fell somewhat flat in the eyes of our 2016 respondents. For instance, Mergers, which was predicted to be 17 in 2016, was only rated as a 12 by this year’s group. After all, 2016 was supposed to be “the year of merger mania,” according to PricewaterhouseCoopers. While we have certainly seen a fair share of mergers, the one that probably sticks out in most people’s minds is the one that fell through: Pfizer and Allergan. Of course, the year started off with a big one: A $32 billion deal between Shire and Baxalta, but very few of our respondents are from these companies, so the majority may have just not felt the effects of a recent merger.

Respondents also predicted a bigger impact from the Political Environment, but we have yet to see that materialize. However, our 2016 respondents, unsurprisingly, think politics will play a larger role in 2017. And to see exactly how they think the presidential election will impact the industry, continue on below.

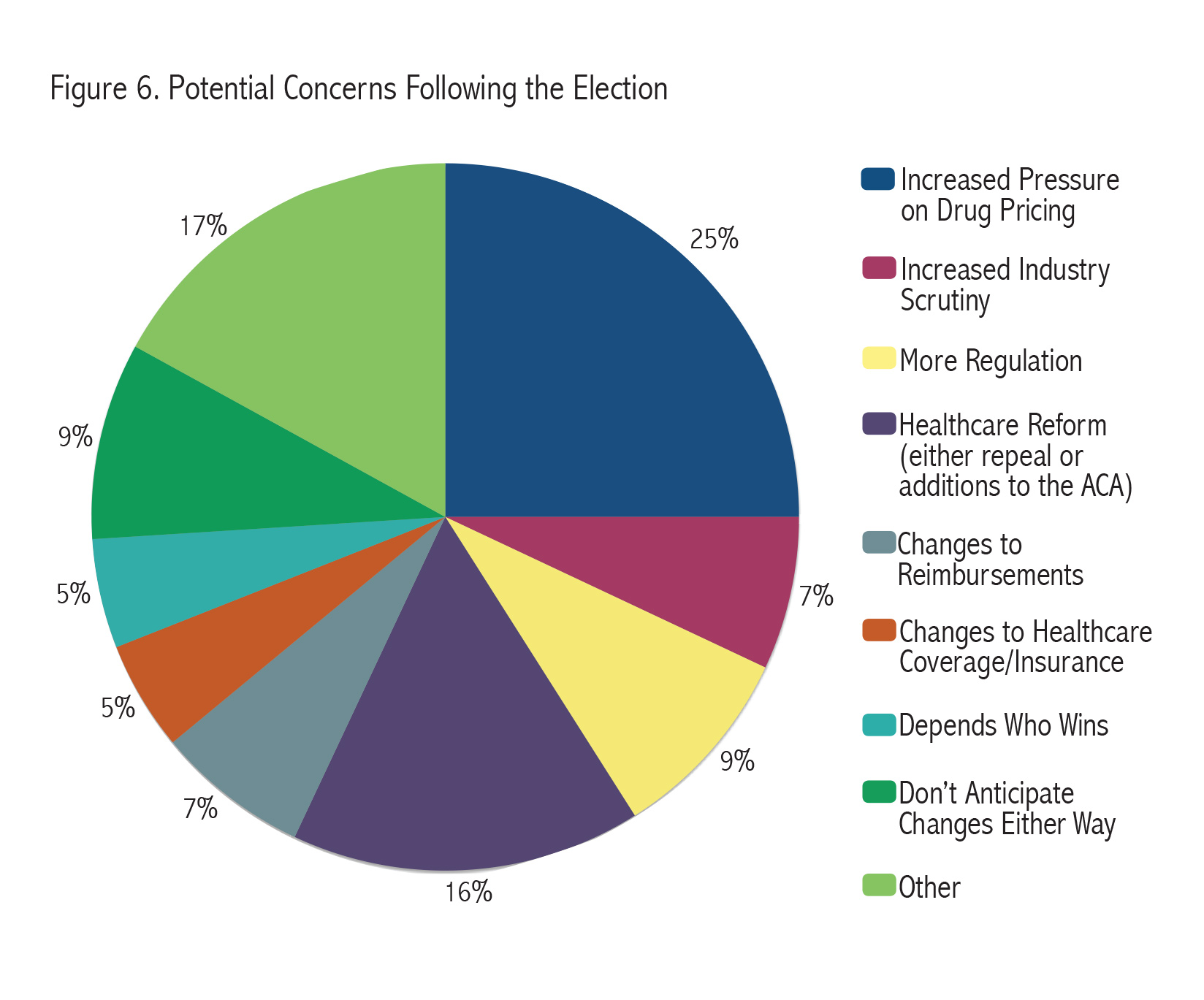

Preparing for the Future

As the country prepares to elect a new President, we asked our respondents what effect they think the 2016 election will have on the life sciences industry, as well as the issue they are most concerned about. For the plurality of our respondents (25%) that issue is the increased pressure put on drug pricing (Figure 6). As one respondent put it, “The next President will likely tackle the ‘rising cost’ of prescription medicines—something that continues to be a campaign priority for the core candidates.” Some respondents, though, think the democrats would be more likely to tackle this issue. One says, “Medicare price negotiation and recent CMS rules on ASP changes could already have a big impact. If democrats win we might see an overhaul in drug pricing which can lower gross margins for the industry.”

But many other potential effects from this election will depend on who wins. And as one of our respondents warns, “This is the type of question that creates way TOO MUCH hot air and false promises.” And we certainly did get some passionate responses. One respondent feels, “Crooked Hillary means problems for all industries. Trump knows how to run a business. Fail and succeed, but do it fairly.” Another believes, “Neither major candidate has any true knowledge of what is going on in the industry and I hope will ‘not make a real mess’ of our industry by being influenced by industry spokesmen and lobby groups, or haters of what we do and try to do.”

But the main difference in who wins comes down to what they will do about healthcare reform. “Clearly a Clinton victory and Democratic majority in the Senate and/or House would see significant differences to any changes/improvements to the ACA versus a Trump victory and maintaining GOP majority in the Senate and/or House,” says one respondent. More specifically, many respondents are keeping an eye on insurance coverage and changes to reimbursement.

Another fear among respondents: Increased scrutiny on the industry, with one specifically mentioning FTC oversight in merger portfolio consolidation while another mentions the potential delay or outright ban of DTC ads. Others feel this is all much ado about nothing. “It will have a big impact with respect to sound bites, the media, and noise,” says one respondent. “However, very little if anything will change.”

We also asked respondents how they plan to deal with another issue not related to the election: Biosimilars. Most respondents said that biosimilars will not affect their brand at this time, but we did get a few strategies on how to deal with their entrance to the marketplace for those who may be affected. Those strategies include: Aggressive contracting, great advertising, market research studies with payers and providers, mergers, payer negotiations, pipeline development, and “a strong strategy that motivates patients and caregivers—delivering a value add they can’t get from any other competitive product.” One person simply states, “Stay on our toes and meet each situation as it arrives.”

Lifecycle

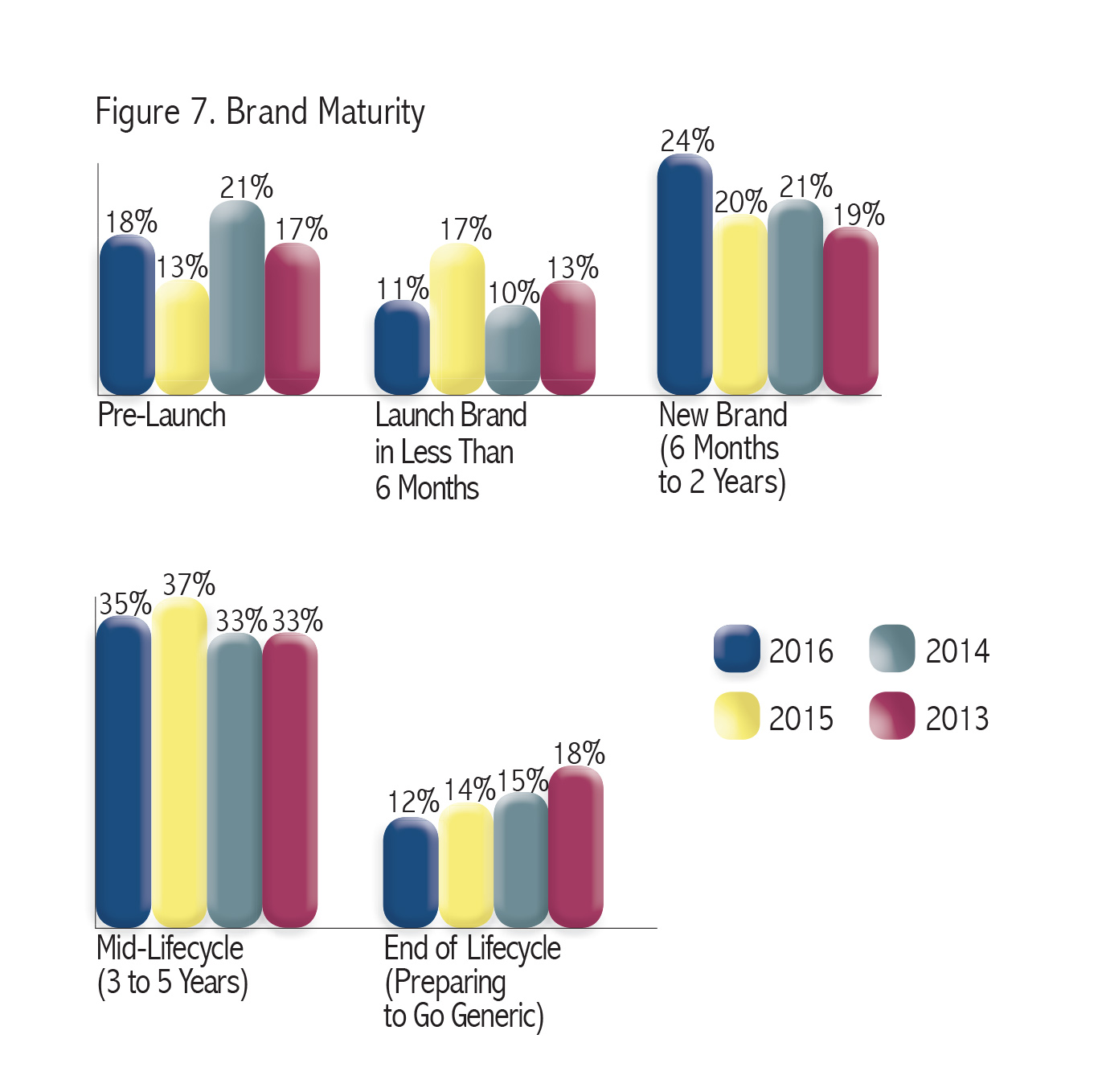

Perhaps one of the reasons respondents were a little less worried about the product pipeline: The majority of respondents are working on brands that are less than two years old (Figure 7). In fact, 53% of respondents work with brands that are somewhere between pre-launch and two years old, which is the highest that figure has been in the past three years. Coincidentally, that also means the number of respondents with brands preparing to go generic is the lowest that figure has ever been—it has dropped 6% since 2013. Another number that has dropped considerably: The number of direct competitors that a brand faces. In 2014, our respondents’ brands faced an average of 4.3 competitors, in 2015 they faced 4.2, but this year the average is down to 3.4. One potential reason for that drop could be that more product managers are working on specialized products which have less direct competition, but that is pure speculation.

Attributes

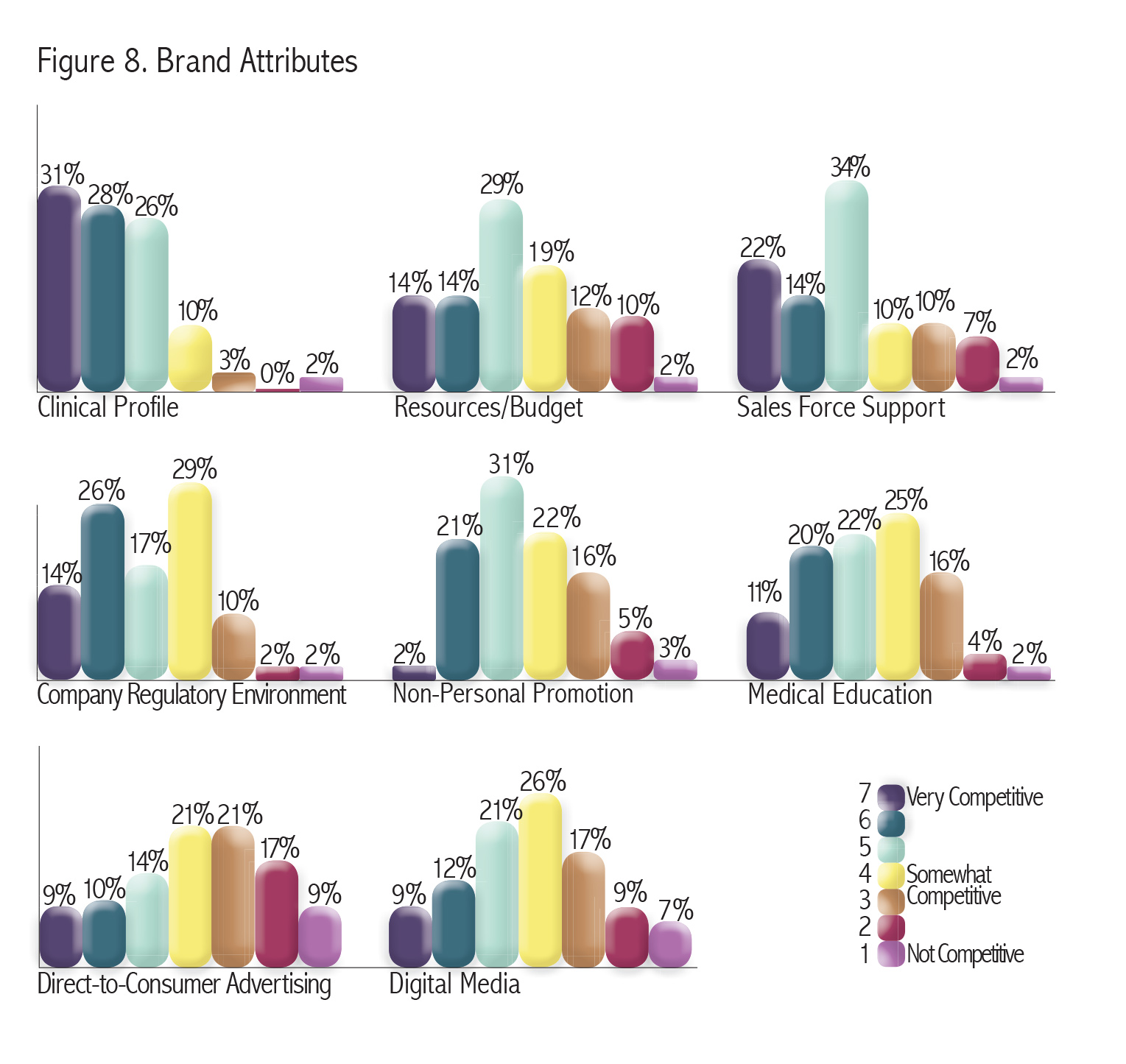

Unfortunately, the lack of direct competitors has not done much for product manager’s faith in their brands. We asked our respondents to rate how well their brand stacks up against their fiercest competitor on a scale of 7 (very competitive) to 1 (not at all competitive). Only 57% rated their brand at 6 or 7, which is a far drop from last year when 67% were confident in their brand’s ability to tackle the competition. It is also slightly down from 2014 when 60% rated their brand’s overall competiveness highly.

Unsurprisingly, that also means that respondents feel a little worse about some of their brand’s individual attributes. As always, we asked respondents to rate the competiveness of several individual brand attributes on the same 7 to 1 scale (Figure 8). Compared to last year, they feel less favorably about their brand’s clinical profile (only 59% rated it as a 6 or 7 compared to 64% in 2015), sales force support (36% vs. 41%), non-personal promotion (23% vs. 25%), DTC advertising (19% vs. 21%), and digital media presence (21% vs. 29%).

But it is not all bad news. Respondents did feel more strongly about the resources/budget they received compared to last year’s group (28% rated it highly compared to 23% in 2015). Also, respondents felt far more comfortable in their company’s regulatory environment. Four in 10 respondents rated it favorably compared to 26% last year and 23% the year before. That is a big jump compared to every other year this survey has been conducted and may be an anomaly.

But it is not all bad news. Respondents did feel more strongly about the resources/budget they received compared to last year’s group (28% rated it highly compared to 23% in 2015). Also, respondents felt far more comfortable in their company’s regulatory environment. Four in 10 respondents rated it favorably compared to 26% last year and 23% the year before. That is a big jump compared to every other year this survey has been conducted and may be an anomaly.

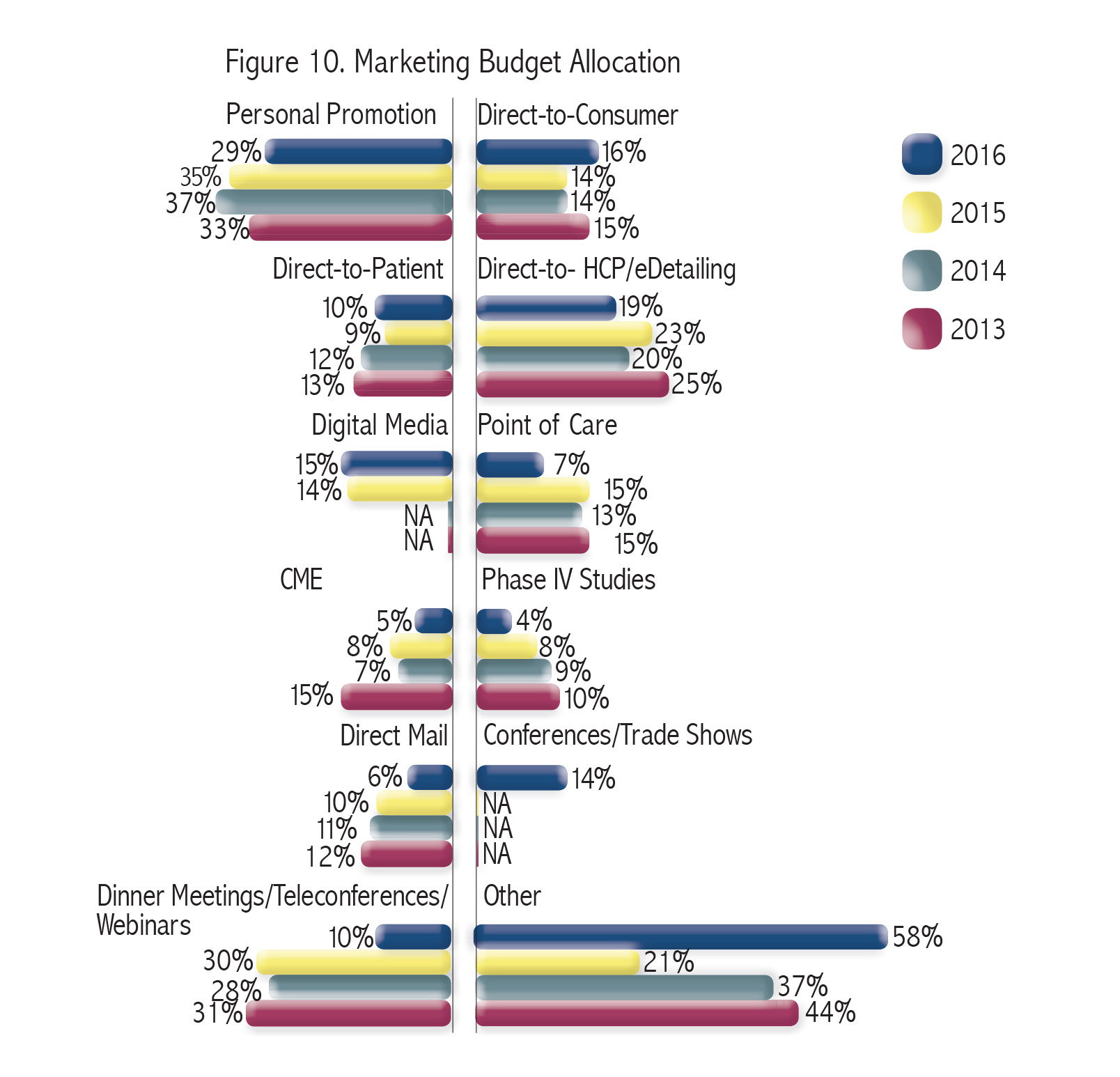

Budget Allocation

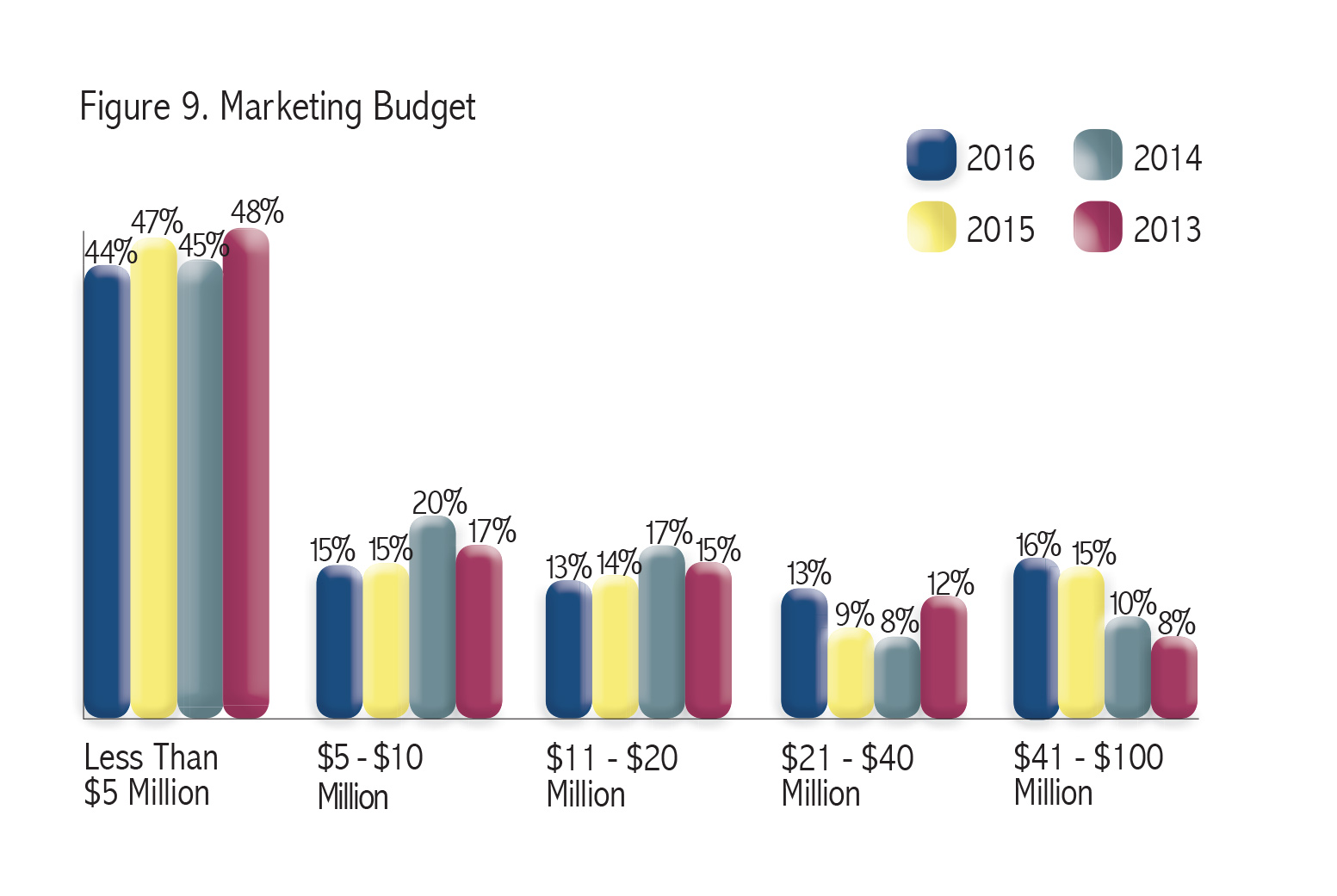

For the second straight year, our respondents buck the trend of reported budget cuts with a higher average annual marketing budget than last year’s group (Figure 9). In 2015, our respondents’ average budget was $17.6 million, which was up $14.7 million from 2014. This year, that figure is even higher: $19.6 million. The biggest jump from the previous year is that marketers with a budget in the $21 to $40 million range increased by 4%. Respondents are also much more comfortable saying that their budget is sufficient enough to remain competitive. Only 38% of respondents felt that way last year, but that number jumps up 9%, so nearly half of respondents believe they have enough money to work with.

In terms of how marketers are allocating that money, we handled the question a little differently this year. Traditionally, we asked respondents for their overall budget allocation and then more specifically how they dole out the money set aside for non-personal promotion. This year, we combined budget allocation into one question (though we do examine digital media spend a little later). This is important to keep in mind when reviewing Figure 10, because the results from this year were calculated differently from the previous years when non-promotional avenues, such as dinner meetings/teleconferences/webinars, direct mail, and point of care, were all asked about in a separate question. So that may skew the results when comparing to previous years, but we still wanted to provide an overview of how respondents spend their marketing dollars.

In terms of how marketers are allocating that money, we handled the question a little differently this year. Traditionally, we asked respondents for their overall budget allocation and then more specifically how they dole out the money set aside for non-personal promotion. This year, we combined budget allocation into one question (though we do examine digital media spend a little later). This is important to keep in mind when reviewing Figure 10, because the results from this year were calculated differently from the previous years when non-promotional avenues, such as dinner meetings/teleconferences/webinars, direct mail, and point of care, were all asked about in a separate question. So that may skew the results when comparing to previous years, but we still wanted to provide an overview of how respondents spend their marketing dollars.

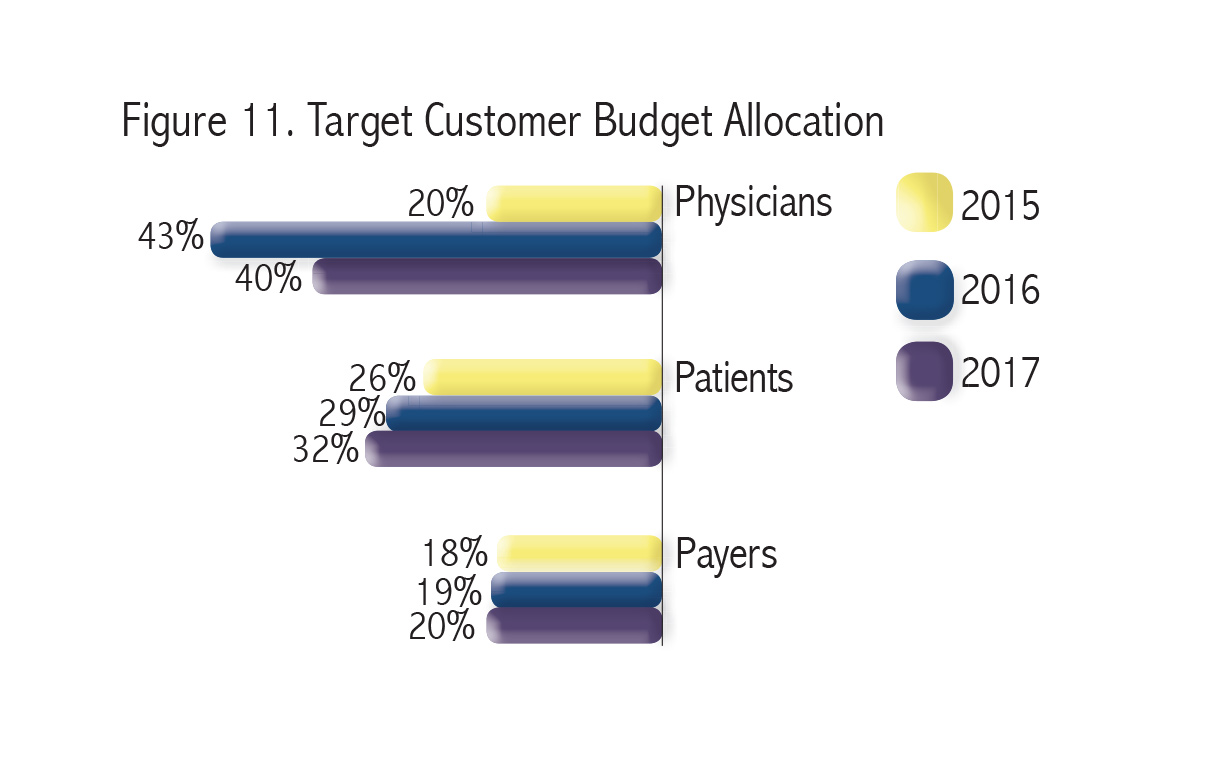

Another change from previous surveys: We asked respondents how they were allocating their budgets in terms of three target customers: Patients, Physicians, and Payers (Figure 11). Respondents were asked to let us know how much of their budget was devoted to each customer segment in 2015, how much they spent this year, and how much they planned to spend in 2017. As you can see, the biggest change is how much marketers are spending on physicians, as the average percentage increases from 20% last year to around 40% this year and next. One reason for this may be as a solution to compensate for smaller sales forces, but it is important to note that the average may be skewed a bit by a couple of respondents who plan to increase their marketing spend to physicians by around 80%.

Budget Changes

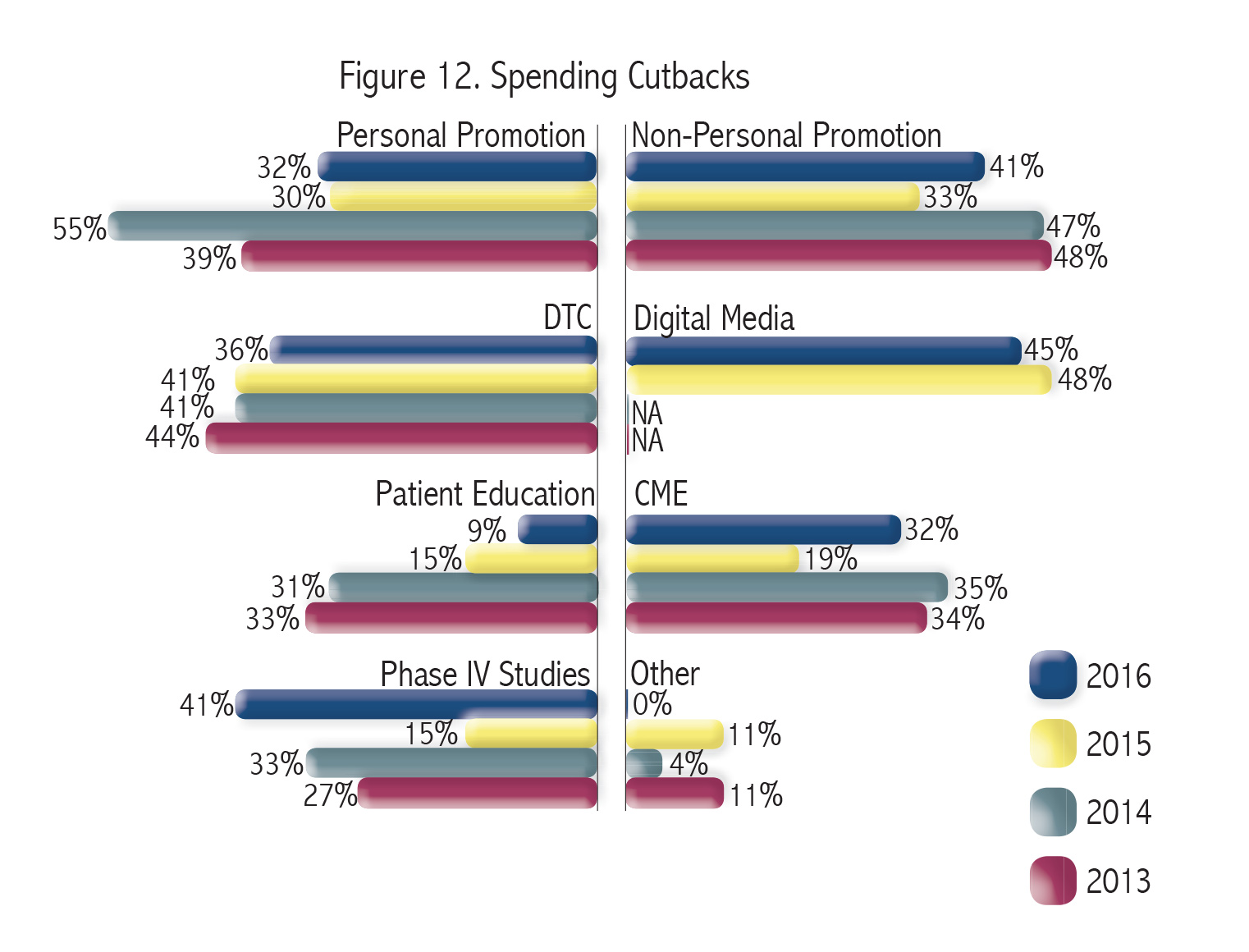

Despite the increase in overall marketing budgets, the plurality of respondents (39%) said that their budgets actually decreased from the previous year. Meanwhile, only 29% of respondents reported that their budgets increased, which is down from 32% last year. However, both of this year’s reported budget changes (the 39% decrease and 29% increase) are much closer to what we heard from marketers from 2012 to 2014, so perhaps 2015 was an aberration. Just to round things out, 32% said that their budget experienced no change from the previous year.

The good news for marketers with decreased budgets: The cuts were not as deep. This year, marketing budgets were only slashed an average of 16% compared to 24% in 2015. And similar to last year, when it comes time to make cuts, the plurality of respondents (45%) choose to scale back their digital media efforts (Figure 12). Another perennial popular area for cut backs is non-personal promotion, which received a bit of reprieve last year, but is up 8%. CME and Phase IV Studies also rose back to become closer to what we saw in 2014 and 2013—more support that 2015 might have been an outliner, in terms of marketing budgets at least. However, the trend of holding back patient education cuts continues as it drops from around 30% to 15% to just 9% this year, so patient centricity efforts may be affecting marketing decision-making. One finding that is somewhat of a surprise: Marketers were a little less willing to cut DTC spend (by about 5%), while that is usually one of the first places our previous respondents turned to for cuts.

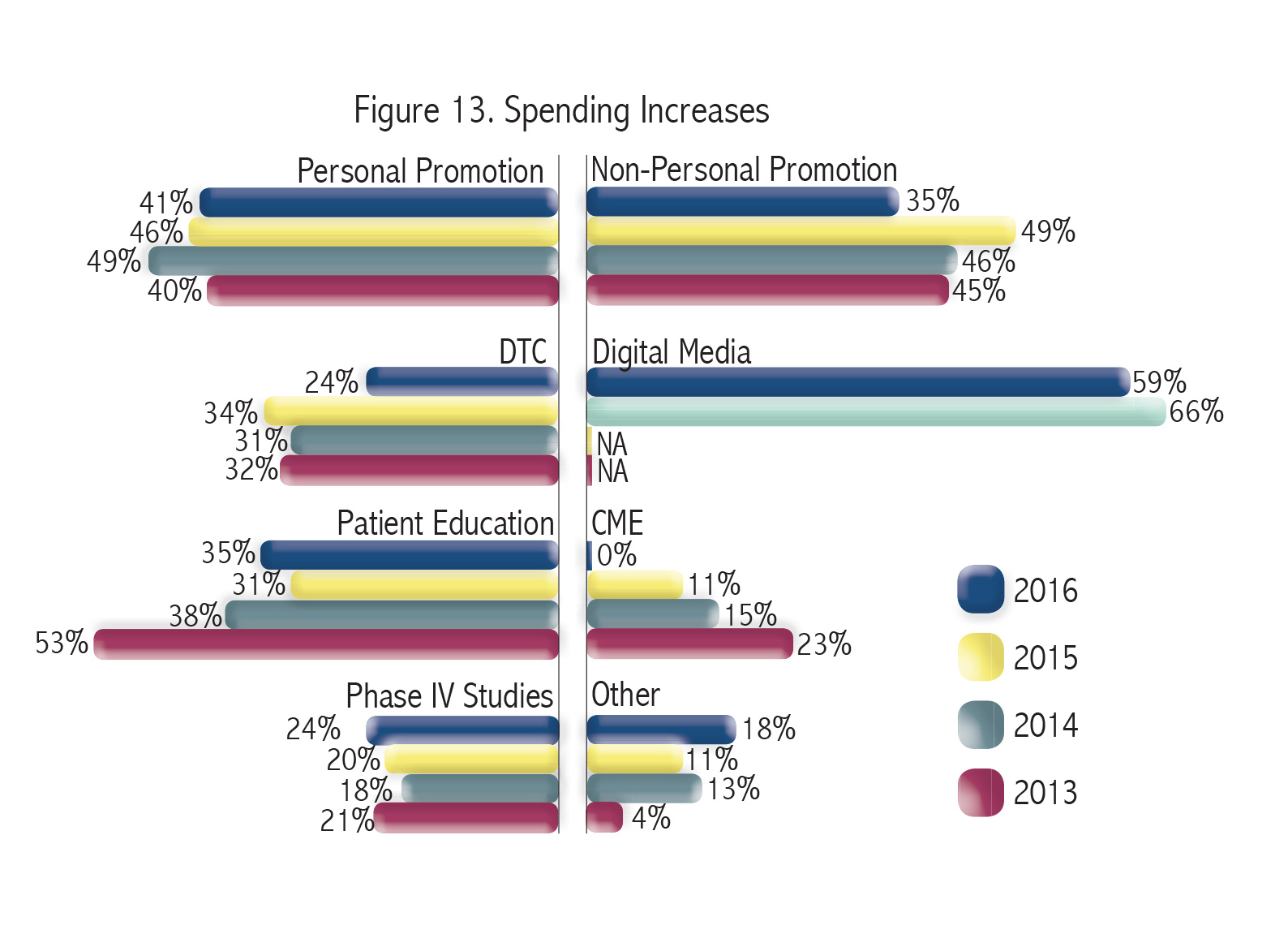

For those lucky few whose budgets did tick up, they were given an average of 24% more marketing dollars. That is a slightly larger increase than last year’s group who received an average of 22% more, but much lower compared to 2014’s 46%. As has been the case for nearly every year we do this survey, the area in which marketers are most likely to turn for cuts is typically also the area they are more willing to invest more in when they have the money to do so. In this case, the majority of marketers (59%) are putting their extra dough into digital media (Figure 13). The biggest differences from last year, and most previous years, is fewer marketers are willing to put any more into their DTC efforts (down 10% from 2015) and non-personal promotion (down 14%). Another oddity: No respondent was willing to put any extra money into CME. However, overall CME has been receiving a smaller piece of the marketing dollars pie each of the past few years.

For those lucky few whose budgets did tick up, they were given an average of 24% more marketing dollars. That is a slightly larger increase than last year’s group who received an average of 22% more, but much lower compared to 2014’s 46%. As has been the case for nearly every year we do this survey, the area in which marketers are most likely to turn for cuts is typically also the area they are more willing to invest more in when they have the money to do so. In this case, the majority of marketers (59%) are putting their extra dough into digital media (Figure 13). The biggest differences from last year, and most previous years, is fewer marketers are willing to put any more into their DTC efforts (down 10% from 2015) and non-personal promotion (down 14%). Another oddity: No respondent was willing to put any extra money into CME. However, overall CME has been receiving a smaller piece of the marketing dollars pie each of the past few years.

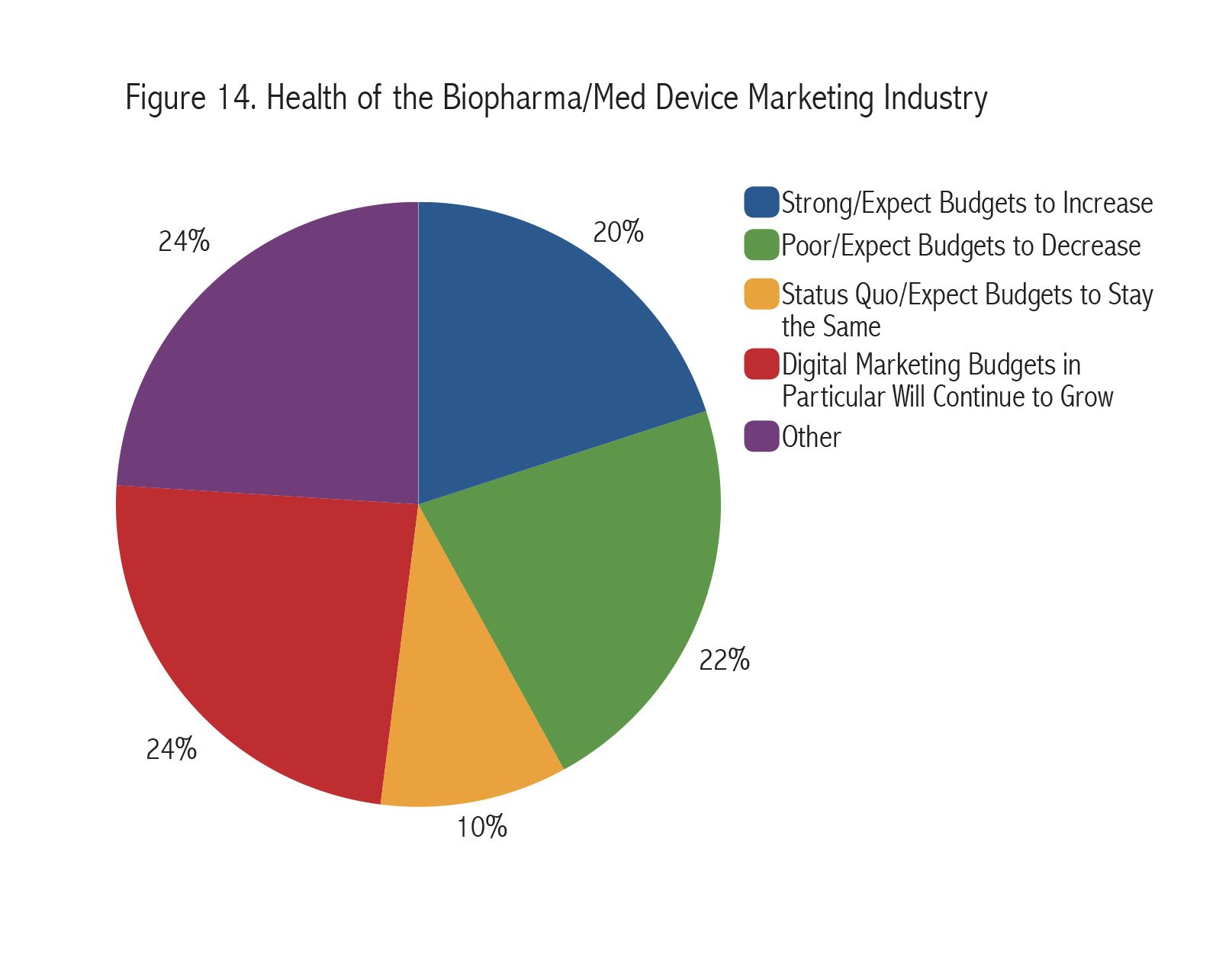

Future Budgets

For the first time, we asked respondents to evaluate the overall health of pharma/medical device advertising today. When it came to how budgets would be affected down the road, opinions were fairly split across the board (Figure 14). About 20% felt the industry was in good shape and expected budgets to increase, while 22% felt the industry was doing poorly and budgets were sure to decease. But the plurality, by a slim margin, mentioned the growing strength of digital and expected more money to be to put into that area.

As one respondent puts it, “Budgets will likely rise but what I believe will have the biggest impact is the allocation of funding within the promo-mix model. Several companies will shift to a reliance on digital when they realize the higher ROI.” Another feels the lack of ROI will actually hurt digital: “They are going to fall, because we now have enough data to show that some of these digital placements are a waste of time. I also think there will be stress to reform the personal promotion side, which will require some funding.”

As one respondent puts it, “Budgets will likely rise but what I believe will have the biggest impact is the allocation of funding within the promo-mix model. Several companies will shift to a reliance on digital when they realize the higher ROI.” Another feels the lack of ROI will actually hurt digital: “They are going to fall, because we now have enough data to show that some of these digital placements are a waste of time. I also think there will be stress to reform the personal promotion side, which will require some funding.”

One respondent predicts bad news ahead for agencies as more marketing technology is announced: “Agency budgets will continue to fall as long as there is technology. They charge too much for sub-par execution. Agencies are great for conceptual ideation, but not always up to date with the latest technology and concepts.” But another feels digital has only spurred better ideation: “Creativity has increased with the focus on non-traditional advertising—using Facebook, Twitter, etc.—and finding other ways besides TV commercials and banner ads.”

One respondent says the key in the future “is all about tying economic factors to clinic outcome. Whoever can do this the most effectively will succeed with the rising power of value analysis committees.”

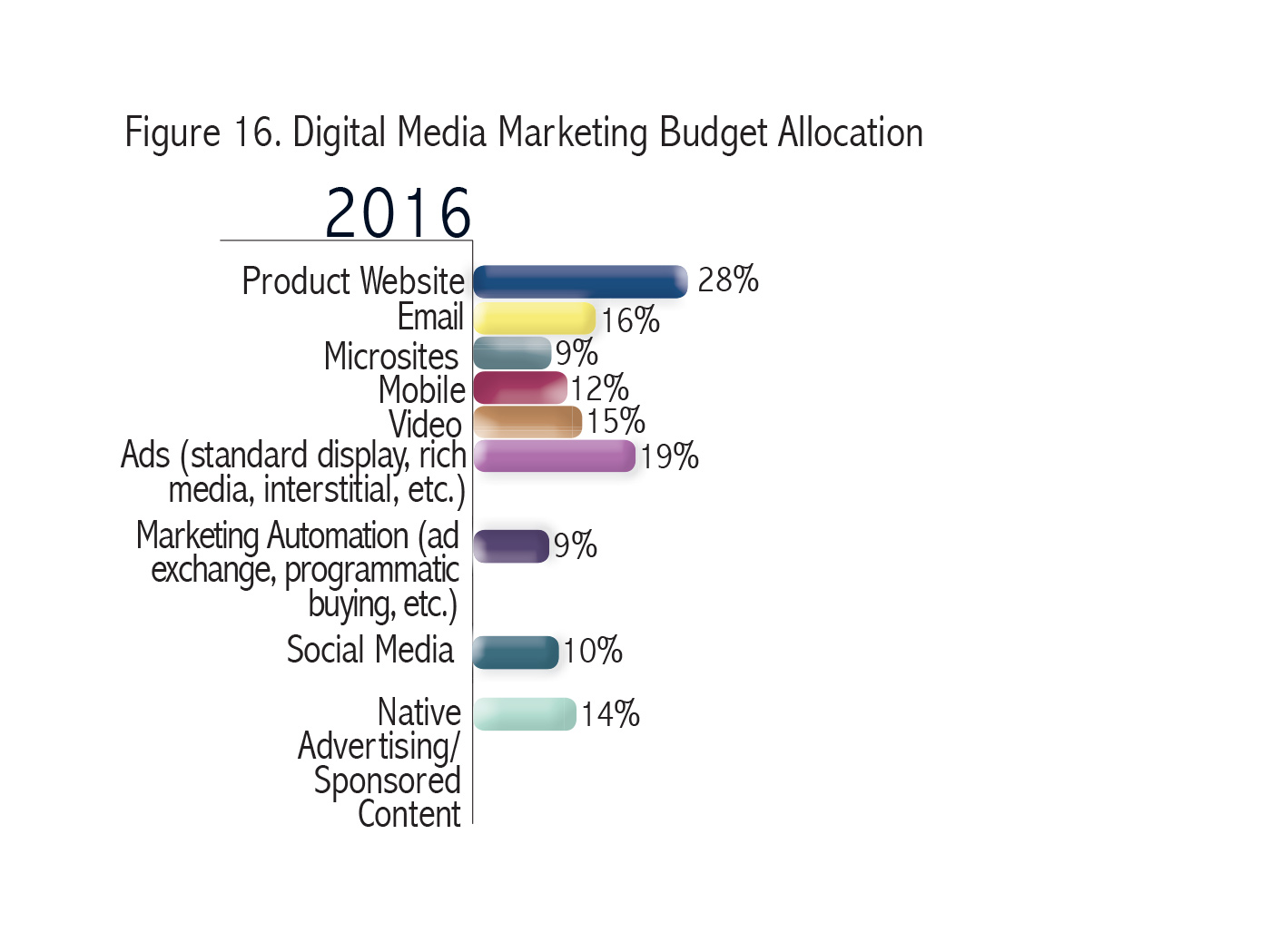

Digital Spend

For the first time, we asked respondents to break down how they allocate their digital spend (Figure 16). Unsurprisingly, the largest chunk (28%) goes to a product’s brand.com site. Then, the second most is spent on online ads (19%) followed by email (16%), video (15%), and native advertising/sponsored content (14%). Most of these have been the standards in digital for years, so it is not shocking that marketers are sticking with what higher ups most likely find to be the safest avenues in digital. Even though native advertising is somewhat of a buzzword, it is still an old concept that has found a new package online. The remaining digital channels are all fairly bunched together: Mobile (12%), social media (10%), microsites (9%), and marketing automation (9%). So it seems like marketers are just spreading their dollars until they are better able to determine which is most effective.

Meanwhile, the majority of our respondents (53%) are only somewhat concerned about ad blocking. And 25% of respondents have either very little concern or are not concerned at all. For the 17% that are very concerned, they are short on solutions. Most of them are still searching, while one mentions working with his or her agency to optimize ads to minimize this occurrence. Other potential solutions mentioned include diversifying advertising dollars, requesting an agreement from the target, and offering incentives for not using ad blocking software.

Meanwhile, the majority of our respondents (53%) are only somewhat concerned about ad blocking. And 25% of respondents have either very little concern or are not concerned at all. For the 17% that are very concerned, they are short on solutions. Most of them are still searching, while one mentions working with his or her agency to optimize ads to minimize this occurrence. Other potential solutions mentioned include diversifying advertising dollars, requesting an agreement from the target, and offering incentives for not using ad blocking software.

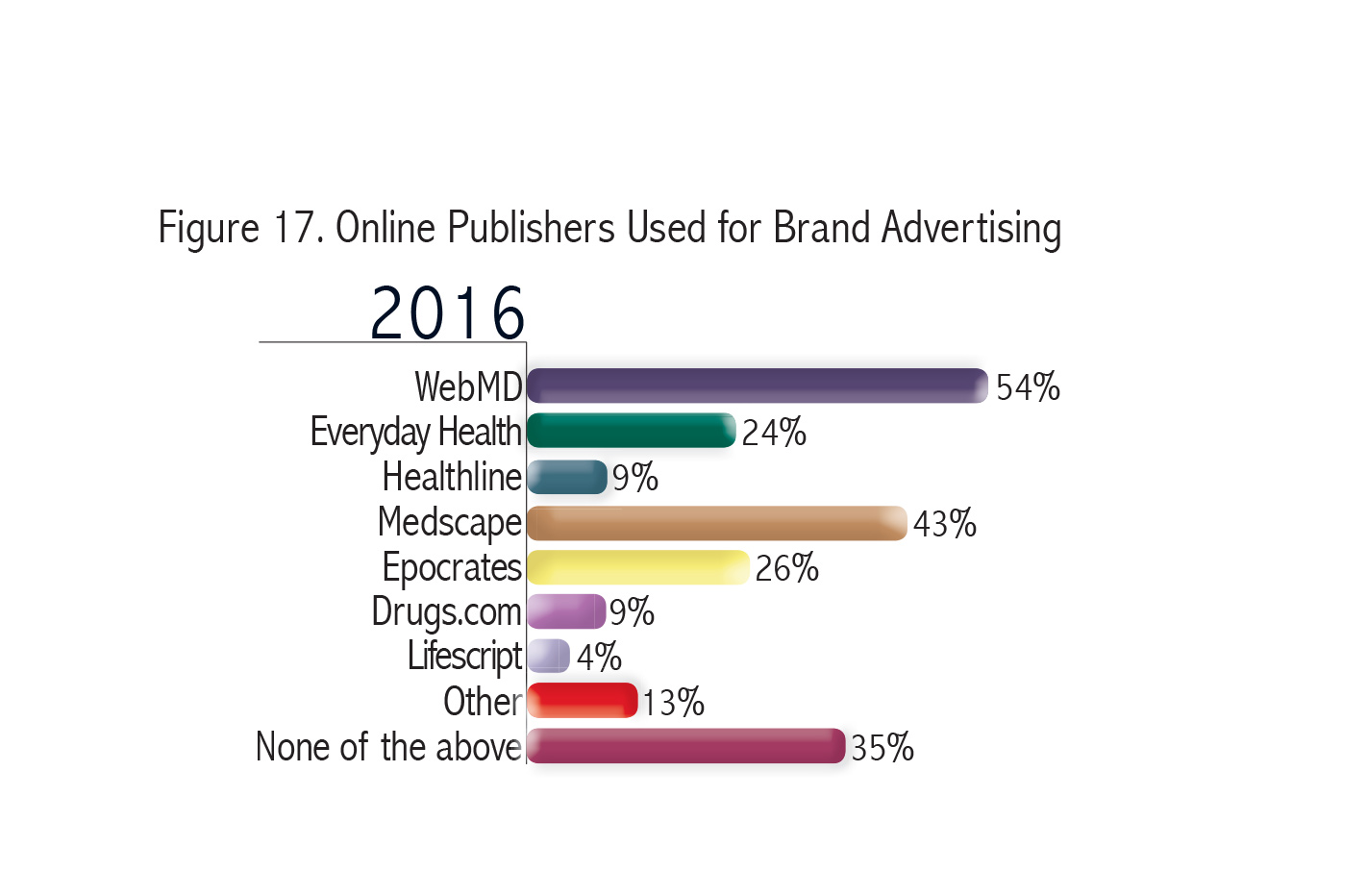

Online Publishers

Another new addition to this year’s survey: We asked respondents to tell us what online publishers/website they are currently using to advertise their brand (Figure 17). None of the top four names would shock you: WebMD (54%), Medscape (43%), Epocrates (26%), and Everyday Health (24%). Some of the other website that respondents wrote in as answers include Blackdoctor.org, Univision, Flatiron, SARX, Patient Portals, AJMC, watzan/ZEN, and CLN, CLP, MLO, CAP Today. But what is far more interesting are respondent’s answers when we asked them to tell us why these are their go-to sites.

Medscape is considered a good spot for our respondents because “it drives traffic” and has the “best conversion rate to branded site hits.” Sharecare, Flatiron, Patient Portals were all said to “offer good reach, in customer workflow/journey and offer competitive ROI.” WebMD rates high “because consumers look there.” One respondent says, “watzan/ZEN is the only publisher that creates a dynamic personal experience for each of my customers.” That respondent also adds, “We have not been able to determine a definitive ROI with any publisher and stopped using that as a buying metric.” A couple of other sites/publishers that respondents listed as their favorites with no added explanation were: PatientsLikeMe, UpToDate, Liquid Grids, and Thompson.

What’s On the Horizon

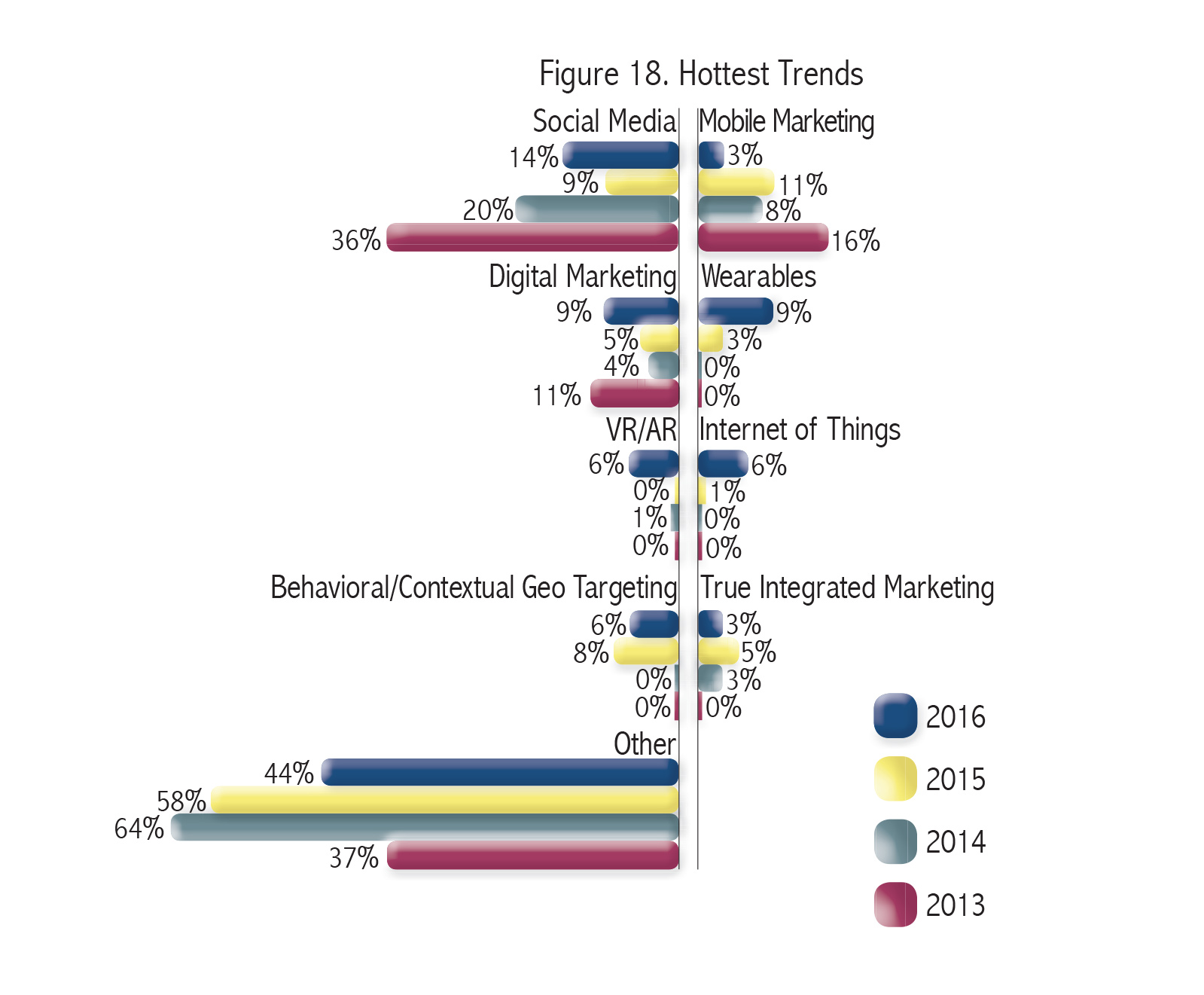

They say trends come and go, but for the pharma industry they just can’t seem to let go of the idea of social media as a trend. While social media was unseated last year as the top named trend, it is once again back on top (Figure 18). Though to be fair, only 14% of respondents named it, so it is a very small plurality and at this point it might have become a default answer for people who really can’t come up with anything new that the industry is actually working on. Or they are just referring to new channels within social media, though our respondents didn’t name anything specific.

Meanwhile, last year’s top trend, the use of Big Data, received zero responses this year, which is why we omitted it from this year’s chart. That doesn’t mean marketers have turned away from Big Data. It could mean they have embraced it more quickly than social media and decided that it is no longer new. However, the idea of using data for some kind of targeting (whether it is behavioral, contextual, or geo) is still a top trend for 6% of our respondents.

Meanwhile, last year’s top trend, the use of Big Data, received zero responses this year, which is why we omitted it from this year’s chart. That doesn’t mean marketers have turned away from Big Data. It could mean they have embraced it more quickly than social media and decided that it is no longer new. However, the idea of using data for some kind of targeting (whether it is behavioral, contextual, or geo) is still a top trend for 6% of our respondents.

A couple of trends that have been on the periphery the past few years are picking up steam. Wearables was mentioned by an additional 6% of respondents compared to last year, and the Internet of Things was mentioned by another 5%. So connected devices may be becoming a bigger priority for pharma and medical device companies, as the industry watches tech companies like Apple (with HealthKit) or Fitbit (with their move into developing medical-grade devices) make health a bigger priority. One respondent even specifically mentions:“Interactive technology, i.e., smart-inhalers for patient-physician dialogue and compliance reminders.”

While only one respondent has mentioned augmented reality/virtual reality in previous surveys, it has become a somewhat popular trend this year. But virtual reality has come a long way recently and consumer devices are starting to hit the market that make it easier for both users and developers to get into this space. A couple of the other interesting ideas that were named by just a single respondent: Watson Health Cognitive Computing, programmatic buying, pre-launch contracting, and positive PR.

Agency/Vendor Partnerships

But overall, it sounds like marketers are still searching for truly innovative new ideas. And 5% of respondents would like their agency/vendor partners to be better at delivering such innovative solutions. While that number may seem small, it was a write-in response so it is obviously something top of mind for quite a few respondents. Plus, the majority (63%) said they want their agencies/vendors to be better at ideation, so they definitely desire partners who are better at creating improved campaigns and solutions. Meanwhile, 32% want agencies/vendors to be better at research, 27% want more help with presentations, 15% are looking for better negotiators, and 7% would like help improving sales tactics. Two more popular write-in answers: Execution and knowledge (especially in the global environment).

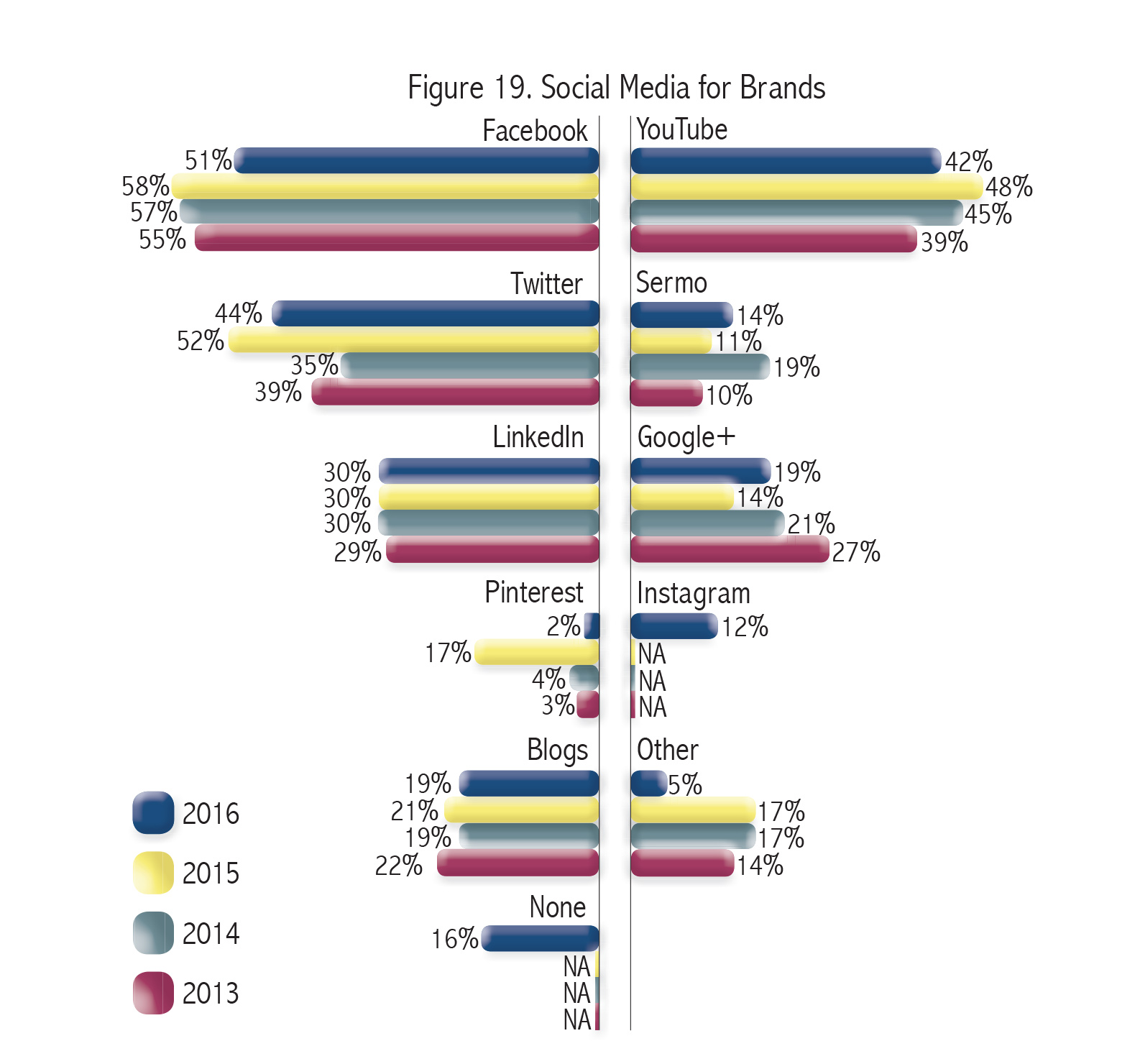

Social Media

Last year, 73% of respondents predicted that social media use among pharma marketers would increase in 2016. But based on this year’s respondents, that doesn’t seem to be the case (Figure 19). For the most part, social media use for brands either went down a little or remained stagnant—at least in the channels we asked about. Compared to last year, use of Facebook is down (51% vs. 58%) as is YouTube (42% vs. 48%), Twitter (42% vs. 48%), and Pinterest (2% vs. 17%). However, use of both Sermo and Google+ rose a bit and Instagram debuted at 12%. Meanwhile, LinkedIn stayed at 30%. Based on this data, it doesn’t seem like the guidances the FDA released in 2014 have led to rampant social media use for marketing purposes or that pharma marketers have fully embraced social media yet. But that may no longer be a regulation issue. As we learned earlier in the survey, most respondents still rely on ROI for deciding which channels to use, and a few respondents mentioned they didn’t feel digital channels (though no one specifically said social) deliver results. So the next hurdle to overcome before we see the use of social media channels rise may be finding better ways to determine their ROI.

New Opportunities

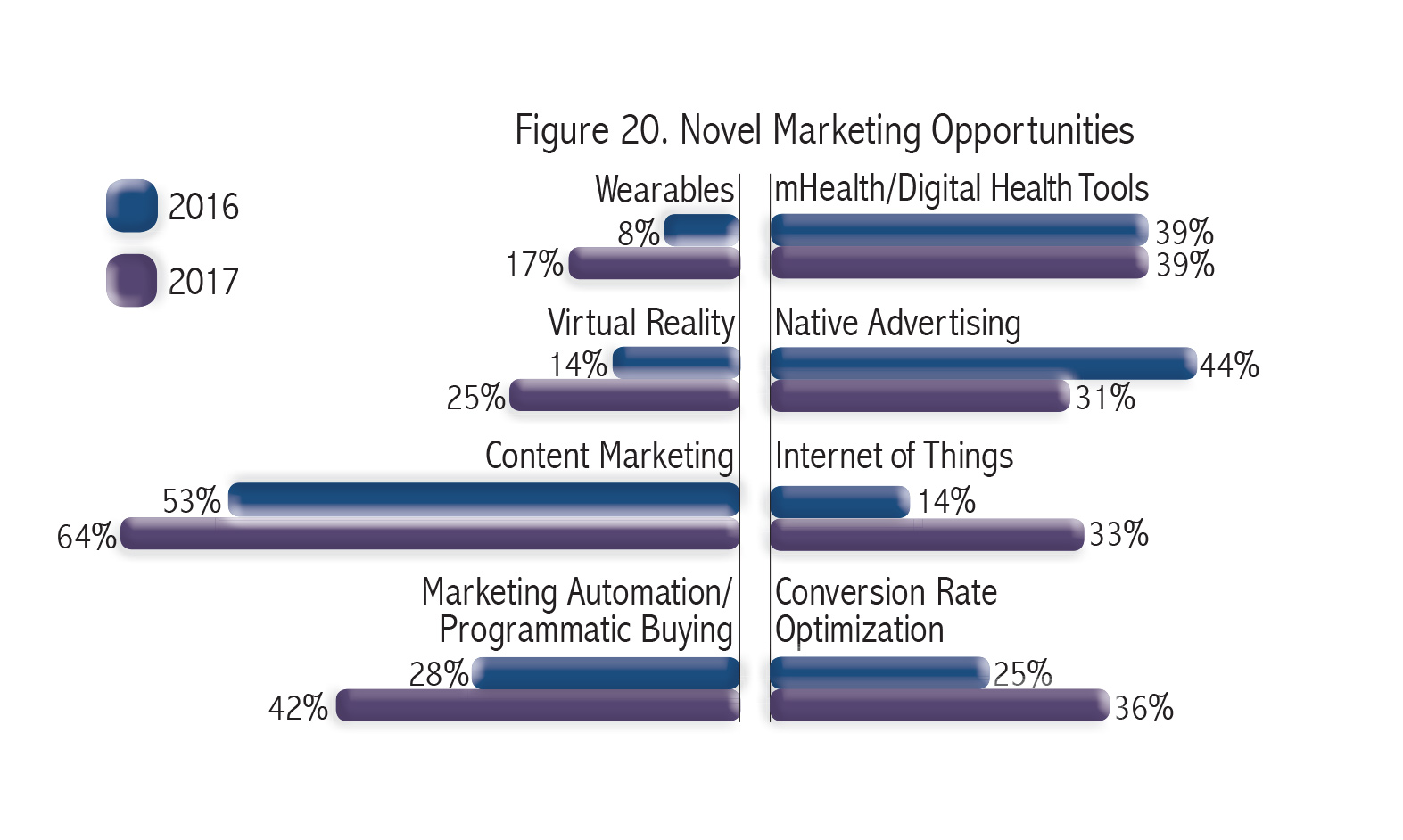

While pharma and medical device marketers are not fully embracing social media yet, they are looking at other novel marketing opportunities/strategies (Figure 20). Among the different opportunities we asked about, the majority of respondents are already doing something with content marketing this year (53%) and even more plan to implement it next year (64%). And it turns out, we asked about what several of our respondents ended up naming as their top trends for 2017, including wearables, virtual reality, and Internet of Things. And all three of these channels appear to be gaining in popularity as the use of Internet of Things will increase by 19% by next year, VR will rise by 11%, and wearables by 9%. The same is true of content marketing and conversion rate optimization, which are both expected to climb by 11%, and the use of marketing automation/programmatic buying which could see a rise of 14%. The only opportunity that marketers are already losing interest in is native advertising, as 13% fewer of our respondents will use this strategy in 2017 compared to this year.

Thanks To Our Respondents From These Companies

5NS Venture/Ethicon

A.P. Pharma, Inc.

Aesculap

Alcon

Alexion Pharmaceuticals, Inc.

American Regent

Aqua Pharmaceuticals

Astellas Pharma US, Inc.

AstraZeneca

Auriga Pharmaceuticals

AuroMedics Pharma

AVEO Pharmaceutical

Baxalta

Bayer Healthcare Pharmaceutical

Bayer Radiology

BioTek Instruments

Boehringer Ingelheim

Bristol-Myers Squibb

Centerpulse Dental Inc.

Chiesi USA

Cure Medical

Eli Lilly and Company

Eisai

Essential Pharmaceuticals

Fera Pharmaceuticals

Ferring Pharmaceuticals

Forest Laboratories Inc.

GE Healthcare

Genzyme

Germfree

Gibson Interprises

Global Pharmaceuticals

Hologic, Inc.

Impax Laboratories

Impax Pharmaceuticals

InterMetro Industries Corporation

Kidz Med Inc.

Konsyl Pharmaceuticals

Lupin Pharmaceuticals

Merck & Co., Inc.

NantWorks

Novartis

Novartis Vaccines and Diagnostics Inc.

Novavax, Inc.

Novo Nordisk Inc.

Nutricia

Onset Dermatologics

Patheon, Inc.

Perrigo Company

Pfizer

Prometheus

Purdue Pharma

Roche Diagnostics Corporation

Romark Laboratories, LC

Sandoz, Inc.

Sanofi

Sanofi Pasteur

SCOLR Pharma

Sekisui Diagnostics

Sirtex Medical Inc.

Span America Medical Systems, Inc.

Sunovion Pharmaceuticals, Inc.

Takeda Oncology

Takeda Pharmaceuticals USA, Inc.

Taxus Cardium

Trevena, Inc.

Tris Pharma, Inc.

Tulex Pharmaceuticals

UCB, Inc.

Ultragenyx Pharmaceuticals, Inc.

Valeant Pharmaceuticals

VANDA Pharmaceuticals, Inc.

Varian Medical Systems, Inc.

VCB Pharma

Vericel Corporation

Vertex Pharmaceuticals

Vicus Therapeutics

Wockhardt USA

Zosano Pharma

ZymoGenetics, Inc.